Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

White House Nearing Fed Appointment Announcements

- BIDEN EYES RASKIN AS BANK'S VICE CHAIRWOMAN OF SUPERVISION: DJ

- BIDEN ALSO CONSIDERS COOK, JEFFERSON FOR OTHER FED POSTS: DJ

US

FED: Markets have been waiting for this since Powell's re-nomination on November 22, the White House looking to announce their new appointments to the Federal Reserve next week (no set time). DJ headlines:

- BIDEN EYES RASKIN AS BANK'S VICE CHAIRWOMAN OF SUPERVISION: DJ

- BIDEN ALSO CONSIDERS COOK, JEFFERSON FOR OTHER FED POSTS: DJ

US TSYS: New Highs For Stocks Yet Again

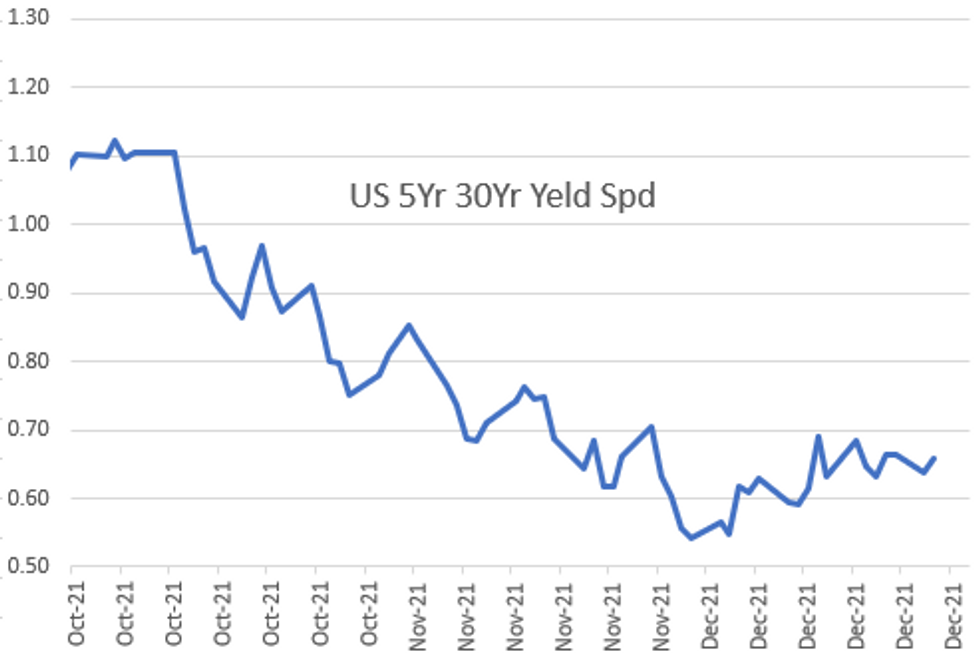

Tsys mixed after the bell, carry-over support for bonds from Mon evaporated since midmorning. Delayed selling after weak 5Y auction. Yield curves recovered from early flattening, 5s30s +2.37 to 65.79; very limited volumes (TYH2 >425k by the bell) should improve when London returns from holiday Wed.- Equities climb to new all-time highs, ESH2 4798.0; Gold reversed early gains, -5.65 to 1806.48 late; West Texas crude +0.47 at 76.04.

- No react to FHFA Home price index 1.1% M/M vs. 0.9% Est; +17.4% YoY.; US REDBOOK: Store sales +21.4% wk ended Dec 25; +17.3% vs. year ago lvl.

- QE: NY Fed buy-operations pause for holidays, resume January 3.

- Tsy futures held near middle of session range after paring gains ahead the auction. Delayed react after $57B 5Y note auction (91282CDQ1) tailed: 1.263% high yield vs. 1.257% WI; 2.41x bid-to-cover vs. last month's 2.34x. Indirect take-up: new year high of 65.66% vs. 56.88% last month. On tap Wed: $56B 7Y note sale (91282CDP3)

- Headline watching: White House Nearing Fed Appointment Annc next week

- The 2-Yr yield is up 4.9bps at 0.748%, 5-Yr is down 0.3bps at 1.2434%, 10-Yr is up 0.3bps at 1.479%, and 30-Yr is up 1.6bps at 1.8997%.

OVERNIGHT DATA

- U.S. OCT. FHFA HOME PRICE INDEX RISES 1.1% M/M vs. 0.9% Est; +17.4% YoY

- U.S. OCT. S&P CORELOGIC CS 20-CITY INDEX RISES 18.4% Y/Y

- US REDBOOK: DEC STORE SALES +17.3% V YR AGO MO

- US REDBOOK: STORE SALES +21.4% WK ENDED DEC 25 V YR AGO WK

- US REDBOOK: WILL RESUME MONTH-TO-MONTH DATA COMPARISON IN FEB 2022

MARKETS SNAPSHOT

Key late session market levels:- DJIA up 130.6 points (0.36%) at 36468.19

- S&P E-Mini Future down 2.5 points (-0.05%) at 4787.75

- Nasdaq down 75.9 points (-0.5%) at 15836.91

- US 10-Yr yield is up 0.3 bps at 1.479%

- US Jun 10Y are up 2/32 at 130-14

- EURUSD down 0.0024 (-0.21%) at 1.1307

- USDJPY down 0.05 (-0.04%) at 114.76

- WTI Crude Oil (front-month) up $0.35 (0.46%) at $76.00

- Gold is down $5.48 (-0.3%) at $1809.79

- EuroStoxx 50 up 23.95 points (0.56%) at 4308.07

- German DAX up 128.45 points (0.81%) at 15953.67

- French CAC 40 up 40.72 points (0.57%) at 7175.43

US TSY FUTURES CLOSE

- 3M10Y -0.244, 141.481 (L: 137.236 / H: 141.996)

- 2Y10Y -4.197, 72.875 (L: 71.069 / H: 77.792)

- 2Y30Y -2.854, 115.051 (L: 110.894 / H: 118.387)

- 5Y30Y +2.119, 65.677 (L: 61.232 / H: 66.645)

- Current futures levels:

- Mar 2Y up 0.375/32 at 109-1.5 (L: 109-01 / H: 109-02.25)

- Mar 5Y up 1.75/32 at 120-30.25 (L: 120-28 / H: 120-31.75)

- Jun 10Y up 2/32 at 130-14 (L: 130-12.5 / H: 130-19.5)

- Jun 30Y down 2/32 at 162-24 (L: 162-19 / H: 163-05)

US EURODOLLAR FUTURES CLOSE

- Mar 22 steady at 99.625

- Jun 22 steady at 99.380

- Sep 22 +0.005 at 99.175

- Dec 22 +0.005 at 98.940

- Red Pack (Mar 23-Dec 23) +0.010 to +0.025

- Green Pack (Mar 24-Dec 24) +0.015 to +0.020

- Blue Pack (Mar 25-Dec 25) +0.010 to +0.015

- Gold Pack (Mar 26-Dec 26) +0.005 to +0.010

SHORT TERM RATES

US DOLLAR LIBOR: No new settlement with London closed for Christmas holiday through December 28. Settlements as of Friday, December 24:

- O/N -0.00538 at 0.06975% (-0.00450 total last wk)

- 1 Month -0.00063 to 0.10125% (-0.00125 total last wk)

- 3 Month -0.00187 to 0.21788% (+0.00525 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00687 to 0.34325% (+0.03050 total last wk)

- 1 Year +0.00600 to 0.56713% (+0.03750 total last wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $75B

- Daily Overnight Bank Funding Rate: 0.07% volume: $257B

- Secured Overnight Financing Rate (SOFR): 0.04%, $888B

- Broad General Collateral Rate (BGCR): 0.05%, $328B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $316B

- (rate, volume levels reflect prior session)

- NY Fed buy-operations pause for holidays, resume Jan 3:

- Mon 01/03 1010-1030ET: Tsy 2.25Y-4.5Y, appr $6.325B vs. $7.375B prior

- Tue 01/04 1100-1120ET: TIPS 1Y-7.5Y, appr $1.525B

- Wed 01/05 1010-1030ET: Tsy 7Y-10Y, appr $2.425B vs. $2.825B prior

- Wed 01/05 1100-1120ET: Tsy 22.5Y-30Y, appr $1.825B

- Thu 01/06 1100-1120ET: TIPS 7.5Y-30Y, appr $0.925B

- Fri 01/07 1010-1030ET: Tsy 0Y-2.25Y, appr $9.325B

FED Reverse Repo Operation

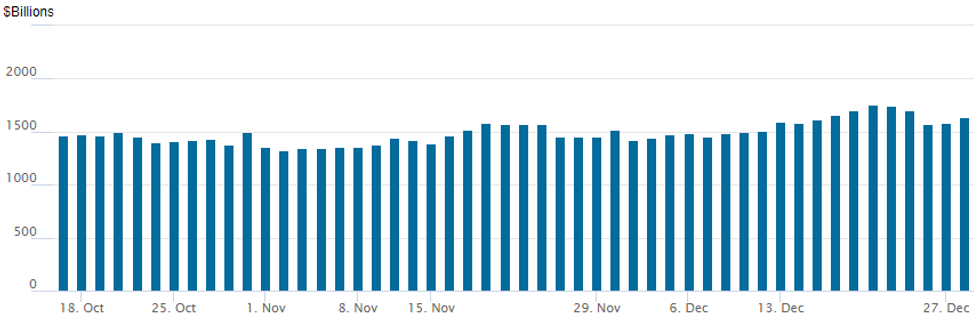

NY Federal Reserve/MNI

NY Fed reverse repo usage bounces to $1,637.064B from 78 counterparties vs. $1,580.347B Monday. Record high of $1,758.041B posted Monday, December 20.

OUTLOOK: Adv Goods Trade, Wholesale/Retail Inv's, Pending Home Sales, 7Y Sale

- US Data/Speaker Calendar (prior, estimate)

- Dec-29 0830 Advance Goods Trade Balance (-$82.9B, -$88.3B)

- Dec-29 0830 Wholesale Inventories MoM (2.3%, 1.5%)

- Dec-29 0830 Retail Inventories MoM (0.1%, 0.5%)

- Dec-29 1000 Pending Home Sales MoM (7.5%, 0.7%)

- Dec-29 1130 US Tsy $40B 119D bill CMB auction (912796U72)

- Dec-29 1130 US Tsy $24B 2Y FRN note auction re-open (91282CDE8)

- Dec-29 1300 US Tsy $56B 7Y Note auction (91282CDP3)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok