Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI POLICY: Waller Stresses Fed's Independence in Debut Speech

- Suez Canal Cleared, Container Ship Ever Given Refloated, Sails Into Bitter Sea

- BIDEN TO SAY 90% OF U.S. ADULTS ELIGIBLE FOR SHOT BY APRIL 19, Bbg

- Biden to Reveal Major Spending Plan With Big Battle Ahead, Bbg

- Multi-trillion dollar long-term plan to be unveiled Wednesday

- White House also presents glimpse of 2022 budget later in week

- CDC DIRECTOR WARNS OF 'IMPENDING DOOM' AS CASES RISE AGAIN; 'RIGHT NOW, I'M SCARED' GIVEN RISE IN COVID CASES, Bbg

- Moderate Democrats buck Biden tax hikes, Axios

US TSY SUMMARY: Risk-On

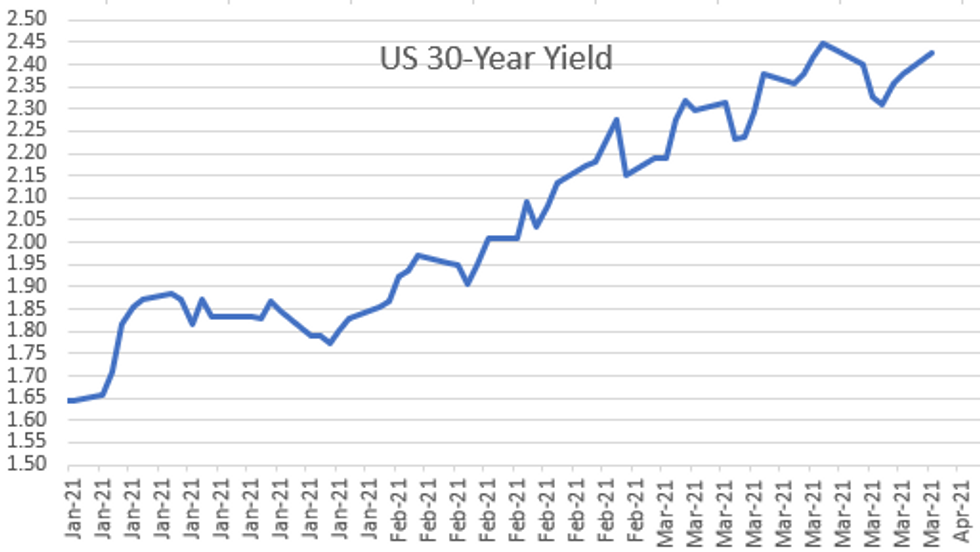

Dire pandemic warnings from CDC director and large dealer losses tied to forced equity unwinds (Archegos fund $20B blow-up continues to trigger massive block sales at several dealers) apparently taken with some reservations Monday. Risk-on tone resumed in second half: Tsy extended sell-off as equities pared losses as equities traded higher.- S&P futures tapped 3971.25 -- just off all-time high of 3977.0 on March 17. High yield marks: 10YY 1.7259%, 30YY 2.4238%.

- Early London hours story that Deutsche Bank may have avoided the forced liquidation pain of fund debacle debatably triggered a sell-off in rates as losses on forced unwinds may not be as bad or as systemic as feared -- despite sporadic reports of large block sales from Morgan Stanley, Wells Fargo, JPM on day.

- While CDC head warned of "impending doom" over case rise, the surge in the amount of people vaccinated and/or expected to receive tempered those concerns somewhat. Meanwhile, shipping traffic on the Suez Canal resumed as the Ever Given container ship was refloated Monday, ending the expensive back-log of ships (est $10B/day drag on global trade).

- Eurodollar and Treasury option trade saw renewed interest in low-delta put buying, hedging rate hike risk starting mid-2022 through 2023.

- Late session: 2-Yr yield is up 0.2bps at 0.1407%, 5-Yr is up 2.1bps at 0.8861%, 10-Yr is up 3bps at 1.7063%, and 30-Yr is up 3bps at 2.4081%.

US

FED: Federal Reserve Governor Christopher Waller on Monday stressed the central bank's independence during his first speech since being appointed by former President Donald Trump, saying costs associated with U.S. deficits won't influence monetary policy decisions.

- "Deficit financing and debt servicing issues play no role in our policy decisions and never will," said Waller. He made no direct reference to the record outlays planned by Joe Biden's administration. for more see MNI Policy main wire at 1106ET.

- Excerpt from recent Washington Post story says the "two-pronged package Biden will begin unveiling this week includes higher amounts of federal spending but also significantly more in new tax revenue — with possibly as much as $4 trillion in new spending and more than $3 trillion in tax increases."

OVERNIGHT DATA

US MARCH DALLAS FED MANUFACTURING INDEX AT 28.9 VS 17.2

MARKETS SNAPSHOT

Key late session market levels:- DJIA up 98.49 points (0.3%) at 33171.37

- S&P E-Mini Future down 0.5 points (-0.01%) at 3964.25

- Nasdaq down 79.1 points (-0.6%) at 13059.65

- US 10-Yr yield is up 3.2 bps at 1.7081%

- US Jun 10Y are down 11.5/32 at 131-13

- EURUSD down 0.0029 (-0.25%) at 1.1765

- USDJPY up 0.17 (0.16%) at 109.81

- WTI Crude Oil (front-month) up $0.61 (1%) at $61.58

- Gold is down $20.93 (-1.21%) at $1711.53

European bourses closing levels:

- EuroStoxx 50 up 16.19 points (0.42%) at 3882.87

- FTSE 100 down 4.42 points (-0.07%) at 6736.17

- French CAC 40 up 26.7 points (0.45%) at 6015.51

MONTH-END EXTENSIONS: Preliminary Barclays/Bbg Extension Estimates

Forecast summary compared to the avg increase for prior year and the same time in 2020. TIPS 0.07Y; Govt inflation-linked, 0.02. Notice the bounce in US Tsy, Agency and MBS estimates, and drop in Credit extension est vs. last year.

| Estimate | 1Y Avg Incr | Last Year | |

| US Tsys | 0.07 | 0.09 | -0.03 |

| Agencies | 0.03 | 0.05 | -0.03 |

| Credit | 0.09 | 0.09 | 0.16 |

| Govt/Credit | 0.08 | 0.09 | 0.06 |

| MBS | 0.12 | 0.06 | 0.03 |

| Aggregate | 0.09 | 0.08 | 0.04 |

| Long Gov/Cr | 0.1 | 0.09 | 0 |

| Iterm Credit | 0.09 | 0.08 | 0.09 |

| Interm Gov | 0 | 0.08 | 0.01 |

| Interm Gov/Cr | 0.09 | 0.08 | 0.05 |

| High Yield | 0.12 | 0.1 | 0.12 |

US TSY FUTURES CLOSE:

- 3M10Y +4.96, 170.531 (L: 161.013 / H: 171.065)

- 2Y10Y +4.257, 157.595 (L: 149.893 / H: 157.951)

- 2Y30Y +4.713, 228.262 (L: 219.881 / H: 228.342)

- 5Y30Y +2.339, 153.469 (L: 149.644 / H: 153.469)

- Current futures levels:

- Jun 2Y down 0.5/32 at 110-12.625 (L: 110-12.5 / H: 110-13.5)

- Jun 5Y down 5.5/32 at 123-21.5 (L: 123-20.25 / H: 123-30)

- Jun 10Y down 13.5/32 at 131-11 (L: 131-09.5 / H: 131-31.5)

- Jun 30Y down 1-8/32 at 154-23 (L: 154-22 / H: 156-14)

- Jun Ultra 30Y down 2-12/32 at 181-04 (L: 181-04 / H: 184-15)

US EURODOLLAR FUTURES CLOSE:

- Jun 21 -0.005 at 99.825

- Sep 21 steady at 99.810

- Dec 21 steady at 99.745

- Mar 22 steady at 99.785

- Red Pack (Jun 22-Mar 23) steady to -0.035

- Green Pack (Jun 23-Mar 24) -0.055 to -0.075

- Blue Pack (Jun 24-Mar 25) -0.075 to -0.07

- Gold Pack (Jun 25-Mar 26) -0.08 to -0.075

Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N -0.00050 at 0.07288% (-0.00350 total last wk)

- 1 Month +0.00125 to 0.10850% (-0.00113 total last wk)

- 3 Month +0.00350 to 0.20250% (+0.00212 total last wk) (Record Low of 0.17525% on 2/19/21)

- 6 Month -0.00037 to 0.20288% (+0.00087 total last wk)

- 1 Year +0.00075 to 0.28150% (+0.00450 total last wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $75B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $252B

- Secured Overnight Financing Rate (SOFR): 0.01%, $924B

- Broad General Collateral Rate (BGCR): 0.01%, $374B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $347B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $8.801B accepted vs. $19.405 submitted

- Next scheduled purchases:

- Tue 3/30 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Wed 3/31 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Pause for Easter Holiday, Resume April 5:

- Mon 4/05 1100-1120ET: Tsy 0Y-2.25Y, appr $12.825B

PIPELINE: $2B Lowe's Matches BMW Debt Issuance

- Date $MM Issuer (Priced *, Launch #)

- 03/29 $2B #Lowe's $1.5B 10Y +90, $500M 30Y +107

- 03/29 $2B #BMW US $750M 3Y +50, $750M 3Y FRN SOFR+53, $500M 10Y +87.5 (BMW US issued $4B last year on April 6: $1.5B 3Y, $1.5B 5Y, $1B 10Y each +350)

- 03/29 $1B *Duke Energy Carolinas $550M 10Y +85, $450M 30Y +105

- 03/29 $925M #Burlington Northern Santa Fe 30Y +87.5

- 03/29 $700M *Korea National Oil $400M 5Y +52.5, $300M 10Y +75

- 03/29 $500M #Kohl's 10Y +167

- 03/29 $Benchmark Ghana 4Y 0% coupon, 8Y 8%a, 13Y 9%a, 21Y 9.5%a

- 03/29 $Benchmark Bahrain Nogaholding 8Y Sukuk

- 03/29 $200M #Maldives 5Y Sukuk 10.5%

- Expected Tuesday:

- 03/30 $Benchmark Dexia Credit 5Y +16a

FOREX: EUR/GBP Hits New Cycle Lows

- As UK lockdowns begin to ease, GBP is outperforming, with EUR/GBP hitting fresh 2021 lows Monday. The cross now eyes support at 0.8521, the 38.2% retracement of the 2015 - 2020 rally. This level was tested Monday and bears will be eyeing any close below.

- EUR was among the session's poorest performers, with EUR/USD remaining in the March downtrend and touching 1.1761 in the process. This retains the negative view for the single currency despite better performance in the EuroStoxx50, which hit the highest levels since 2008.

- The greenback was mixed, with a slightly steeper US Treasury curve helping support the USD index.

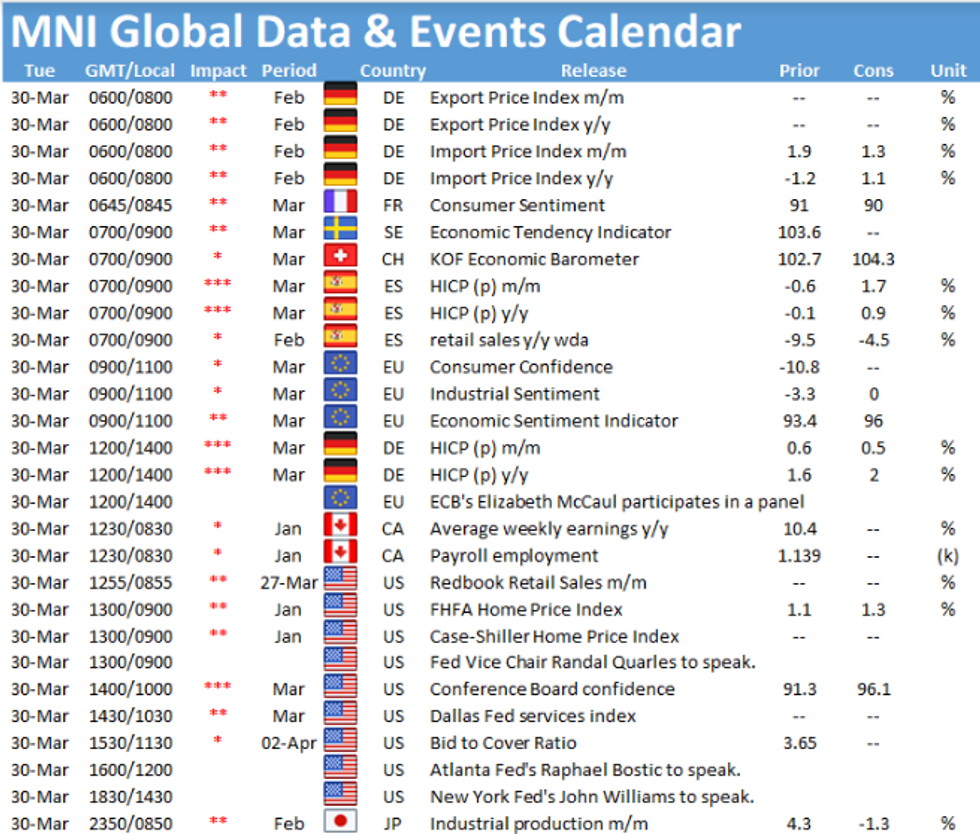

- Focus Tuesday turns to Japanese jobs & retail sales numbers, regional and national German CPIs and US consumer confidence data for March. Fed's Quarles & Williams are both speaking.

EGBs-GILTS CASH CLOSE: Early Rally Gives Way To Bear Steepening

Early bull flattening gave way to bear steepening over the course of Monday's session, as weekend concerns over a hedge fund default and Suez Canal blockage dissipated.

- Bund yields jumped around 0900BST on news that Deutsche Bank's exposure to Archegos was relatively limited. Later, fairly high offer-to-cover on BoE's short-dated APF (3.50x) contributed to the bearish tone.

- Periphery spreads tightened, led by Greece (10Y GGB -1.8bps vs Bunds). UK 5s30s hit highest levels since Mar 19; Germany since the 24th.

- Data showed ECB net asset purchases slowed slightly last week, though E19.0bn of PEPP buys was comparable to last week's accelerated pace.

- Attention turns to Tuesday's inflation data (Spain and Germany), as well as BTP supply.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 0.6bps at -0.709%, 5-Yr is up 1.9bps at -0.657%, 10-Yr is up 2.8bps at -0.318%, and 30-Yr is up 3.2bps at 0.248%.

- UK: The 2-Yr yield is up 0.6bps at 0.067%, 5-Yr is up 0.9bps at 0.341%, 10-Yr is up 3.1bps at 0.788%, and 30-Yr is up 3.7bps at 1.319%.

- Italian BTP spread down 0.7bps at 95.7bps/ Spanish spread down 0.2bps at 63.1bps

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.