Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

Treasury 2s10s Yield Curve

Tsy 2s/10s Yield Curve

US TSYS: Markets Roundup: Paradigm Shift In Hike Expectations Post Bank Fails

- Surge in short end rates resumed as Silicone Valley Investment Bank collapsed late last week, followed by New York's Signature Bank on Sunday, the bank run on deposits continued to send shock waves across markets Monday.

- A paradigm shift from last week's rate hike expectations to rate cuts occurred as short end exploded higher: Fed terminal rate fell to 4.810 in May'23, down over 80bp for August late last week. Fed funds implied hike for Mar'23 at 18.7bp, May'23 cumulative 25.9bp to 4.819%, Jun'23 dipped to 13.4bp to 4.694%. Rate cuts start pricing in for Jul'23: -16.5 cumulative at 4.398%.

- In Treasuries, 2Y futures traded over a full point higher to 103-15.38, yield fell below 4.0% to 3.9889% low in the first half while yield curves bull steepened: 2s10s tapped -54.707 high -- nearly 50% higher than last week's four decade lows.

- Of note, Goldman Sachs and Barclays both revised their rate call to steady next week from +50bp prior.

- Despite sharply lower bank stocks on the day, US equities are modestly firmer in recent trade, the e-mini S&P futures near middle of the session range at 9818.0 (+21) below initial resistance of 3960.75 Low Mar 2.

- No data on the day, CPI tomorrow MoM (0.5% prior, 0.4% est); YoY (6.4%, 6.0%) while the Federal Reserve will remain in media blackout regarding monetary policy through March 23.

US

US: Core CPI inflation is seen holding a 0.4% M/M clip for the third month running in February. It is however expected to have been boosted by a bounce in used car prices rather than more broad-based pressure, especially in light of a sizeable easing in supply chain pressures.

- Core non-housing services will again be in focus after moderating to a mixed extent in January, whilst OER and primary rents inflation are seen slowing slightly further.

- Powell had last week opened the door to a 50bp hike at the March FOMC, arguably dented after Friday’s payrolls report showed softer wage pressures despite continued surprise strength for payrolls growth. That already seems like a long time ago: a historical fixed income rally on regional bank contagion fears now sees only one more 25bp hike for the cycle priced, after a 100bp drop in 2Y Tsy yields in three days.

CANADA

BOC: The BOC is poised for a long interest-rate pause with the demise of Silicon Valley Bank weighing on already clear signs that growth is slowing enough to pull inflation back to target, former central bank researcher and Conference Board of Canada Chief Economist Pedro Antunes told MNI.

- "The SVB collapse will worry central bankers and likely make them more cautious about raising rates further," Antunes said by email Monday.

- Bank of Canada Governor Tiff Macklem last week held the key rate at 4.5% after eight previous increases and underlined he's likely finished with inflation seen slowing to about 3% by mid-year and to the 2% target in 2024. Officials also said they could hike again if upside inflation risks were realized. (See: MNI BOC WATCH:Key Rate Stays 4.5%, Pause Affirmed As CPI Slows)

- Canada was already unique among G7 central banks in ending the hiking cycle and that optimism was justified by Canada's 1 million new immigrants over the past year boosting production capacity and the steep decline in the country's previously hot housing market, Antunes said. For more, see MNI Policy main wire at 1135ET.

EUROPE

ECB: President Lagarde has strongly guided the market to a 50bp hike in March and stressed that this would happen unless an extreme scenario materializes. Cleary the failure of Silicon Valley Bank (SVB) is an extreme event.

- With the fallout of SVB ongoing at the time of writing, and the situation fluid, the ECB’s prior pre-commitment for March is clearly in doubt.

- Absent any further communication from the ECB, we still expect the ECB to hike by 50bp in March given the persistence of underlying inflation and resilience of the euro area economy, but our conviction is much weaker at this point. Even if the ECB goes ahead as planned, the heightened uncertainty would preclude further explicit rate guidance beyond March For more see MNI Policy main wire at 1306ET.

OVERNIGHT DATA

No economic data next Monday, focus on Tuesday's CPI release:

- US Data/Speaker Calendar (prior, estimate)

- Mar-14 0600 NFIB Small Business Optimism (90.3, --)

- Mar-14 0830 CPI MoM (0.5%, 0.4%); YoY (6.4%, 6.0%)

- Mar-14 0830 CPI Ex Food and Energy MoM (0.4%, 0.4%); YoY (5.6%, 5.5%)

- Mar-14 0830 CPI Index NSA (299.17, 300.860)

- Mar-14 0830 CPI Core Index SA (302.702, 303.736)

- Mar-14 0830 Real Avg Hourly Earning YoY (-1.9% rev, --)

- Mar-14 0830 Real Avg Weekly Earnings YoY (-1.9% rev, --)

- Mar-14 1720 Fed Gov Bowman community bank event

MARTKETS SNAPSHOT

Key late session market levels:

- DJIA down 59.68 points (-0.19%) at 31870.6

- S&P E-Mini Future down 3.5 points (-0.09%) at 3896.5

- Nasdaq up 77.1 points (0.7%) at 11223.09

- US 10-Yr yield is down 13.7 bps at 3.5619%

- US Jun 10-Yr futures are up 40.5/32 at 114-13

- EURUSD up 0.0085 (0.8%) at 1.0728

- USDJPY down 1.59 (-1.18%) at 133.44

- WTI Crude Oil (front-month) down $2.18 (-2.84%) at $74.50

- Gold is up $42.89 (2.3%) at $1910.91

- EuroStoxx 50 down 132.99 points (-3.14%) at 4096.54

- FTSE 100 down 199.72 points (-2.58%) at 7548.63

- German DAX down 468.5 points (-3.04%) at 14959.47

- French CAC 40 down 209.17 points (-2.9%) at 7011.5

US TREASURY FUTURES CLOSE

- 3M10Y -0.814, -125.656 (L: -140.779 / H: -110.252)

- 2Y10Y +41.8, -47.583 (L: -82.037 / H: -47.395)

- 2Y30Y +55.812, -32.79 (L: -76.421 / H: -32.79)

- 5Y30Y +28.026, 1.856 (L: -22.235 / H: 2.221)

- Current futures levels:

- Jun 2-Yr futures up 1-03.25/32 at 103-13.25 (L: 102-10.375 / H: 103-15.375)

- Jun 5-Yr futures up 1-08.25/32 at 109-8.75 (L: 107-25.5 / H: 109-29.75)

- Jun 10-Yr futures up 1-10/32 at 114-14.5 (L: 112-21 / H: 115-13)

- Jun 30-Yr futures up 1-19/32 at 130-30 (L: 128-07 / H: 132-30)

- Jun Ultra futures up 24/32 at 141-16 (L: 138-14 / H: 146-03)

US 10YR FUTURE TECHS: Impulsive Bull Wave Extends

- RES 4: 116-28+ High Jan 19 and key resistance

- RES 3: 116-08 High Feb 2

- RES 2: 116-00 Round number resistance

- RES 1: 115-13 High Mar 13

- PRICE: 114-17 @ 16:44 GMT Mar 13

- SUP 1: 114-00 Round number support and the Feb 14 high

- SUP 2: 113-10 High Mar 10

- SUP 3: 112-31+ 50-day EMA

- SUP 4: 112-21 Low Mar 13

Treasury futures have started the week on a firm note as the contract extends last week’s strong impulsive gains through to the Monday close. A number of important Fibonacci retracement points have been cleared and 115-03+, the 76.4% retracement of the bear leg between Feb 2 - Mar 2, has been pierced. A clear breach of 115-03+ would signal scope for a climb towards the 116-00 handle next. Initial firm support lies at 112-31+, the 50-day EMA.

EURODOLLAR FUTURES CLOSE

- Mar 23 +0.271 at 95.134

- Jun 23 +0.550 at 94.975

- Sep 23 +1.060 at 95.675

- Dec 23 +0.945 at 95.845

- Red Pack (Mar 24-Dec 24) +0.190 to +0.750

- Green Pack (Mar 25-Dec 25) steady to +0.085

- Blue Pack (Mar 26-Dec 26) -0.025 to steady

- Gold Pack (Mar 27-Dec 27) -0.05 to -0.025

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00400 to 4.55714% (-0.00243/wk)

- 1M -0.00743 to 4.79857% (+0.08943/wk)

- 3M -0.01557 to 5.13814% (+0.15414/wk)*/**

- 6M -0.07157 to 5.42829% (+0.11158/wk)

- 12M -0.12515 to 5.73814% (+0.04371/wk)

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.15371% on 3/9/23

- Daily Effective Fed Funds Rate: 4.57% volume: $115B

- Daily Overnight Bank Funding Rate: 4.57% volume: $305B

- Secured Overnight Financing Rate (SOFR): 4.55%, $1.120T

- Broad General Collateral Rate (BGCR): 4.51%, $469B

- Tri-Party General Collateral Rate (TGCR): 4.51%, $461B

- (rate, volume levels reflect prior session)

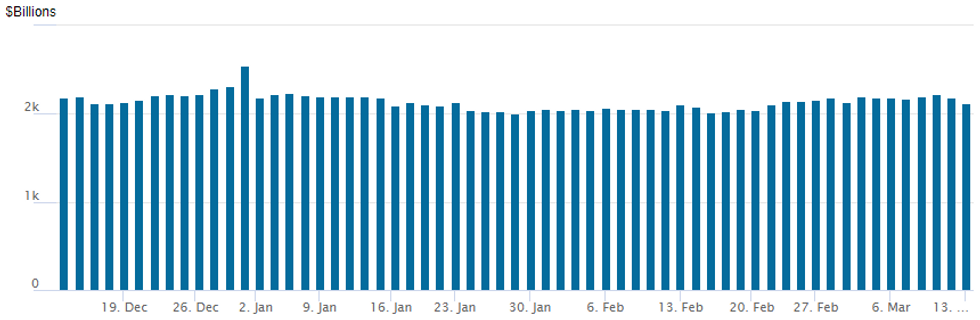

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,126.677B w/ 97 counterparties vs. prior session's $2,188.375B. Compares to Friday, Dec 30 record/year-end high of $2,553.716B (prior record high was $2,425.910B on Friday, September 30.

PIPELINE

No new corporate bond issuance, several interested parties withdrew bond sale plans due to market volatility tied to Silicone Valley Bank and Signature Bank collapse last Friday.

EGBs-GILTS CASH CLOSE: US Bank Panic Sparks Massive Short-End Rally

A global flight to safety and sharp downward repricing of ECB and BoE tightening expectations saw a historic rally across EGBs and Gilts Monday.

- With concerns over US banking stability mounting, the German curve bull steepened sharply, with Schatz yields seeing their biggest-ever drop (41bp, and 52bp at one point).

- March ECB implied hike pricing (our meeting preview is here) fell 8bp on the day, but rose from session lows of 33bp to just under 38bp after MNI's sources piece "ECB Clings To 50Bp Hike Plan Amid Market Turmoil".

- Around 80bp of hikes have been priced out of the ECB cycle altogether, including 50bp today (had been as much as 100bp intraday ), with terminal now seen at 3.38% vs 4.18% last week.

- Periphery spreads widened sharply, led by GGBs.

- The Gilt move was more limited from a historical standpoint given comparisons to last autumn's budget-related volatility, but 2Y yields dropped the most since October. BoE hike pricing dropped 37bp Monday, and is off 55bp since last Thursday (terminal Bank rate now seen at 4.36%).

- Further developments in US banks will be eyed overnight, with the focus of Tuesday's schedule being US CPI.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 40.7bps at 2.69%, 5-Yr is down 31.5bps at 2.328%, 10-Yr is down 24.9bps at 2.259%, and 30-Yr is down 19.2bps at 2.276%.

- UK: The 2-Yr yield is down 27.9bps at 3.363%, 5-Yr is down 24.8bps at 3.277%, 10-Yr is down 27bps at 3.37%, and 30-Yr is down 17.7bps at 3.835%.

- Italian BTP spread up 11.3bps at 192.4bps / Greek up 21.8bps at 204.4bps

FOREX: Greenback Pressure Extends Ahead Of US CPI, DXY Down 0.9%

- Despite equity markets stabilising throughout the US session on Monday, the substantial moves across fixed income markets and the related Fed re-pricing have continued to weigh on the greenback, with the USD index looking set to close with a 1% decline as we approach the APAC crossover.

- Punchy ranges have been witnessed across the G10 currency space, none more so than for USDJPY which printed a low of 132.29 from overnight highs of 135.08. Lower core rates and the associated narrowing of interest rate differentials key here. Despite a bounce into the close, USDJPY still resides down 1.15%.

- With more stable price action for equity markets in Monday’s US session, the Australian dollar has been able to capitalise on the broad greenback weakness, with AUDUSD now ~1.5% higher as we approach the APAC crossover. Despite this climb, the trend condition remains bearish for now and initial firm resistance remains defined at 0.6784, the Mar 1 high.

- Spot USD/CNH (-1.30%) is consolidating sharp losses on Monday. The pair briefly tried below its 50-DMA, intersecting today at 6.8373, which has underpinned price action since mid-February. A close under the March 01 low of CNH6.8634 would mark the completion of a double top formation, with the bearish theme being reinforced by a sustained move through the 50-DMA.

- Elsewhere in emerging markets, substantial volatility was seen in the Mexican peso, with USDMXN briefly spiking back above the 19.00 handle. The pair has advanced 2.25% on Monday and MXNJPY had been down as much as 5.3% at worst levels.

- Focus turns to Tuesday’s US inflation data, made more interesting by the plethora of Fed view changes for the March decision that have crossed the newsfeeds today.

Tuesday Data Calendar: CPI on Tap

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/03/2023 | 0700/0700 | *** |  | UK | Labour Market Survey |

| 14/03/2023 | 0800/0900 | *** |  | ES | HICP (f) |

| 14/03/2023 | 0900/1000 | * |  | IT | Industrial Production |

| 14/03/2023 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 14/03/2023 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 14/03/2023 | - |  | EU | ECB de Guindos at ECOFIN Meeting | |

| 14/03/2023 | 1230/0830 | ** |  | CA | Monthly Survey of Manufacturing |

| 14/03/2023 | 1230/0830 | *** | | US | CPI |

| 14/03/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 14/03/2023 | 1400/1000 | * | | US | Services Revenues |

| 14/03/2023 | 2120/1720 | | US | Fed Governor Michelle Bowman |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.