Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

MNI (London)

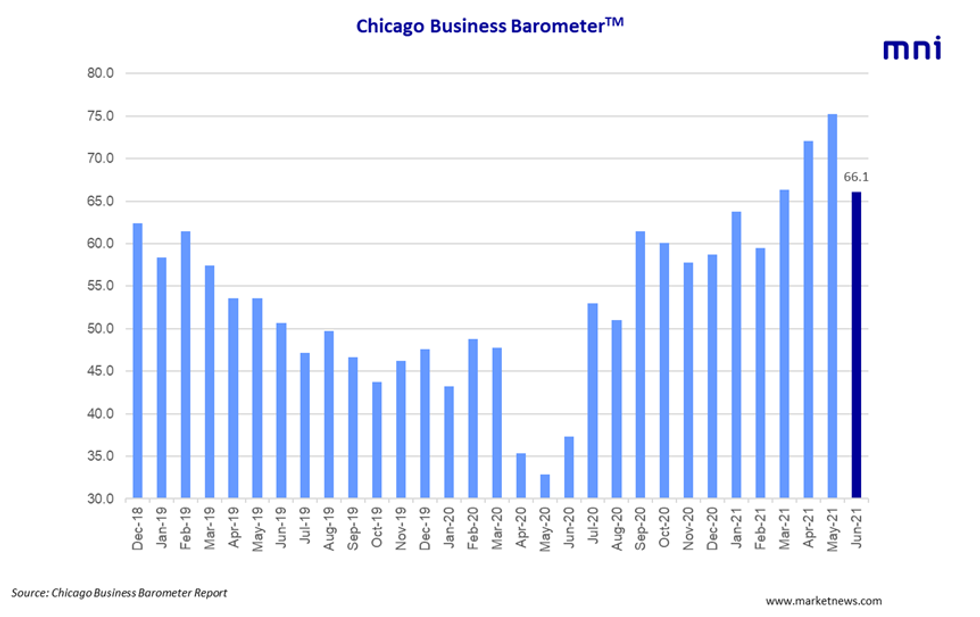

MNI CHICAGO BUSINESS BAROMETER 66.1 JUN VS 75.2 MAY

MNI CHICAGO BUSINESS BAROMETER 71.1 Q2 VS 63.2 Q1

MNI Q2 CHICAGO BUSINESS BAROMETER AT HIGHEST SINCE Q4 1973

MNI CHICAGO: ORDER BACKLOGS SHOWED LARGEST M/M DECLINE IN JUN

MNI CHICAGO: PRICES PAID AT HIGHEST SINCE DEC 1979

- The Chicago Business Barometer slipped to 66.1 in Jun, coming in weaker than markets expected (BBG: 70.0).

- Through Q2 the index surged 7.9 points to 71.1, its highest quarterly reading since Q4 1973.

- May's downtick was led by a sharp drop of Order Backlogs (66.6), followed by New Orders (66.7) and Production (60.0).

- While the quarterly avg. of New Orders (73.0) and Order Backlogs (73.5) increased markedly, Production (67.9) eased slightly in Q2.

- Employment shifted deeper into contraction at 44.0, with firms noting difficulties in finding staff.

- Supplier Deliveries (86.5) rose further in Jun, while the quarterly average surged to 81.7 in Q2, both recorded the highest levels since 1974.

- Factory gate prices (91.9) jumped to a 41-year high in Jun, pushing up the index (90.6) up to the highest level since Q4 1979 through Q2.

- The majority (82.1%) said their business decisions are impacted by the rising prices.

- Companies remained concerned about the ongoing supply chain problems such as freight issues, slow deliveries and material shortages.

- Nevertheless, the majority (41.0%) reported that their firms are thriving and growing.

MNI London Bureau | +44 203-865-3814 | irene.prihoda@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok