Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

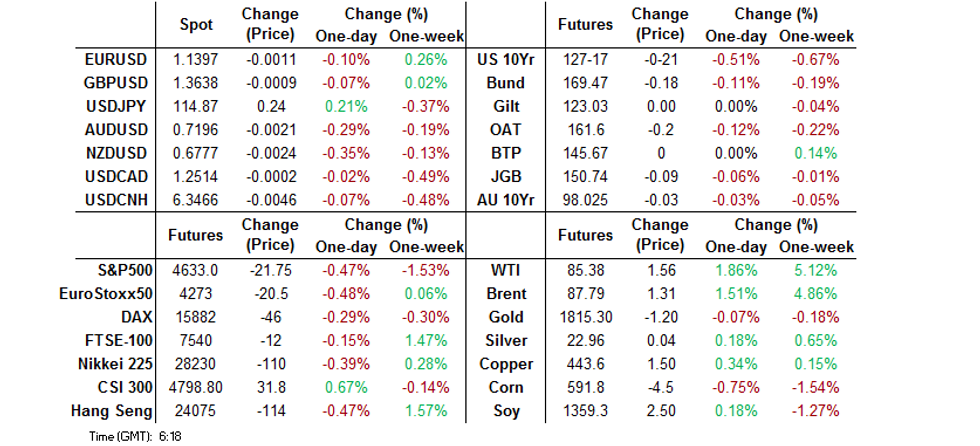

- U.S. Tsys retreat as cash trading resumes after a local holiday, weakness spills over into broader core FI space. 2-Year Tsy yield crosses above the 1% mark, while the curve bear flattens.

- A sudden upswing in U.S. Tsy yields bolsters the greenback, while sapping strength from the Antipodeans. The yen takes hit as BoJ communique fails to satisfy more hawkish watchers, with the Bank providing a broadly in-line statement.

BOND SUMMARY: Continued U.S. Tsy Sales Spill Over, Lack Of Hawkish BoJ Surprises Fails To Offer Reprieve

The Treasuries tumbled as cash trading resumed after a U.S. holiday, with voices pointing to a more aggressive policy tightening from the Fed growing louder still. Renewed weakness in U.S. Treasuries spilled over into the Asia-Pac core FI space, countering any potential impact of the BoJ's monetary policy decision announcement, as some of the more hawkish scenarios constructed based on recent source stories failed to materialise.

- Last week's RTRS piece noting that the BoJ were debating how to begin messaging an eventual (albeit not imminent) rate hike raised the perceived odds of the Bank dropping some hints re: potential departure from their ultra-loose policy stance. The statement contained no such indications, as the BoJ kept the main policy settings unchanged and altered their economic forecasts broadly in line with expectations. They upgraded the inflation projections for FY2022 & FY2023 and dropped their long-standing view that price risks are skewed to the downside, but struck some cautious notes on growth outlook and did not communicate any shift in policy. The decision came as local markets were shut for a lunch break, but JGB futures retreated once trading resumed, as post-BoJ musings failed to counter the spillover from retreating U.S. Tsys. JBH2 last trades at 150.80, 3 ticks shy of previous settlement, gradually edging away from its session low of 150.68. Cash JGB yields are marginally mixed as we type, off the slightly depressed levels seen in early trade. Focus turns to the press conference with BoJ Gov Kuroda, which may shed some more light on what we heard from the Bank today.

- T-Notes posted a fresh leg lower once the BoJ risk was out of the way, with cash Tsys taking a nosedive in tandem with the benchmark futures contract. TYH2 last changes hands -0-17+ at 127-20+, moving away from its session low of 127-15 over the last hour or so. Eurodollar futures run up to 7.5 ticks lower through the reds. Bear flattening remains evident in U.S. Tsy curve, with yields last seen 3.9-7.2bp higher, slightly off earlier highs & flats. The yield on 2-year notes punched crossed above the 1% mark, with fresh cycle highs also reached by 10-year (north of 1.85%) and 30-year (above 2.18%) yields. The U.S. docket is headlined by the monthly Empire Manufacturing Survey today.

- Offshore impetus was the primary driver of ACGBs in the absence of notable local catalysts. Aussie bond futures (YM last -4.0 & XM -3.5) followed in the footsteps of their major peers and have now moved away from lows printed in the wake of the downswing led by U.S. Tsys. Bills run 1-7 ticks lower through the reds. Cash ACGB yields trade 2.3-5.5bp higher across a flattened curve.

FOREX: Rising U.S. Tsy Yields Boost Greenback, Yen Retreats After BoJ Disappoints Hawks

The gauge of U.S. dollar strength (DXY) took a sudden upswing in sync with a jump in U.S. Tsy yields, with U.S. participants set to return to the market after a holiday. The moves have been attributed to continued hawkish chatter surrounding the most probable trajectory of Fed tightening.

- Firmer U.S. Tsy yields sapped strength from Antipodean currencies, key regional risk proxies. AUD/USD and NZD/USD each printed a fresh one-week low, with the former diving through the $0.7200 mark in the process. With the sudden upswing in U.S. Tsy yields pulling the rug from beneath the Antipodeans, they both gave up gains registered against JPY in the wake of the BoJ's monetary policy decision.

- The yen took a hit after the BoJ showed no appetite for tightening policy, even as RTRS last week reported that the Bank were debating how to begin communicating an eventual rate hike. Policymakers tipped hat to rising price pressures through expected upgrades to inflation forecasts & their assessment of risks to the price outlook, but they stopped short of offering any indications that they could start paring back stimulus anytime soon.

- Today's data highlights include UK jobs market data, German ZEW Survey, U.S. Empire Manufacturing Survey & Canadian housing starts. Speeches are due from ECB's Villeroy & Riksbank's Ingves, with BoJ Gov Kuroda set to hold a press conference.

FOREX OPTIONS: Expiries for Jan18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1250(E1.7bln), $1.1370-75(E566mln)

- USD/JPY: Y114.00($1.5bln), Y115.00($566mln), Y116.00-25($1.4bln), Y117.00($1.6bln)

- AUD/USD: $0.7200(A$882mln)

- USD/CNY: Cny6.3500($775mln), Cny6.4100($505mln), Cny6.65($1.0bln)

ASIA FX: Greenback Upswing Drives Most USD/Asia Higher But KRW & THB Hold Firm

A sudden upswing in U.S. Tsy yields provided a tailwind for the greenback, prompting USD/Asia crosses to erase earlier losses. The moves were attributed to continued hawkish Fed repricing, with U.S. markets set to re-open after a holiday.

- CNH: Spot USD/CNH fell to a fresh YtD low, with USD/CNY printing its worst levels since May 2018, but a round of fresh demand for the greenback prompted the pair to trim losses. Calls for cuts to China's benchmark loan prime rates grew louder, drawing more attention to Thursday's fixing, while the yuan reference rate was set virtually in line with expectations.

- KRW: South Korean won remained the best performer in the Asia EM basket, even as spot USD/KRW clawed back the bulk of its initial losses. The BoK called in their monthly report for a stronger monitoring of global capital flows and the FX market, as they see the won weakening despite strong economic fundamentals.

- IDR: Spot USD/IDR bounced back into positive territory, even as Indonesia lifted its ban on foreign arrivals. Participants eyed Bank Indonesia monetary policy decision, due Thursday.

- PHP: Spot USD/PHP narrowed in on resistance from Jan 10 cycle high of THB51.440 and peaked just shy of there.

- THB: Spot USD/THB stayed in negative territory despite the greenback-led bounce off session lows. The baht was bolstered by Thailand's push to reinstate its quarantine-free visa programme for vaccinated travellers.

- MYR: Malaysian markets were shut in observance of a public holiday.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/01/2022 | 0700/0700 | *** |  | UK | Labour Market Survey |

| 18/01/2022 | 1000/1100 | *** |  | DE | ZEW Current Conditions Index |

| 18/01/2022 | 1000/1100 | *** | | DE | ZEW Current Expectations Index |

| 18/01/2022 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 18/01/2022 | - |  | EU | ECB de Guindos at ECOFIN Meeting | |

| 18/01/2022 | 1315/0815 | ** |  | CA | CMHC Housing Starts |

| 18/01/2022 | 1330/0830 | ** |  | US | Empire State Manufacturing Survey |

| 18/01/2022 | 1500/1000 | ** | | US | NAHB Home Builder Index |

| 18/01/2022 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 18/01/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 18/01/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 18/01/2022 | 2100/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.