Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- A story surrounding a 3-month+ grace period for Evergrande re: the maturity of a bond issued by China Fortune Holdings (a JV that it guarantees bond holdings for), seemingly pressured risk, perhaps on a period of elongated uncertainty surrounding Evergrande matters, without a fix for the underlying problem.

- That allowed the JPY to move to the top of the G10 FX table overnight.

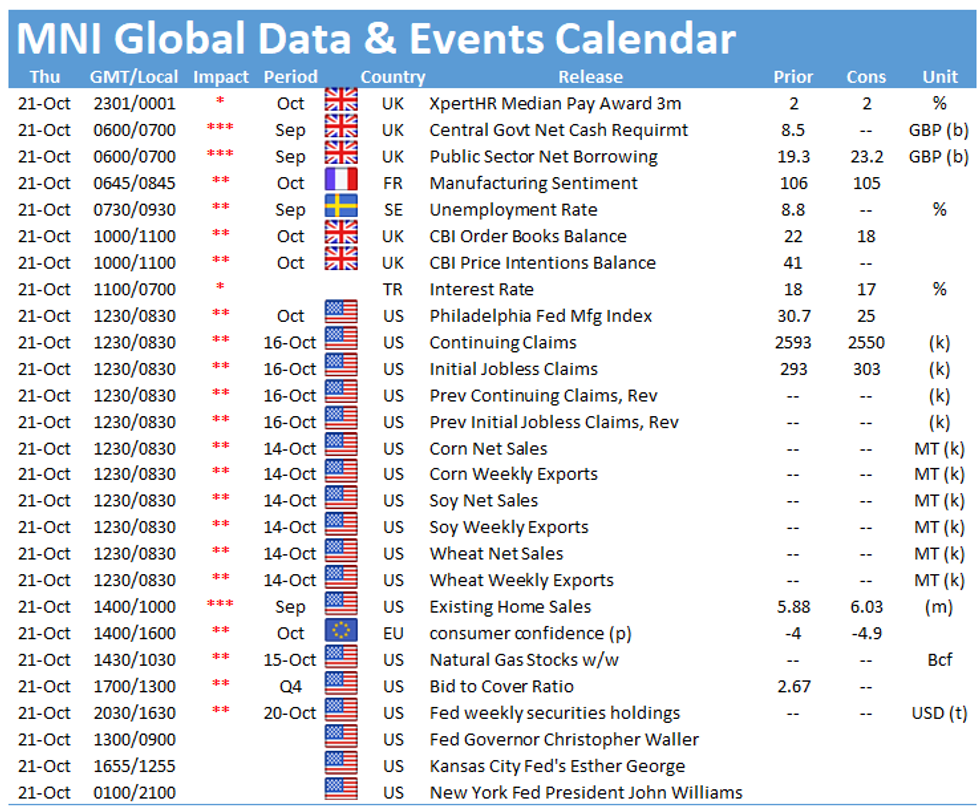

- U.S. weekly jobless claims, EZ consumer confidence and comments from Fed's Waller, ECB's Visco & Riksbank's Breman take focus Thursday.

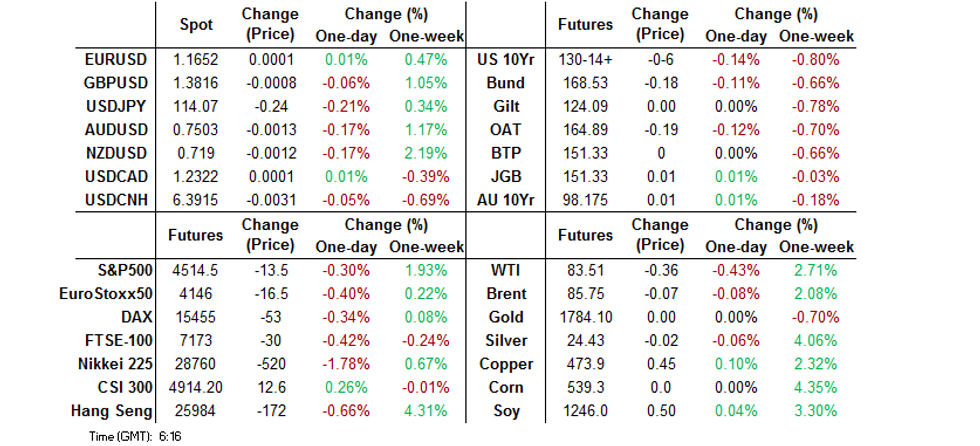

BOND SUMMARY: Off Lows On Wider Flows

Core FI markets have regained some poise in recent dealing after a bit of a drift lower in early Asia-Pac trade. The initial drift lower perhaps focused on yesterday's cheapening in the long end of the Tsy curve & ACGB dynamics.

- The bid seemingly came in after little-known news provider REDD noted that Evergrande Group secured an extension on the maturity of a $260mn bond issued by Jumbo Fortune Enterprises, the JV it is involved in and guarantees the bonds for. The article suggested that the extension period will last more than 3 months, citing sources. The defensive tone may just be a case of the market not liking the continued uncertainty that the 3-month+ grace period indicated in the article may create, as it isn't an ultimate fix to the issues at hand.

- TYZ1 last -0-05+ at 130-15, with some very modest twist flattening witnessed on the cash Tsy curve, although the major benchmarks sit within -/+0.5bp of Wednesday's closing levels. A 10K block buyer of TYZ1 129.50 puts headlined flow overnight. Weekly jobless claims data, the latest Philly Fed business outlook survey, 5-Year TIPS supply, the Tsy's month-end supply announcement and another address from Fed Governor Waller are all due on Thursday.

- JGBs futures were relatively insulated, holding within the confines of the overnight range, even as Japanese equities struggled and the JPY turned bid. Cash trade sees the major JGB benchmarks run little changed to 2bp richer across the curve.

- Over in Sydney YM +3.5 and XM +1.5. Earlier in the day, the RBA held off from enforcing its YCT mechanism, choosing not to purchase ACGB Apr-24 in today's typical purchase window. This weighed YM as some in the market were disappointed (we suggested that the previously flagged move from the RBA earlier this week limited the chances of such purchases today). ACGB Apr-24 traded above 0.16% in yield terms, a little over 6bp above the RBA's 0.10% target, before recovering. Elsehwere, semi issuance saw QTC price A$1.5bn of Aug '33 paper. The bid off lows in ACGBs was in play before the broader rally took hold.

JAPAN: Plenty To Note In Weekly International Security Flow Data

Japanese investors recorded a 7th consecutive week of net purchases of overseas bonds last week, showing little worry in the wake of the recent uptick in global bond yields (although major benchmarks are of course still subdued in a historical sense).

- Japanese investors recorded a 5th straight week of net purchases of foreign equities, although the latest week saw a very marginal round of net buying.

- Foreign investors broke a streak of 3 weeks of net sales of Japanese bonds, although the 4-week rolling sum of the measure remains comfortably in negative territory, holding around levels not seen since the onset of the COVID pandemic.

- Foreign investors recorded a second straight week of relatively large net purchases of Japanese equities, with the inflows perhaps surrounding the expectations re: PM Kishida's fiscal spending intentions.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | 1221.3 | 140.8 | 2996.1 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 64.7 | 119.2 | 836.2 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 623.9 | -705.8 | -3162.0 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | 960.1 | 1015.6 | 1414.5 |

FOREX: Risk Switch Flicked To Off, Yuan Defies Softer PBOC Fix

Risk-off flows swept across G10 FX space amid a fairly abrupt change in sentiment, with major crosses unwinding earlier moves, which coincided with a bout of equity weakness. Antipodean currencies turned into the main laggards in G10 FX space after printing fresh multi-month highs against the greenback earlier in the session.

- USD/CNH went offered amid initial greenback weakness, looking through another softer than expected PBOC fix, but almost erased those losses as risk-off flows kicked in.

- JPY jumped onto the top of the G10 pile as the Nikkei 225 retreated, while U.S. e-mini futures ticked lower.

- U.S. weekly jobless claims, EZ consumer confidence and comments from Fed's Waller, ECB's Visco & Riksbank's Breman take focus later in the day.

FOREX OPTIONS: Expiries for Oct21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1734-40(E1.4bln)

- EUR/GBP: Gbp0.8460(E610mln)

- USD/JPY: Y115.30($610mln)

- AUD/USD: $0.7470-75(A$726mln)

- NZD/USD: $0.6950(N$2.3bln)

- USD/CAD: C$1.2650($1.0bln)

- USD/CNY: Cny6.4300($505mln), Cny6.4400($1.2bln)

ASIA FX: USD/CNH Trims Wednesday's Gains, Rupiah Loses Ground

The yuan gained despite a weaker than expected PBOC fix, while Indonesian rupiah underperformed as local markets reopened.

- CNH: Offshore yuan looked through another softer than expected PBOC fix and appreciated, with USD/CNH giving away some of its yesterday's gains. China's central bank set their USD/CNY mid-point 14 pips above sell-side estimate, which was a smaller divergence than on Wednesday.

- KRW: The won was rangebound, even as South Korea's exports proved resilient, as per the report for the first 20 days of October.

- IDR: The IDR underperformed in Asia EM basket as onshore Indonesian markets reopened after a holiday, with participants awaiting a speech from BI Gov Warjiyo.

- MYR: The ringgit drew some modest support from firmer palm oil prices.

- THB: The baht operated in a familiar range, amid talk of speculative activity of foreign investors driving the currency's sell-off over the recent months.

- PHP: The peso traded marginally lower, with participants awaiting a briefing with central bank officials on Q3 inflation.

- TWD: USD/TWD extended losses after Taiwan reported an above-forecast surge in export orders.

EQUITIES: Focus On Chinese Property Developers

Thursday saw a relatively mundane early round of trade for the major equity indices in Asia.

- Pressure then crept in after little-known news provider REDD noted that Evergrande Group secured an extension on the maturity of a $260mn bond issued by Jumbo Fortune Enterprises, the JV it is involved in and guarantees the bonds for. The article suggested that the extension period will last more than 3 months, citing sources. The defensive tone may just be a case of the market not liking the continued uncertainty that the 3-month+ grace period indicated in the article may create, as it isn't an ultimate fix to the issues at hand.

- Outside of that story there was plenty of focus on the Chinese property developer space. China Evergrande & Hopson both filed resumption of trading notices on the HKEx. This comes after news that the potential sale of the former's property services unit to the latter had collapsed, increasing pressure on the giant as the countdown to official default on its debt continues to tick over. Evergrande lost ~10% on the day, while Hopson added ~5%. Elsewhere in the sector, property developer Modern Land China suspended trading in Hong Kong pending the release of inside information after noting that it continues to face "liquidity issues." Finally, Fitch placed 29 Chinese property developers on UCO after a criteria update.

- U.S. e-minis sit a touch lower, which came in the wake of a modest uptick for both the S&P 500 & the DJIA on Wednesday. The NASDAQ 100 lost a little bit of ground on Wednesday as most of the U.S. Tsy curve cheapened on the day, although the tech index finished off of worst levels.

GOLD: Supported, With Bulls Looking To Key Resistance

The broader DXY is threatening a clean break below Monday's lows, while our weighted U.S. real yield monitor is holding on to most of yesterday's losses. These factors supported bullion on Wednesday, with relatively sedate trade subsequently witnessed in Asia hours, leaving spot a handful of dollars higher, just above $1,785/oz. Bulls still need to take out the October 14 high ($1,800.6/oz), which forms key short-term resistance, before they can turn their focus higher.

OIL: Little Changed In Asia, Fresh Cycle Highs Hit

WTI & Brent crude futures are little changed during Asia-Pac dealing after registering fresh cycle highs early in the session. News flow has been relatively light overnight, with a very modest downtick in U.S. e-mini equity futures perhaps helping crude away from highs.

- This comes after a rally on Wednesday, which saw the space receive support from a surprise headline drawdown in crude stockpiles per the DoE, which was accompanied by a drawdown in stocks at the Cushing hub and larger than expected drawdowns in both gasoline & distillate stocks, in addition to a downtick in weekly crude production (providing a more bullish outcome than Tuesday evening's inventory estimates from the API).

- An uptick in the S&P 500 also supported crude, while the Saudi Energy Minister played down chances of: an imminent, larger than pencilled in rise in crude production for OPEC+.

- Elsewhere, there was a call for continued upside in crude prices from the Iraqi oil minister (pointing to the potential for $100/bbl prices in Q1/Q222).

- These factors allowed crude prices to reverse their early losses on Wednesday, resulting in the aforementioned cycle highs.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.