Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

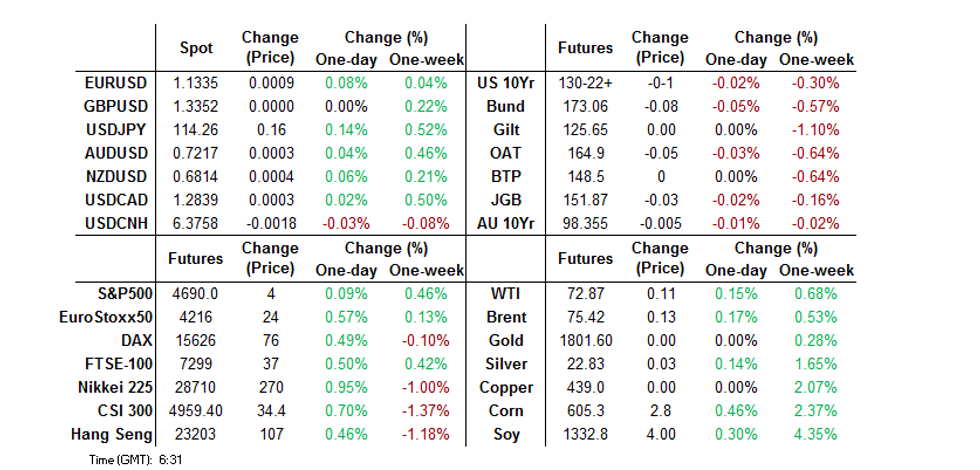

- Equities nudge higher in Asia, on spill over from Wednesday's NY session.

- Broader volume and price action was limited ahead of the Christmas break, with limited headline flow further crimping activity.

- North American data headlines the broader docket on Thursday.

BONDS: Core FI Little Changed Overnight

Participants are understandably unwilling to take on risk ahead of Thursday’s U.S. data releases and the Christmas break, with limited headline flow also noted, resulting in limited ranges and volume when it came to Tsy trade in Asia. TYH2 last unch. at 130-23+, operating in a 0-02+ range on ~28K lots, while cash Tsys are ~0.5bp cheaper across the curve. U.S. hours will see the release of the PCE suite, durable goods data, weekly jobless claims, existing home sales and final UoM sentiment readings.

- RTRS sources noted that “Japan plans to issue Y4.2tn of 40-Year JGBS, a 17% increase that comes even as the government plans to cut its bond issuance overall.” The sources noted that the move reflects “solid demand from life insurers at the long end of the yield curve.” The report notes that the increased issuance of 40-Year paper will come via a Y100bn uptick in auction size on a bi-monthly basis, as opposed to more frequent issuance. Elsewhere, the piece pointed to an uptick in 10-Year issuance and a reduction in 2-Year supply. The piece suggested that total JGB issuance for the next FY will be somewhere in the region of Y200tn, down ~Y20tn vs. the current FY. There will also be a modest uptick (~Y600bn) in liquidity enhancement auctions during the next FY. That dynamic, coupled with a soft cover ratio at the latest liquidity enhancement auction covering 15.5- to 39-Year JGBs, promoted some twist steepening of the cash curve, with 20+-Year yields rising by ~1bp. JGB futures showed through their Wednesday/overnight trough in early Tokyo dealing, before recovering some poise. The weakness in the longer end of the curve then applied some pressure, meaning the contract hit the bell -3.

- Aussie bonds oscillated within a tight range, with YM closing -1.0 and XM -0.5. A late, modest bid crept in as NSW confirmed that a mask mandate for indoor public venues will be reintroduced in the state as of tomorrow, along with new density limits in venues.

JAPAN: Bonds Continue To Dominate Weekly International Security Flow Data

The latest round of weekly international security flow data revealed that Japanese investors reverted to selling foreign bonds, racking up over Y1.0tn of sales for the third time in four weeks (note that the previous week saw a ~Y450bn round of net purchases). The latest week represented the largest round of net weekly sales of foreign bonds witnessed since February.

- Foreign investors lodged a third consecutive sizeable round of weekly net purchases when it came to Japanese bonds (~Y1.25tn), with the 4-week rolling sum of the measure moving to levels not witnessed since late ’18 in the process.

- Equity flows on both sides of the ledger maintained their respective trends, with the respective net weekly flows operating shy of their recent extremes.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -1588.5 | 458.9 | -3645.2 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 247.4 | 196.2 | 1763.6 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 1251.8 | 1157.6 | 3963.1 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | -841.3 | -604.3 | -1830.9 |

FOREX: Tight Asia Trade Observed, North American Data Eyed

A lack of meaningful news flow & the proximity to the Christmas break combined to result in a lacklustre round of Asia-Pac trade.

- EUR sits at the top of the G10 FX table, challenging Wednesday’s high at typing, but EUR/USD is less than 15 pips higher on the day.

- USD/CNH looked through a softer than expected USD/CNY mid-point fixing.

- The major USD crosses are effectively unchanged.

- Thursday’s U.S. data dump will be headlined by the PCE suite and durable goods print, while the latest round of monthly Canadian GDP data will also cross.

EQUITIES: Equities Nudge Higher In Asia

A lacklustre round of Asia-Pac trade saw the major regional equity indices and e-minis trade flat to a touch higher (the benchmarks print unch. to +0.5% at typing), with the space aided by Wednesday’s rally on Wall St., which stemmed from positive developments when it comes to the broader fight against COVID. Still, a lack of notable headline flow and thinner pre-Christmas markets limited broader activity.

GOLD: U.S. PCE Eyed

Gold trades little changed on the day, just above $1,805/oz, after reclaiming the $1,800/oz level on Wednesday. To recap, Wednesday saw the metal draw support from a downtick in both the broader DXY & U.S. real yields. The immediate technical parameters are well defined and remain untouched. Initial resistance comes in at the Nov 26 high/near-term bull trigger ($1,815.6/oz), while support is seen at the bull channel base drawn off the Aug 9 low. U.S. PCE data provides Thursday’s major macro release.

OIL: A Touch Above Wednesday’s Settlement Levels

WTI & Brent crude futures sit ~$0.20 above their respective settlement levels, holding to sub-$0.50 ranges in Asia, with a lack of notable headline flow apparent ahead of the Christmas break.

- South Korea presented the details re: its short-term commitments under the well-documented joint strategic oil inventory release that some of the major oil consuming nations are deploying, but this had no impact on prices.

- A reminder that Wednesday saw the benchmark contracts draw support from positive news surrounding the broader omicron situation and a larger than expected drawdown in headline U.S. crude stockpiles in the weekly DoE inventory data

- The next OPEC+ meeting provides a focal point in early ’22 (scheduled for January 4).

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/12/2021 | 0800/0900 | *** |  | ES | GDP (f) |

| 23/12/2021 | 0900/1000 | ** |  | IT | ISTAT Business Confidence |

| 23/12/2021 | 0900/1000 | ** | | IT | ISTAT Consumer Confidence |

| 23/12/2021 | 1330/0830 | ** |  | US | Jobless Claims |

| 23/12/2021 | 1330/0830 | ** | | US | Durable Goods New Orders |

| 23/12/2021 | 1330/0830 | ** | | US | Personal Income and Consumption |

| 23/12/2021 | 1330/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 23/12/2021 | 1330/0830 | * | | CA | Payroll Employment |

| 23/12/2021 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 23/12/2021 | 1400/1500 | ** |  | BE | BNB Business Sentiment |

| 23/12/2021 | 1500/1000 | *** | | US | Final Michigan Sentiment Index |

| 23/12/2021 | 1500/1000 | *** | | US | New Home Sales |

| 23/12/2021 | 1500/1000 | * | | US | US Bill 08 Week Treasury Auction Result |

| 23/12/2021 | 1500/1000 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 23/12/2021 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 23/12/2021 | 2130/1630 | ** | | US | Fed Weekly Money Supply Data |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.