Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- A combination of Senator Manchin sinking Biden's BBB plan & a lockdown in the Netherlands (alongside increased prospects of deeper COVID restrictions across Europe & the UK) weighed on risk appetite in Asia.

- The PBoC cut its 1-Year LPR fixing by 5bp.

- Monday's docket lacks any notable tier 1 risk events.

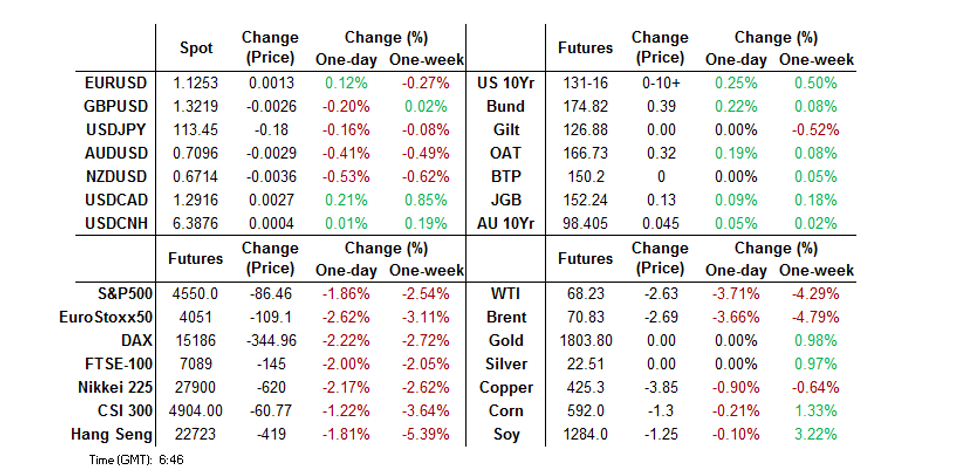

BONDS: Core FI Bid On U.S. Fiscal Woes & Omicron Worry

A combination of deeper omicron worry (centring on Europe, in the wake of a lockdown in the Netherlands & the UK, as speculation mounts re: circuit breaker restrictions after Christmas) and U.S. Democratic Senator Manchin’s move to effectively block President Biden’s Build Back Better scheme weighed on risk appetite in Asia, supporting core FI markets. Note that the PBoC’s latest 1-Year LPR fixing moved 5bp lower, surprising most economists. There isn’t anything in the way of notable tier 1 risk events slated during the remainder of Monday’s session, which will leave headlines & broader risk appetite at the fore.

- TYH2 is threatening a clean break above technical resistance at the Dec 3 high/bull trigger (131-16) into European hours, trading +0-11+ at on the day at typing, printing 131-17. Cash Tsys run 3.0-4.5bp richer, with 5s leading as the wings of the curve lag. Eurodollar futures have seen some bull flattening, running flat to 6.0bp firmer through the reds.

- JGB futures unwound their overnight losses, finishing Tokyo trade +13. Cash trade saw 7s lead the rally, with the major benchmarks running 0.5-1.5bp richer on the day. BoJ Governor Kuroda failed to introduce any new points of discussion in his latest address to parliament (stressing that now is not the time to normalise policy, pointing to outcome-based monetary policy re: inflation, as opposed to a date-based process).

- Aussie bond futures finished just shy of best levels, with YM +4.0 & +4.5. Cash ACGB trade saw most of the major benchmarks richen by 4-5bp. EFPs pushed wider on the day, with 3s leading the way. Bills were 2-4 firmer through the reds. Australian PM Morrison has called a snap National Cabinet meeting for Tuesday, with focus on the dissemination of up-to-date information on Omicron. It would seem that Morrison has played down the importance of the meeting. Note that various state & federal level officials sounded relatively relaxed re: the matter over the weekend, given the onset of the summer season & high vaccination rate in place in Australia.

FOREX: Omicron Worry & U.S. Fiscal Roadblock Weigh On Risk

Greater worry re: omicron (punctuated by a lockdown in the Netherlands and fears re: wider containment measures across Europe & the UK) coupled with U.S. Democratic Senator Manchin’s decision to effectively block President Biden’s Build Back Better plan dented risk appetite in Asia. The PBoC delivered a 5bp cut in its 1-Year LPR fixing (which took most by surprise, even after various state-owned media outlets ran commentary pieces alluding to chances of such a move in recent days) which failed to support risk appetite, even as Beijing tipped its hat further towards pro-growth policies.

- This left the JPY atop the G10 FX table, as you would expect in such an environment, although all of the major FX crosses held within their recently observed ranges.

- The combination of the dent in broader risk appetite and another monthly trade deficit for New Zealand weighed on the kiwi, which found itself at the bottom of the G10 FX pile. NZD/USD sits at ~$0.6720, ~30 pips softer on the day.

- The broader backdrop & some idiosyncracies weighed on GBP. Continued political woes for PM Johnson (the resignation of Brexit Minister Lord Frost, growing discontent with the PM from within his own party, trailing the Labour party in opinion polls & further signs of Tory officials, including himself, potentially flouting some of the COVID restrictions that have been in place) in addition to the prospect of announcements re: deeper COVID restrictions in the coming days (Health Sec. Javid did not rule out such a move before Christmas, while the Times has pointed to a 2-week circuit breaker post-Christmas, whereas the Telegraph pointed to the potential announcement of warnings for household mixing over the Christmas period) dominated weekend press reports.

- There isn’t anything in the way of meaningful economic data releases to note on Monday, which will leave headline flow/broader risk appetite at the fore.

FOREX OPTIONS: Expiries for Dec20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1250(E625mln), $1.1300(E916mln), $1.1335-55(E1.1bln), $1.1400(E1.4bln)

- USD/JPY: Y113.65-75($726mln), Y114.10-25($741mln), Y115.00($1.2bln)

- AUD/USD: $0.7100(A$686mln), $0.7200-05(A$1.6bln); $0.7240-50(A$1.5bln)

- USD/CAD: C$1.2800-20($690mln)

EQUITIES: Asia Provides Soft Start To The Week

The combination of U.S. Democratic Senator Manchin delivering a roadblock for President Biden’s Build Back Better scheme & increased omicron worry (centring on Europe & the UK) weighed on risk appetite during Asia-Pac hours. This pushed all of the major regional equity indices lower, adding to the burden of a negative lead from Wall St. The Nikkei 225 was the weakest index among the major regional benchmarks, shedding ~2%. Meanwhile, U.S. e-mini futures lost ~0.8-1.0%, trading below their respective Friday troughs in the process. A 5bp cut in the latest PBoC 1-Year LPR fixing failed to boost risk appetite.

GOLD: Hovering Around $1,800/oz

A flat start to the week for bullion, with spot last dealing just above the $1,800/oz mark, little changed on the day. Our weighted U.S. real yield monitor continues to hold a little shy of the levels observed around last week’s FOMC decision (which represented a multi-month high). Meanwhile, Friday saw the broader USD recover to trade a little shy of Wednesday’s peak, which applied pressure to gold. This meant that bulls failed to force a break of the initial technical resistance level at the Nov 26 high ($1,815.6/oz). Initial support is located at the bull channel base drawn off the Aug 9 low. Note that ETF holdings of gold have ticked back towards the recent lows, but still remain elevated by a historical standard.

OIL: Pressured By Omicron Worry & U.S. Fiscal Dynamic

Omicron worry (dominated by a lockdown in the Netherlands and the potential for a deepening of restrictions across broader Europe & the UK) weighed on crude to start the week, as demand fears notched higher. Meanwhile, U.S. Democratic Senator Manchin’s choice to effectively block President Biden’s Build Back Better scheme weighed further on risk appetite. This combination leaves WTI & Brent futures ~$2.50 below Friday’s settlement levels as of typing.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/12/2021 | 0900/1000 | ** |  | EU | EZ Current Acc |

| 20/12/2021 | 1100/1100 | ** |  | UK | CBI Industrial Trends |

| 20/12/2021 | 1630/1130 | * |  | US | US Treasury Auction Result for 13 Week Bill |

| 20/12/2021 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 20/12/2021 | 1800/1300 | * | | US | US Treasury Auction Result for Cash Management Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.