Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

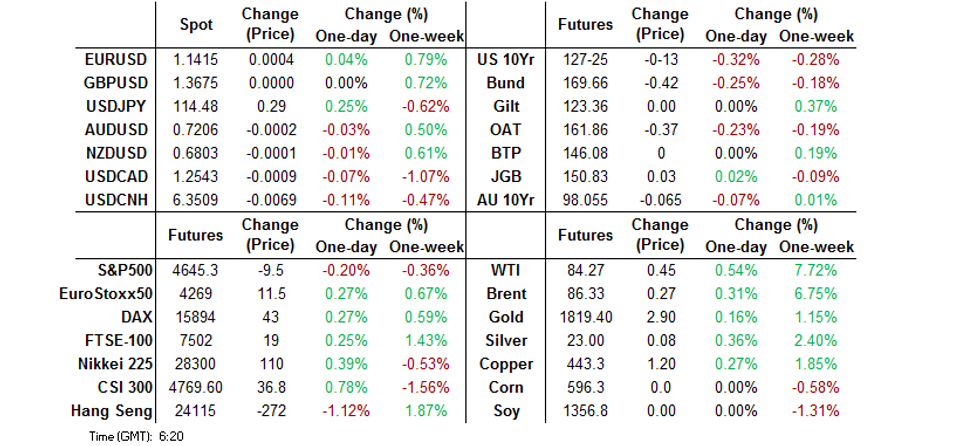

- PBOC cut the interest rates applied to 1-year MLF & 7-day reverse repo ops by 10bp apiece. It is the first time since Apr '20 when the former rate is lowered. Those expecting a move in rates as soon as today were in a minority, while the magnitude of the cut & the size of the liquidity injection provide further surprises.

- The yuan shows a muted reaction to PBOC steps on interest rates and only appreciates after the release of Chinese GDP/activity data, albeit in a gradual manner. Growth slows but still tops consensus, while activity indicators are a mixed bag.

- U.S. Tsys & ACGBs falter as market impetus from after Asia hours Friday spills over. JGBs' price action is somewhat erratic ahead of Tuesday's BoJ MonPol decision, while the yen lags all of its major currency peers.

BOND SUMMARY: U.S. Tsys & ACGBs Go Offered, JGBs Wobbly Ahead Of BoJ Meeting

Friday's upswing in U.S. Tsy yields spilled over into Asia in early trade, before the spotlight shifted to China, whose central bank cut the interest rates applied to 1-year MLF and 7-day reverse repo operations in a bid to stimulate economic growth. While speculation of imminent policy easing had been doing the rounds, the consensus view had been that the PBOC would leave these parameters unchanged today. Their moves came shortly before the release of China's Q4 GDP & December economic activity data, with the slowdown in growth proving less severe than forecast. The impact of Chinese goings-on may have helped prevent a recovery in U.S. Tsys & ACGBs after their initial spell of weakness.

- T-Notes extended their Friday rout before finding support at 127-20+ and stabilising in the Tokyo afternoon. TYH2 last changes hands -0-14 at 127-24. Eurodollar futures run 0.25-3.00 ticks lower through the reds. Cash Tsy markets won't re-open until Tuesday, as the U.S. observes a national holiday today.

- Cash ACGB yields sit 5.5-6.7bp higher across the curve, with bear steepening evident, albeit less pronounced than earlier in the session. Aussie bond futures have ticked away from lows but remain at depressed levels, YM -5.5 & XM -6.5. Bills trade 1-8 ticks lower through the reds. The Australian headline flow failed to offer much in the way of market catalysts, with initial price action seemingly driven by impetus from Friday's after-hours moves in U.S. Tsys.

- The Tokyo session saw somewhat erratic price action of JGBs, with participants preparing for the upcoming monetary policy decision from the BoJ. Policymakers will make their announcement on Tuesday and are expected to raise the FY2022 CPI forecast a tad, with potential for hawkish (by BoJ standards) tweaks in the language surrounding risks to the price outlook. Benchmark JGB futures rose after the re-open, topped out at 150.86 and retreated from there, extending their pullback after the lunch break. The contract sits at 150.79, 1 tick shy of previous settlement and off the session low of 150.73 printed in the wake of the aforementioned pullback. Cash JGB yields are mixed across the curve, with 10s outperforming. Another missile test conducted by North Korea, reports flagging potential for tighter Covid curbs in several Japanese prefectures and the proximity of a key policy speech from PM Kishida helped complicate the underlying risk environment.

FOREX: Yen Lags Major Peers On Eve Of BoJ Policy Announcement

The yen went offered on the eve of the BoJ's monetary policy decision announcement, despite speculation that it might see policymakers tone down their dovish rhetoric. The BoJ are widely expected to deliver a modest upgrade to their FY2022 CPI forecast on Tuesday. Meanwhile, source reports have suggested that policymakers may discuss tweaks to the language around risks to the price outlook, which might involve dropping the long-held view that they are skewed to the downside. Nonetheless, the yen landed at the bottom of the G10 pile as T-Notes extended their rout (cash Tsys did not trade), with the touted tweaks to the BoJ's rhetoric seemingly priced in.

- Spot USD/CNH crept higher but took a dive into negative territory when a slew of Chinese data hit the wires. The economic growth slowed in 4Q2021 but was better than expected and topped the government's official target. Elsewhere, December retail sales growth undershot median forecast, yet industrial output rose faster than anticipated.

- By the time China's data hit the wires, the PBOC cut the interest rates applied to their 1-year MLF (for the first time since Apr 2020) & 7-day reverse repo operations by 10bp each. Only a handful of economists expected the People's Bank to trim rates today, while even this minority group was generally surprised by the magnitude of the cuts and the size of the liquidity injection. Offshore yuan held steady despite China's growing policy divergence with the U.S.

- The global data calendar offers little of note during the remainder of the day, with U.S. markets shut in observance of a public holiday. The dearth of catalysts outside China translated into muted price action across G10 FX space overnight.

FOREX OPTIONS: Expiries for Jan17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1505-15(E657mln)

- USD/JPY: Y114.10-20($1.4bln), Y115.00($1.7bln), Y116.50($680mln)

- EUR/GBP: Gbp0.8410(E605mln)

- AUD/USD: $0.7285(A$577mln)

ASIA FX: USD/Asia Crosses Firm Amid Widening U.S.-China Policy Gap, Geopolitics Undermine KRW

All eyes were on China as the NBS released quarterly GDP figures and monthly economic activity data, while the PBOC slashed the interest rates applied to its 1-year MLF operations and 7-day reverse repo operations by 10bp apiece. On top of that, Friday’s after-hour USD purchases reverberated across the re-opening onshore markets in the region.

- CNH: Spot USD/CNH crept higher in early trade but pulled back (albeit in a gradual manner) after the data dump hit the wires. The economic growth slowed to +4.0% Y/Y in the final quarter of 2021 but topped median estimate of +3.3%, with YTD growth at +8.1% Y/Y, comfortably above the government's target of "over +6.0%." Industrial output grew faster than expected in December, but retail sales printed below consensus forecast, while the unemployment rate unexpectedly edged higher. Earlier in the session, offshore yuan showed muted reaction to interest-rate action from the PBOC, even as the outcome (in terms of the rate cuts, their magnitude, and the size of the liquidity injection) was more dovish than expected by most analysts.

- KRW: The South Korean won was the worst performer in Asia EM space, as North Korea conducted its fourth missile test this year, rubbing salt into the wounds of the risk-sensitive currency. The DPRK fired two suspected ballistic missiles eastwards from an airfield in Pyongyang, pouring fuel on a simmering regional geopolitical tension.

- IDR: Spot USD/IDR jumped after the re-open before trimming some gains, with Friday's after-hours move in U.S. Tsy yields being the main driver. Indonesia's trade surplus shrank way more than forecast in December, as the slowdown in exports growth proved more pronounced than expected.

- MYR: Spot USD/MYR followed a similar trajectory as USD/IDR, trimming its initial gains over the course of the Asia-Pac session. The local headline flow was fairly light.

- PHP: The Philippine peso remained on the back foot, as Cabinet Sec Nograles announced Friday that the current virus restrictions in Metro Manila will remain unchanged through the month-end. BSP Gov Diokno said Saturday that the Philippines can meet it inflation forecasts for 2022 & 2023 unless crude oil prices top $95/barrel.

- THB: Spot USD/THB stayed in positive territory, as domestic headline flow failed to offer much of real note.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/01/2022 | - |  | EU | ECB Lagarde & Panetta Eurogroup Meeting | |

| 17/01/2022 | 1330/0830 | * |  | CA | International Canadian Transaction in Securities |

| 17/01/2022 | 1400/0900 | * | | CA | Home Sales – CREA (Canadian real estate association) |

| 18/01/2022 | 0700/0700 | *** |  | UK | Labour Market Survey |

| 18/01/2022 | 1000/1100 | *** |  | DE | ZEW Current Conditions Index |

| 18/01/2022 | 1000/1100 | *** | | DE | ZEW Current Expectations Index |

| 18/01/2022 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 18/01/2022 | - | | EU | ECB de Guindos at ECOFIN Meeting | |

| 18/01/2022 | 1315/0815 | ** | | CA | CMHC Housing Starts |

| 18/01/2022 | 1330/0830 | ** |  | US | Empire State Manufacturing Survey |

| 18/01/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 18/01/2022 | 1500/1000 | ** | | US | NAHB Home Builder Index |

| 18/01/2022 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 18/01/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 18/01/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 18/01/2022 | 2100/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.