Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The RBA Governor stressed the Bank’s ability to wait when it comes to rate hikes given broader uncertainties and a lack of worry re: runaway inflation. He noted that a rate hike in ’22 is plausible, as is a scenario whereby lift-off is 1 year+ down the line (while stressing that he “struggles” with the degree of tightening priced into markets at present). Lowe underscored the idea that the RBA’s goals are now in sight, while pointing to wage growth of 3% in ‘23, alongside the need for the Bank to monitor a wider array of wage metrics owing to the varied renumeration practices observed in tight labour markets.

- U.S. ADP employment change, flash Eurozone CPI as well as comments from BoC's Macklem & Gravelle will take focus on Wednesday.

BOND SUMMARY: RBA Looks For More Patience Than Rates Markets Price

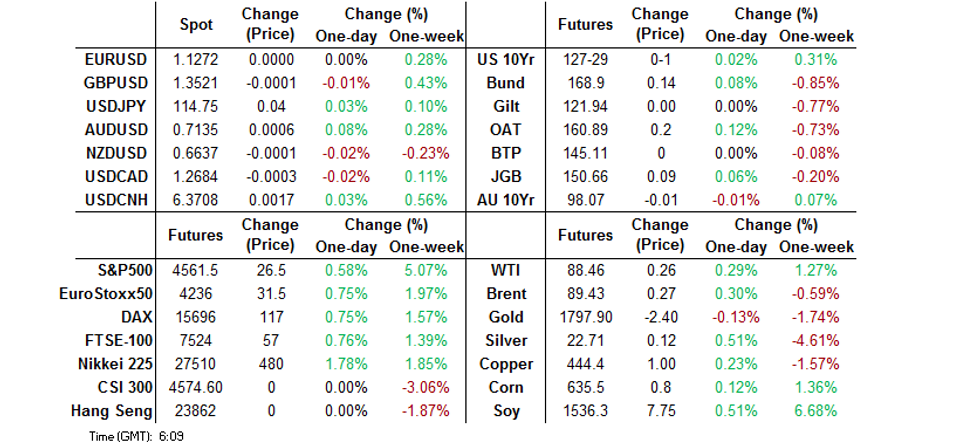

TYH2 stuck to a narrow 0-04+ range overnight, last +0-01 at 127-29 on light volume of 45K (impacted by the ongoing observance of the LNY holiday period across major financial centres in Asia and a related lack of macro headline flow). Cash Tsys run flat across the curve. NY hours will see the latest ADP employment print, in addition to the release of the quarterly Tsy refunding announcement.

- JGBs firmed during the Tokyo morning, with futures printing through their overnight high, before paring back from best levels, hitting the bell +8. The bid looked to be futures led, with 7s outperforming in cash trade, where the major benchmarks run flat-1.0bp richer on the session, while the long end lagged a little ahead of tomorrow’s 30-Year JGB issuance. The fact that 5s failed to test the 0% mark and backed off (a little) also supported the space. The BoJ carried out the previously outlined BoJ Rinban operations, with sizes of the respective purchases unchanged, with the following offer/cover ratios observed: 1- to 3-Year: 2.26x (prev. 1.61x), 3- to 5-Year: 2.01x (prev. 2.43x), 10- to 25-Year: 2.05x (prev. 3.19x).

- RBA Governor Lowe’s heavily awaited address allowed the ACGB space to correct from early Sydney lows. The Governor stressed the Bank’s ability to wait when it comes to rate hikes given broader uncertainties and a lack of worry re: runaway inflation. He noted that a rate hike in ’22 is plausible, as is a scenario whereby lift-off is 1 year+ down the line (while stressing that he “struggles” with the degree of tightening priced into markets at present). Lowe underscored the idea that the RBA’s goals are now in sight, while pointing to wage growth of 3% in ‘23, alongside the need for the Bank to monitor a wider array of wage metrics owing to the varied renumeration practices observed in tight labour markets. YM & XM finished -1.0 on the day, with the Bill strip twist steepening, +3 to -3 through the reds.

AUSSIE BONDS: The AOFM sells A$1.0bn of the 1.00% 21 Nov '31 Bond, issue #TB163

The Australian Office of Financial Management (AOFM) sells A$1.0bn of the 1.00% 21 November 2031 Bond, issue #TB163:

- Average Yield: 1.9267% (prev. 1.6800%)

- High Yield: 1.9275% (prev. 1.6800%)

- Bid/Cover: 3.2250x (prev. 4.4830x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 83.6% (prev. 70.4%)

- Bidders 42 (prev. 42), successful 14 (prev. 9), allocated in full 5 (prev. 1)

FOREX: Antipodean Divergence Unfolds In Muted Asia Trade

Major USD pairs stuck to tight ranges in muted Asia-Pac trade, as Lunar New Year holidays in major regional financial centres continued to weigh on activity. The DXY struggled for any topside impetus, operating in close proximity to yesterday's low.

- The Aussie dollar outperformed, showing some limited volatility as participants reacted to remarks from RBA Gov Lowe. AUD/USD crept higher ahead of Lowe's address, but eased off as his scripted comments reaffirmed the Bank's patient stance. The rate then posted a short-lived uptick as the official flagged the possibility of a cash rate hike this year, while pointing to a multitude of uncertainties ahead. The rate hovers just above neutral levels as we type, north of broken resistance from Jan 7 low of $0.7130.

- The kiwi dollar underperformed, with little in the way of initial reaction to New Zealand's Q4 jobs data. The unemployment rate dropped to an all-time low, indicating continued tightness in the labour market. Employment grew slower than forecast, but still marked the fifth consecutive quarter of steady increases. ASB altered their RBNZ call and now see the OCR peaking at 2.75% (prev. 2.00%) in early 2023, following a "steady pace of 25bp hikes" at each MPC meeting.

- U.S. ADP employment change, flash EZ CPI as well as comments from BoC's Macklem & Gravelle will take focus later in the day.

FOREX OPTIONS: Expiries for Feb02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1200(E520mln), $1.1240(E589mln)

- USD/JPY: Y113.25($600mln), Y114.35-50($840mln), Y115.00($793mln), Y115.50($761mln), Y116.00($1.2bln)

- GBP/USD: $1.3545-50(Gbp504mln)

- AUD/USD: $0.7050(A$506mln), $0.7250(A$563mln)

- USD/CAD: C$1.2500($711mln)

ASIA FX: Peso Lags On Philippine M'fing PMI Print

Many Asian financial centres remained shut for Lunar New Year holidays, limiting liquidity in Asia EM FX space.

- CNH: Offshore yuan remained comfortably within yesterday's range, as Lunar New Year holiday translated into a dearth of catalysts.

- IDR: The rupiah appreciated sharply, catching up with recent greenback sales, as onshore Indonesian markets re-opened after a holiday. Bank Indonesia Gov Warjiyo reaffirmed familiar stance on policy outlook, before January data showed that CPI inflation accelerated to +2.18% Y/Y, in line with expectations.

- PHP: The Philippine peso went offered as IHS Markit PMI data showed that expansion in the local manufacturing sector ground to a halt in January, owing to the surge in Covid-19 cases and the impact of typhoon Odette.

- THB: Spot USD/THB clawed back its initial losses, albeit domestic headline flow failed to provide much in the way of notable catalysts.

EQUITIES: Equities Tick Higher Overnight

The positive lead from Wall St., better than expected earnings from tech giant Alphabet and a lack of liquidity facilitated a move higher in the major regional equity indices that were open during Asia-Pac hours. The Nikkei 225 & ASX 200 added over 1.0% apiece as a result.

- E-minis were flat to 1.0% higher, with the NASDAQ 100 contract leading the way in the wake of Alphabet’s firmer than expected earnings, which was supplemented by a better-than-expected earnings release from AMD. The DJIA contract likely lagged on the back of rotational flows.

GOLD: Glued To $1,800/oz

Gold continues to oscillate around the $1,800/oz mark, with a lack of meaningful macro headline flow evident during Asia-Pac hours. More broadly, U.S. Fed policy & the geopolitical tension centred on Russia & Ukraine provide the short term headline risk factors, while Friday’s U.S. NFP presents the immediate event risk.

OIL: Crude Holding Shy Of Recent Highs

A tech-driven uptick in e-minis supported broader risk appetite during Asia-Pac hours, which allowed WTI & Brent futures to add a little over $0.30 apiece to settlement levels.

- Reports covering the latest weekly round of U.S. API crude inventory estimates pointed to a surprise drawdown in headline crude stocks, a drawdown in stocks at the Cushing hub, a larger than expected build in gasoline stocks and a slightly wider than expected drawdown in distillate stocks. The net impact of the report was virtually non-existent when it came to crude prices.

- Oil continues to oscillate just shy of the recent cycle highs, with today’s focus falling on the weekly DoE inventory data out of the U.S. and the latest OPEC+ gathering. A quick reminder that OPEC+ is expected to stick to the pre-prescribed cumulative 400K bpd lift in joint production in March come the end of today’s virtual gathering. Questions continue to circle re: the ability of certain participating nations when it comes to fulfilling increased production quotas, with some already failing to pump the maximum permitted amount.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/02/2022 | 1000/1100 | *** |  | IT | HICP (p) |

| 02/02/2022 | 1000/1100 | *** |  | EU | HICP (p) |

| 02/02/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 02/02/2022 | 1315/0815 | *** | | US | ADP Employment Report |

| 02/02/2022 | 1330/0830 | * |  | CA | Building Permits |

| 02/02/2022 | 1500/1000 | ** | | US | Housing Vacancies |

| 02/02/2022 | 1500/1000 | | CA | BOC Deputy Gravelle Speaks On Swaps Panel | |

| 02/02/2022 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 02/02/2022 | 2000/1500 | | CA | BOC Gov Macklem Testifies At Parliamentary Committee | |

| 03/02/2022 | 2200/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.