Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Asia markets feel the impact of above-forecast U.S. CPI data released Friday, with participants adding hawkish FOMC bets.

- China reports upticks in COVID-19 cases in Beijing and Shanghai, with resultant partial re-opening unwind weighing on sentiment.

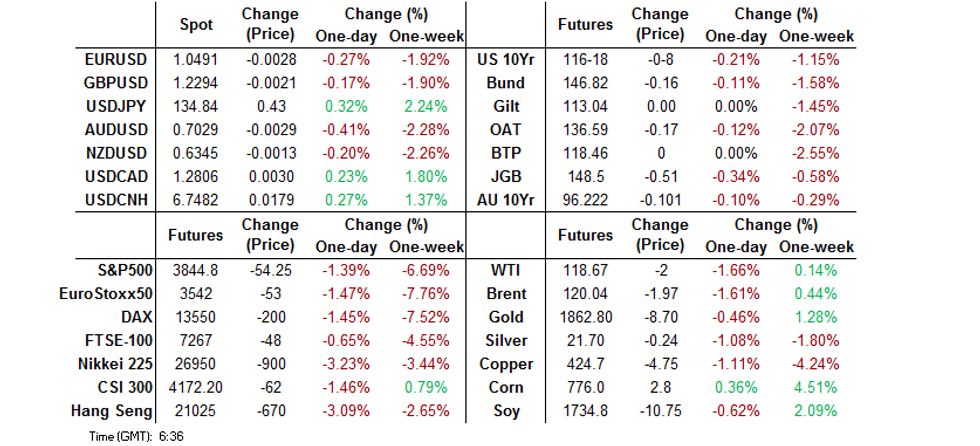

- USD/JPY breaks above Y135.00 and prints best levels since 1998. JGBs retreat ahead of Friday's BoJ meet. 10-Year JGB yield breaches the BoJ's 0.25% cap, prompting the central bank to step up bond buying.

BOND SUMMARY: U.S. 2-/10-Yr Tsy Yield Spread Nears Zero, Super-Long End Leads JGB Curve Steepening

Regional reaction to above-forecast U.S. CPI figures released after hours Friday applied further pressure to core FI space, with participants adding hawkish FOMC bets. Benchmark futures contracts extended losses despite risk-negative COVID-19 headlines out of China, where Beijing and Shanghai unwound some of their recent re-opening on the back of rising case counts.

- T-Notes extended their post-CPI sell-off and last trade -0-11+ at 116-14+, hovering near session lows, with Eurodollar futures running 3.0-19.5 ticks lower through the reds. Cash Tsy curve bear flattened, with 2-Year yield last 10bp higher. U.S. 2-Year/10-Year Tsy yield spread faltered towards zero, raising the prospect of an imminent yield curve inversion. Comments from Fed's Brainard (she will speak on the Community Reinvestment Act) take focus from here, while Wednesday's FOMC monetary policy decision headlines the local docket for the week.

- JGB futures softened as regional players caught up with U.S. consumer inflation data published after Asia hours Friday. JBU2 last changes hands at 148.51, down 50 ticks from previous settlement, close to session lows. Cash curve bear steepened, with the super-long end leading declines. Cheapening impetus is putting the BoJ's YCC framework to a test, with 10-Year yield trading close to the 0.25% ceiling. With the 10-Year/30-Year spread widening to multi-year highs, some are suggesting that the BoJ could buy longer-dated debt to step up enforcement of the YCC. The Bank is due to wrap up its monetary policy meeting on Friday.

- Australian financial markets were closed in observance of a public holiday.

JGBS: Futures Rebound On BoJ Stepped Up YCC Enforcement, Pull Back As Kuroda Sticks To Usual Script

Benchmark JGB futures have bounced from session lows (148.42) as the BoJ stepped up efforts to enforce its 0.25% ceiling on 10-Year yield, offering to buy an additional Y500bn of 5- to 10-Year JGBs on Tuesday.

- The announcement came as 10-Year JGB yield breached 0.25%, rising to its highest levels since January 2016.

- JGB futures last trades at 148.52, 49 ticks below previous settlement, pulling back from post-BoJ highs as BoJ Gov Kuroda reiterated the intention to stick with powerful monetary easing.

- Cash JGB yields sit higher, curve runs steeper as speculation that the central bank may eventually have to buy longer-dated debt has weighed on the super-long end. 10-Year JGB yield remains above 0.25% as we type.

FOREX: Yen Tumbles Past Another Round Figure Despite Risk Aversion

The psychologically important Y135.00 level gave way to rallying USD/JPY as (1) U.S. Tsy yields advanced after the release of firmer-than-expected U.S. CPI figures on Friday, (2) participants showed confidence in the dovish resolve of Mr Kuroda et al. ahead of this week's FOMC/BoJ monetary policy meetings, and (3) a senior lawmaker from Japan's ruling LDP helped reduce the credibility of verbal interventions by top financial officials.

- Spot USD/JPY struggled to break above Y135.00 for the better part of the Tokyo session, some suggested that topside was limited by the shrinking U.S. 2-/10-Year yield gap. The pair topped out at Y135.19, its highest level since 1998. Implied volatilities climbed across the curve, while 1-month 25 delta risk reversal snapped a two-day losing streak.

- Sales of U.S. Tsys resumed in cash Tokyo trade after CPI report published on Friday fanned hawkish FOMC bets. The greenback turned bid at the start to the new week, easily outperforming its major peers.

- The FOMC will deliver its monetary policy decision on Wednesday, just two days ahead of the BoJ's announcement. Japanese policymakers are increasingly isolated in their ultra-loose policy stance, which they are expected to reaffirm on Friday.

- Over the weekend, head of the LDP's Policy Research Council Sanae Takaichi said now was not the right time for an FX intervention, as yen weakness can help attract foreign tourists and increase export competitiveness. Her comments exposed cracks in the government's united front on yen weakness, cushioning the impact of official rhetoric signalling a sense of concern with rapid yen depreciation.

- AUD/JPY recouped initial losses amid fresh demand seen on the back of USD/JPY breaching Y135.00. The rate struggled for any further gains, with the Aussie dollar and its commodity-tied peers pressured by risk-off reaction to COVID-19 headlines out of China. Australian markets were shut for a holiday.

- Shanghai and Beijing reported upticks in COVID-19 case tallies and walked back on some of their recent re-opening measures. Offshore yuan went offered even as the PBOC set the mid-point of permitted USD/CNY trading band below the expected level for the third day in a row.

- UK economic activity indicators are about the only notable data release today. Comments are due from ECB's de Guindos, Holzmann & Simkus as well as Fed's Brainard.

FOREX OPTIONS: Expiries for Jun13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0575(E651mln), $1.0625-35(E567mln), $1.0675(E630mln), $1.0745-50(E1.9bln)

- EUR/JPY: Y143.00(E1.6bln)

- USD/CNY: Cny6.85(2.2bln)

ASIA FX: CPI Aftereffects

The release of expectation-beating U.S. CPI data after hours on Friday reverberated in Asia, as regional markets reopened, seeing U.S. Tsy yields creep higher still. Risk aversion fuelled by China's difficult COVID-19 situation exacerbated weakness in Asia EM FX space.

- CNH: Offshore yuan went offered before stabilising later in the session. The redback ignored a firmer than expected PBOC fix (25-pip deviation from sell-side estimate) as participants parsed COVID-19 headlines highlighting upticks in Shanghai & Beijing case tallies that resulted in partial re-tightening of virus curbs. Spot USD/CNH sits ~260 pips higher after printing a three-week high.

- KRW: The won was comfortably the worst performer in the Asia EM basket, as fallout from the U.S. & China was amplified by domestic concerns. Early trade data showed that South Korea recorded a trade deficit of $6bn in the first 10 days of June, as a couple of public holidays weighed on exports. Meanwhile, North Korea fired artillery shots, presumably from multiple rocket launchers, amid fears of a potential imminent nuclear test.

- IDR: Spot USD/IDR crept higher, with the rupiah suffering from higher U.S. Tsy yields. Bank Indonesia's weekly survey showed that inflation may break out of the central bank's target range this month.

- MYR: Spot USD/MYR took out May 19 high of MYR4.4085 and lodged fresh cycle highs at levels last seen more than two years ago.

- PHP: Firm resistance from PHP53.000 gave way as spot USD/PHP soared in line with regional trend, ignoring outgoing BSP Gov Diokno's remark that the central bank will scale back its daily purchases of government securities as policy normalises. Separately, incoming Economic Planning Secretary Balisacan suggested that higher inflation may cause 2022 GDP growth to average below the target set by the outgoing administration.

- THB: Hawkish comments from BoT Gov Sethaput helped the baht recover from lows, after spot USD/THB showed at its best levels in four years. The official tipped hat to the need to withdraw monetary stimulus as inflation rises, testing the central bank's policy mandate. In a break with previously cautious language, he added that "too slow a rate hike is not good," opening the door for the BoT to join the global tightening campaign.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/06/2022 | 0600/0700 | ** |  | UK | Index of Services |

| 13/06/2022 | 0600/0700 | ** | | UK | UK Monthly GDP |

| 13/06/2022 | 0600/0700 | *** | | UK | Index of Production |

| 13/06/2022 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 13/06/2022 | 0600/0700 | ** | | UK | Trade Balance |

| 13/06/2022 | 0600/0800 | ** |  | NO | Norway GDP |

| 13/06/2022 | 1100/1300 |  | EU | ECB de Guindos at Arab Central Banks & Monetary Authorities' Meeting | |

| 13/06/2022 | 1230/0830 | * |  | CA | Household debt-to-disposable income |

| 13/06/2022 | 1500/1100 | ** |  | US | NY Fed survey of consumer expectations |

| 13/06/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 13/06/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.