Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Inflation Seen Staying High, Making Fed Rate Pause Harder

- MNI INTERVIEW: High Prices Key Driver of Weak Sentiment- UMich

US

FED: A deceleration in inflation the Federal Reserve hopes could allow it to slow or pause rate hikes in the fall may not materialize, with current and former Fed staff economists telling MNI supply shocks and strong domestic demand are likely to keep prices rising more than expected for months longer.

- The full inflationary impact of the war in Ukraine and China's zero-Covid policy is only starting to be felt, the economists said. Meanwhile, continued reopening after pandemic restrictions could further fuel demand for services, a sector already experiencing acute staffing shortages and wage pressures. Housing costs are also headed higher still.

- While war has already sent energy prices soaring, the inability of Russia and Ukraine to export wheat and key fertilizer components like ammonia, natural gas and potash are just beginning to make their way into the production process and could hit food prices later this year, said Robert Rich, director of the Center for Inflation Research at the Cleveland Fed. For more see MNI Policy main wire at 1031ET.

- "They continue to hold pretty pessimistic views about the general state of the economy going forward and the common theme is inflation," said Joanne Hsu said in a phone interview Friday. "They are very concerned. They're worried about inflation. They're worried about their fellow Americans."

- While nearly 90% of people expect the Fed to continue to raise interest rates, Hsu said, Americans confidence in government policies to fight inflation is at its lowest level since 2014. "People really are not confident about about government policies to fight inflation." For more see MNI Policy main wire at 1706ET.

US TSYS: Late Risk Appetite Gathers Momentum

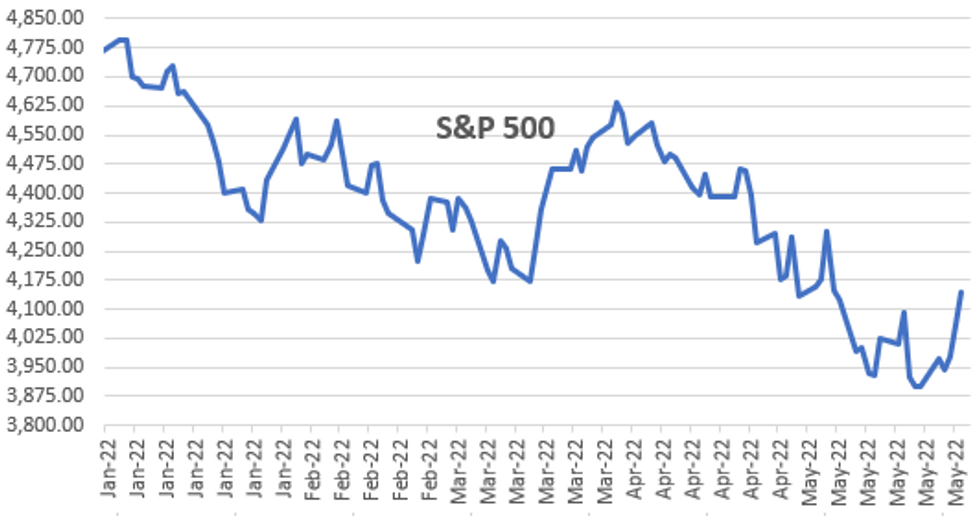

Midweek risk-on tone gathered momentum into Fri's close: Tsys steady/mixed with long end firmer but near second half lows while stocks continued to extend rally.

- SPX eminis were up near 5% for the week as risk appetite improved following Wed's May FOMC minutes release that showed a flexible Fed and no discussion of larger rate hikes ESM2 +105.25 (2.47%) at 4161.0.

- Bonds receded off early session highs post data, Apr core PCE at 4.9% YoY but headline of 6.3% YoY slightly higher than expected and fastest of last three months.

- Aside from PCE, Apr Advance Goods Trade Balance shows deficit of $105.9B vs. $114.9B expected; Wholesale Inventories +2.1% MoM vs. +2.0% exp.

- General quiet ahead Monday, May 30 Memorial Day national holiday. Cash FI markets closed while Globex opens at normal time Sunday evening at 1800ET through Monday at 1300ET. Globex reopens at 1800ET Monday evening.

- Tuesday focus: FHFA House Price Index MoM (2.1%, 2.0%); QoQ (3.3%, --); MNI Chicago PMI (56.4, 54.8); Conf. Board Consumer Confidence (107.3, 103.5); May-31 1030 Dallas Fed Manf. Activity (1.1, 1.5)

OVERNIGHT DATA

- US APR PERSONAL INCOME +0.4%; NOM PCE +0.9%

- US APR PCE PRICE INDEX +0.2%; +6.3% Y/Y

- US APR CORE PCE PRICE INDEX +0.3%; +4.9% Y/Y

- US APR UNROUNDED PCE PRICE INDEX +0.247%; CORE +0.344%

- Apr Advance Goods Trade Balance deficit of $105.9B vs. $114.9B expected deficit

- Wholesale Inventories +2.1% MoM vs. +2.0% expected

- MICHIGAN FINAL MAY CONSUMER SENTIMENT AT 58.4; EST. 59.1

- 5-Yr Inflation Forecast +3.0%

- 12-Mo Inflation Forecast +5.3%

- End-May Expectations 55.2

- End-May Current Index 63.3

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 576.23 points (1.77%) at 33213.42

- S&P E-Mini Future up 99.75 points (2.46%) at 4155.5

- Nasdaq up 390.5 points (3.3%) at 12131.13

- US 10-Yr yield is down 1.1 bps at 2.736%

- US Jun 10Y are down 1/32 at 120-18

- EURUSD up 0.0008 (0.07%) at 1.0733

- USDJPY up 0.02 (0.02%) at 127.14

- WTI Crude Oil (front-month) up $1.04 (0.91%) at $115.13

- Gold is up $2.93 (0.16%) at $1853.55

- EuroStoxx 50 up 68.55 points (1.83%) at 3808.86

- FTSE 100 up 20.54 points (0.27%) at 7585.46

- German DAX up 230.9 points (1.62%) at 14462.19

- French CAC 40 up 105.17 points (1.64%) at 6515.75

US TSY FUTURES CLOSE

- 3M10Y -1.841, 165.86 (L: 163.203 / H: 168.729)

- 2Y10Y -1.694, 24.813 (L: 23.515 / H: 28.795)

- 2Y30Y -2.766, 47.239 (L: 46 / H: 52.143)

- 5Y30Y -3.174, 23.775 (L: 23.066 / H: 27.752)

- Current futures levels:

- Jun 2Y up 2.375/32 at 106-4.25 (L: 106-01.625 / H: 106-05.375)

- Jun 5Y down 1.25/32 at 113-25.25 (L: 113-24 / H: 113-29.5)

- Jun 10Y down 1.5/32 at 120-17.5 (L: 120-16 / H: 120-27)

- Jun 30Y up 8/32 at 141-30 (L: 141-17 / H: 142-22)

- Jun Ultra 30Y up 11/32 at 158-16 (L: 158-01 / H: 159-19)

US 10Y FUTURES TECH: (U2) Challenging The 50-Day EMA

- RES 4: 122-00 Round number resistance

- RES 3: 121-27+ High Apr 5

- RES 2: 121-27+ High Apr 7

- RES 1: 120-15+/19+ 50-day EMA / Intraday high

- PRICE: 120-11+ @ 11:23 BST May 27

- SUP 1: 119-03 Low May 23

- SUP 2: 118-01+ Low May 18

- SUP 3: 117-18 Low May 11

- SUP 4: 116-21 Low May 9 and a bear trigger

Treasuries are trading at their recent highs. The contract has tested above the 50-day EMA, currently at 120-15+. A clear break of this average would pave the way for a climb towards the 122-00 handle. Gains are still considered corrective though and the primary trend direction remains down. Key support and the bear trigger is 116-21, May 9 low. Initial firm support has been defined at 118-01+, the May 18 low.

US EURODOLLAR FUTURES CLOSE

- Jun 22 +0.010 at 98.240

- Sep 22 steady at 97.495

- Dec 22 -0.010 at 96.995

- Mar 23 -0.005 at 96.860

- Red Pack (Jun 23-Mar 24) -0.025 to -0.005

- Green Pack (Jun 24-Mar 25) -0.02 to steady

- Blue Pack (Jun 25-Mar 26) +0.005 to +0.020

- Gold Pack (Jun 26-Mar 27) +0.030 to +0.030

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00828 to 0.82557% (+0.00086/wk)

- 1M +0.00214 to 1.06171% (+0.08814/wk)

- 3M +0.02300 to 1.59786% (+0.09143/wk) * / **

- 6M +0.01043 to 2.08614% (+0.00943/wk)

- 12M +0.01414 to 2.69571% (-0.03429/wk)

- * Record Low 0.11413% on 9/12/21; ** New 2Y high: 1.57486% on 5/26/22

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.83% volume: $81B

- Daily Overnight Bank Funding Rate: 0.82% volume: $252B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.78%, $955B

- Broad General Collateral Rate (BGCR): 0.79%, $368B

- Tri-Party General Collateral Rate (TGCR): 0.79%, $351B

- (rate, volume levels reflect prior session)

FED OVERNIGHT REPO OPERATION

NY Federal Reserve/MNI

NY Fed reverse repo usage slips to 2,006.688B w/ 99 counterparties vs. 2,007.702B prior session, compares to Monday's record high $2,044.658B.

FOREX: Equity Indices Boost Antipodean FX, EUR Underperforms

- Equity markets traded in more optimistic fashion on Friday, lending support to the likes of AUD and NZD. Additionally, there was more supportive price action for the Chinese Yuan with USDCNH retreating around 0.65% and negating Thursday’s advance.

- AUDUSD maintains a firmer short-term tone. The resumption of gains saw the pair rise to just below the 50-day EMA, at 0.7169 today. This average marks an important resistance and a clear break is required to further strengthen bullish conditions.

- Euro was the key laggard on to end the week, sitting marginally in the red after faltering from the overnight peak at 1.0765. Decent two-way price action in EURUSD throughout the session with some notable selling ahead of the WMR fix, potentially related to month-end. The boost in equities kept Eur/crosses on the backfoot.

- Pressure on the Euro kept the USD index from losing ground and remains unchanged for Friday. This week’s greenback weakness has seen the DXY narrowing in on the key 50-dma support, intersecting at 101.32

- Monday will focus on state-level German preliminary CPI figures during the European session before the Eurozone HICP flash estimate is released on Tuesday. US ISM Manufacturing PMI and NFP are the highlights of next week’s data calendar. The Bank of Canada decision is due Wednesday.

- It is worth noting Monday marks Memorial Day holiday in the US. Additionally, there will be UK bank holidays on Thursday and Friday for the Queen’s Jubilee.

Monday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/05/2022 | 0600/0800 | *** |  | SE | GDP |

| 30/05/2022 | 0600/0800 | ** |  | DE | Import/Export Prices |

| 30/05/2022 | 0700/0900 | *** |  | ES | HICP (p) |

| 30/05/2022 | 0700/0900 | * |  | CH | KOF Economic Barometer |

| 30/05/2022 | 0800/1000 | *** | | DE | Bavaria CPI |

| 30/05/2022 | 0900/1100 | *** | | DE | Saxony CPI |

| 30/05/2022 | 0900/1100 | ** |  | EU | Economic Sentiment Indicator |

| 30/05/2022 | 0900/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 30/05/2022 | 0900/1100 | * | | EU | Business Climate Indicator |

| 30/05/2022 | 1200/1400 | *** | | DE | HICP (p) |

| 30/05/2022 | 1230/0830 | * |  | CA | Current account |

| 30/05/2022 | 1500/1100 |  | US | Fed Governor Christopher Waller |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.