Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI BCB Preview

Executive Summary

- In line with prior guidance from the December statement, the Copom are widely expected to hike the Selic rate by another 150bps to 10.75%.

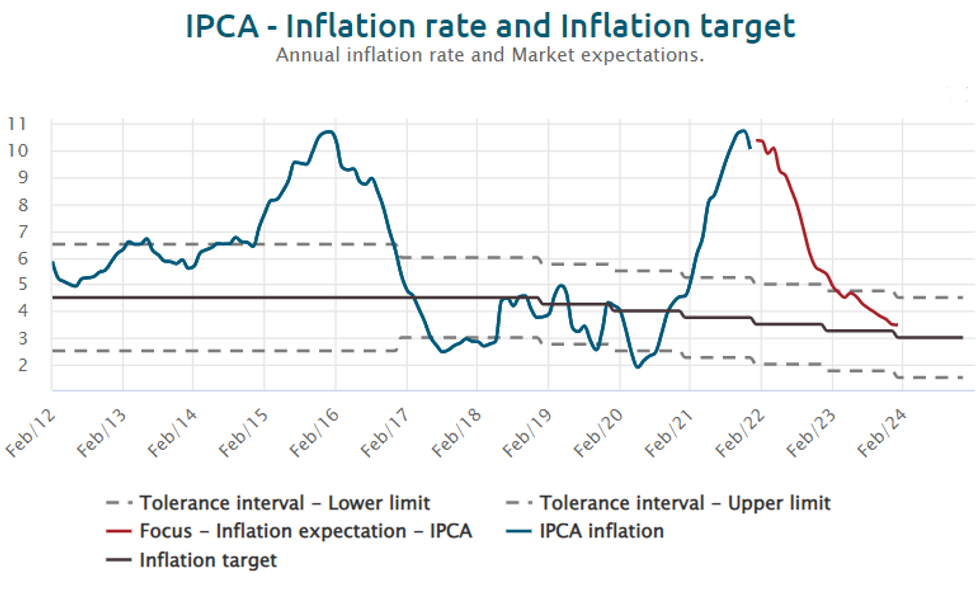

- Despite headline inflation decreasing from the 10.96% peak, pressures on inflation expectations remain and signals for further tightening should remain within the committee’s guidance.

- However, after a likely 875bps of hikes and a declining growth outlook, the Copom may indicate a potential deceleration in the pace of tightening going forward.

Click to view the full preview: MNI Brazil Central Bank Preview - Feb 2022.pdf

Forward Guidance Appears of Paramount Importance

At the December meeting, the Copom made their second consecutive 150bps rate hike and detailed that the committee “foresees another adjustment of the same magnitude” at the February meeting. JPMorgan highlight this to be “a pace that is exceptionally rapid by any historical and international standards”. While the consensus among analysts is for the BCB to stick to this mantra, there is also growing view for the central bank to give themselves optionality going forward, by not pre-committing with regard to the future magnitude of hikes. With this said, the persistence of inflation pressures, particularly in core and services components, has prompted some analysts such as Goldman Sachs to expect the Copom to “harden the language on inflation, and the balance of risks around it”.

Inflation Prints Continue to Surprise Estimates

The most recent IPCA inflation data for the first half of January showed the headline reading had continued to ease to 10.20% from 10.42%, however, both the monthly and annual prints were above the median analyst estimates. Indeed, the persistence of the inflationary pressures remain evident in the latest BCB Focus survey, where forecasts for 2022 year-end inflation were revised up to 5.38% and perhaps more significantly, to 3.5% in 2023, evidence of a further contamination of medium-term expectations.

Source: Brazil Central Bank

Source: Brazil Central Bank

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.