Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- SUNAK AND TRUSS RULE OUT FREEZING ENERGY PRICES AT LEADERSHIP HUSTINGS (GUARDIAN)

- RBNZ DELIVERS EXPECTED 50BP RATE HIKE

- BOC'S MACKLEM: CANADA INFLATION MAY HAVE PEAKED BUT STILL TOO HIGH (RTRS)

- RUSSIAN ECONOMY MINISTRY SEES SMALLER 2022 SLUMP, LOWERS 2023 GDP VIEW (RTRS)

- US WEIGHS EU PLAN TO REVIVE IRAN NUCLEAR DEAL ABANDONED BY TRUMP (BBG)

- EU SAYS IRAN’S RESPONSE TO NUCLEAR DEAL PLAN IS CONSTRUCTIVE (BBG)

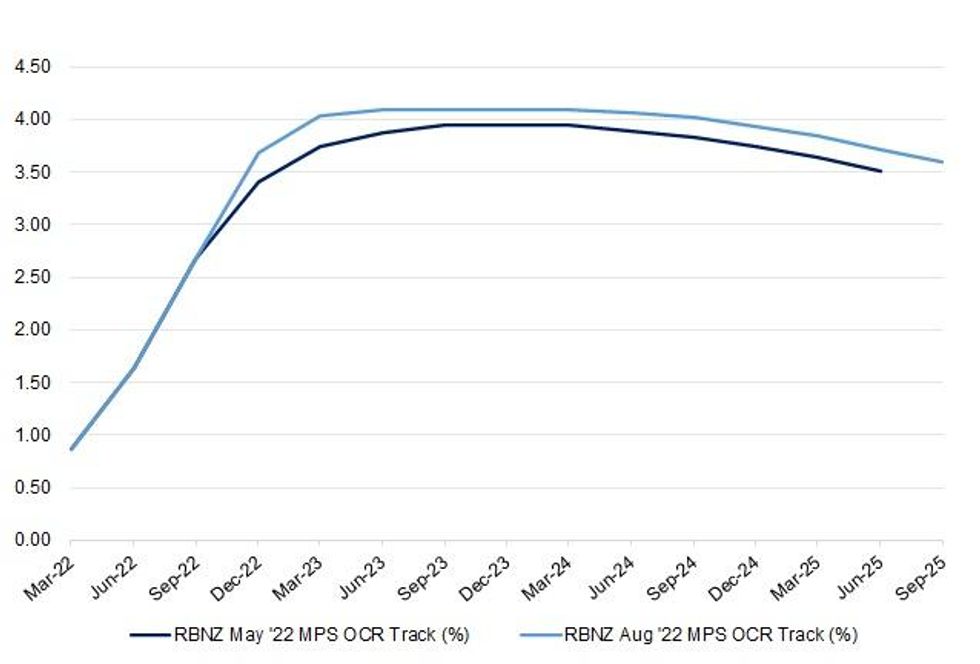

Fig. 1: RBNZ Aug ‘22 OCR Track Vs. May ‘22 OCR Track

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UK

POLITICS/FISCAL: Rishi Sunak and Liz Truss have ruled out freezing energy prices by claiming it would be an expensive, short-term fix that would fail to solve the underlying problem with soaring energy costs. (Guardian)

POLITICS/FISCAL: Rishi Sunak escalated his attacks on Liz Truss by warning tonight that her plans to tackle the cost of living crisis would lead to millions of people being “tipped into destitution”. (The Times)

ECONOMY: British employers agreed average pay rises of 4% with staff in the three months to the end of July, the joint-biggest increase since 1992 but falling further behind inflation, industry data showed on Wednesday. (RTRS)

EUROPE

GERMANY: Germany’s natural gas reserves may be filling faster than normal, but the country will still struggle to have enough fuel to get through the coming winter. Even if gas inventories can meet Germany’s target of being 95% full by November, that would only cover about 2-1/2 months of heating, industrial and power demand if Russia cuts off supplies completely, according to Klaus Mueller, president of the Federal Network Agency, the country’s energy regulator. Stockpiles are currently 77% full, which is two weeks ahead of schedule. (BBG)

GERMANY: Germany’s government denied a media report on Tuesday that it had decided to postpone the closure of its last three nuclear power plants, saying it would make its final decision once it received the results of ongoing stress tests. (RTRS)

U.S.

FED: The Federal Reserve will likely raise interest rates substantially more than markets are pricing in because inflation will prove stubborn even amid slowing economic activity, former long-time Bank of England member and adviser Charles Goodhart told MNI. (MNI)

ECONOMY: The US economy faces “a lot of uncertainty” over the next year from global threats, but should be buoyed by a strong labor market and new legislation, White House economic adviser Brian Deese said Tuesday. (BBG)

ECONOMY: U.S. President Joe Biden's emergency board tasked with helping major freight railroads and unions end a contract negotiation stalemate proposed on Tuesday annual wage increases of between 4% and 7% through 2024, according to a report seen by Reuters. (RTRS)

FISCAL: President Joe Biden on Tuesday signed into law a $430 billion bill that is seen as the biggest climate package in U.S. history, designed to cut domestic greenhouse gas emissions as well as lower prescription drug prices and high inflation. (RTRS)

OTHER

GLOBAL TRADE: The U.S. Agency for International Development is spending more than $68 million to purchase and ship Ukrainian grain in the largest such export deal since Russia’s invasion this year and the start of a July agreement to allow for renewed shipments from Ukraine’s Black Sea ports. (WSJ)

GLOBAL TRADE: Toyota Motor Corp. and Contemporary Amperex Technology Co., the world’s biggest battery maker, have announced factory closures as the impact of a drought-induced power crisis in China’s Sichuan province spreads. (BBG)

U.S./CHINA/TAIWAN: US congressional visits to Taiwan are inflaming regional tensions, and the Biden administration shouldn’t underestimate China’s resolve on the issue, Beijing’s envoy to Washington said Tuesday. (BBG)

RBNZ: New Zealand raised interest rates by a half percentage point for a fourth straight meeting, underscoring the Reserve Bank’s status as a leading hawk in the global tightening cycle. The Monetary Policy Committee lifted the Official Cash Rate to 3% -- a seven-year high that was unanimously forecast by economists -- on Wednesday. It reckons the OCR will reach 3.69% at the end of this year and peak at 4.1% in the second quarter of 2023, higher and sooner than previously forecast. (BBG)

NORTH KOREA: South Korea doesn’t back the use of force to bring down the North Korean regime, President Yoon Suk Yeol said, adding he is open to speak with leader Kim Jong Un if he’s willing to end his atomic ambitions. (BBG)

HONG KONG: “We will definitely continue to relax curbs when conditions are mature and permit as it is beneficial to the economy and various industries,” Hong Kong’s Chief Secretary Eric Chan says at a briefing when asked about international travel restrictions. (BBG)

BOC: Canadian inflation may have peaked, but it remains far too high, Bank of Canada Governor Tiff Macklem said in a newspaper op-ed on Tuesday, after official data showed annual price increases eased to 7.6% in July from 8.1% in June. (RTRS)

RUSSIA: Russia's economy will contract less than expected and inflation will not be as high as projected three months ago, the economy ministry forecasts seen by Reuters showed, suggesting the economy is dealing with sanctions better than initially feared. The economy is plunging into recession after Moscow sent its armed forces into Ukraine on Feb. 24, triggering sweeping Western curbs on its energy and financial sectors, including a freeze of Russian reserves held abroad, and prompting scores of Western companies to leave. (RTRS)

RUSSIA: Russia notified Japanese companies that buy liquified natural gas from Sakhalin-2 of plans to transfer rights to the project to a new Russian entity, Nikkei reports. (BBG)

SOUTH AFRICA: South African opposition parties that formed coalitions to wrest control of a number of towns from the governing African National Congress in last year’s municipal elections, are now considering campaigning jointly ahead of a national and provincial vote in 2024. (BBG)

IRAN: The Biden administration is weighing Iran’s response to a European Union proposal aimed at reviving the 2015 international nuclear agreement, with officials on both sides of the Atlantic signaling the possibility that a deal could emerge now after more than a year of false starts. (BBG)

IRAN: The European Union views Iran’s response to a proposed blueprint for reviving the 2015 nuclear deal as constructive, according to an official familiar with the diplomatic efforts, and is consulting with the US on a “way ahead” for the protracted talks. (BBG)

OIL: Shell on Tuesday said it plans to shut for two weeks in September a key crude oil pipeline in Gulf of Mexico that supplies oil to Louisiana refineries. The Odyssey and Delta crude pipelines in September will be shut for planned maintenance early-to-mid September, Shell said in a statement. (RTRS)

FOREX: The amount of foreign-exchange transactions has leaped over the past year amid a surge in market volatility that’s been fueled by increased geopolitical turbulence and big shifts in monetary policy as central banks around the world battle to contain inflation. (BBG)

CHINA

BONDS: Chinese government bond yields may decline further as the country's central bank will still maintain reasonably ample liquidity to offset downward pressure on the economy, while money market interest rates will remain low in the short term, the 21st Century Business Herald wrote, citing analysts. Following the PBOC's surprise cuts to two major policy rates on Monday, the 10-year Treasury yield extended its fall to around 2.60%, which represented a fresh two-year low. The rate cuts ignited bullish sentiment in the bond market, as traders bet on a longer easing cycle given the current economic downturn and limited financing needs, the newspaper noted. (MNI)

PROPERTY: More Chinese cities are expected to lower down payment ratio demands for house purchases after some cities cut deposit requirements for first-time buyers to as low as 20%, in a bid to prop up the struggling real estate market, the Securities Daily reported, citing analysts. Further relaxation, including optimizing purchase and loan restrictions, in addition to lower mortgage rates, should be deployed to stimulate housing demand, the newspaper wrote, citing analysts. As of early August, nearly 240 cities had issued more than 650 measures to relax housing regulations, ranging from issuing home purchase subsidies and easing purchase restrictions in a bid to attract talented workers, the newspaper noted. (MNI)

CHINA MARKETS

PBOC INJECTS CNY2 BILLION VIA OMOS, LIQUIDITY UNCHANGED

The People's Bank of China (PBOC) injected CNY2 billion via 7-day reverse repos with the rate unchanged at 2.0% on Wednesday. This keeps the liquidity unchanged after offsetting the maturity of CNY2 billion repos today, according to Wind Information.

- The operation aims to keep liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.6751% at 9:38 am local time from the close of 1.3192% on Tuesday.

- The CFETS-NEX money-market sentiment index closed at 53 on Tuesday vs 45 on Monday.

PBOC SETS YUAN CENTRAL PARITY AT 6.7863 WEDS VS 6.7730

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 6.7863 on Wednesday, compared with 6.7730 set on Tuesday.

OVERNIGHT DATA

JAPAN JUL TRADE BALANCE -Y1,436.8BN; MEDIAN -Y1,362.5BN; JUN -Y1,398.5BN

JAPAN JUL EXPORTS +19.0% Y/Y; MEDIAN +17.6%; JUN +19.3%

JAPAN JUL IMPORTS +47.2% Y/Y; MEDIAN +45.5%; JUN +46.1%

JAPAN JUL ADJUSTED TRADE BALANCE -Y2,133.3BN; MEDIAN -Y1,914.9BN; JUN -Y1,950.0BN

JAPAN CORE MACHINE ORDERS +0.9% M/M; MEDIAN +1.0%; MAY -5.6%

JAPAN CORE MACHINE ORDERS +6.5% Y/Y; MEDIAN +7.7%; MAY +7.4%

AUSTRALIA JUL WESTPAC LEADING INDEX -0.15% M/M; JUN -0.16%

The Index growth rate has held broadly steady over the last three months after an abrupt slowdown earlier in the year from a strongly above trend starting point. Latest reads are consistent with momentum continuing to track slightly above trend heading into year-end. While overall momentum in the economy remains above trend we expect that as we near the final quarter of the year growth in spending will slow under the weight of rising interest rates and high inflation which are already sapping confidence. However, these negative forces are, for now, being compensated by a very strong labour market and solid household balance sheets. (Westpac)

AUSTRALIA Q2 WAGE PRICE INDEX +2.6% Y/Y; MEDIAN +2.7%; Q1 +2.4%

AUSTRALIA Q2 WAGE PRICE INDEX +0.7% Q/Q; MEDIAN +0.8%; Q1 +0.7%

NEW ZEALAND Q2 INPUT PPI +3.1% Q/Q; Q1 +3.4%

NEW ZEALAND Q2 OUTPUT PPI +2.4% Q/Q; Q1 +2.6%

MARKETS

SNAPSHOT: RBNZ Delivers 50bp Hike, Shifts OCR Track Higher

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 up 303.97 points at 29173.2

- ASX 200 up 13.011 points at 7118.40

- Shanghai Comp. up 9.134 points at 3287.019

- JGB 10-Yr future down 15 ticks at 150.46, yield up 1bp at 0.184%

- Aussie 10-Yr future down 3.5 ticks at 96.72, yield up 4bp at 3.264%

- U.S. 10-Yr future -0-00+ at 119-12, yield up 1.27bp at 2.817%

- WTI crude up $0.78 at $87.31, Gold up $3.31 at $1778.99

- USD/JPY down 11 pips at Y134.11

- SUNAK AND TRUSS RULE OUT FREEZING ENERGY PRICES AT LEADERSHIP HUSTINGS (GUARDIAN)

- RBNZ DELIVERS EXPECTED 50BP RATE HIKE

- BOC'S MACKLEM: CANADA INFLATION MAY HAVE PEAKED BUT STILL TOO HIGH (RTRS)

- RUSSIAN ECONOMY MINISTRY SEES SMALLER 2022 SLUMP, LOWERS 2023 GDP VIEW (RTRS)

- US WEIGHS EU PLAN TO REVIVE IRAN NUCLEAR DEAL ABANDONED BY TRUMP (BBG)

- EU SAYS IRAN’S RESPONSE TO NUCLEAR DEAL PLAN IS CONSTRUCTIVE (BBG)

US TSYS: Tight Range In Asia As Market Awaits FOMC Minutes

TYU2 stuck to a narrow 0-05 range during Asia-Pac hours, dealing either side of late NY levels, last -0-00+ at 119-12 on sub-par volume of ~45K, with Antipodean influences (namely the previously covered Australian wage data and RBNZ monetary policy decision) having very modest impact on price action. Cash Tsys run flat to 1.5bp cheaper on the day at present, with 7s providing the weakest point of the curve.

- Looking ahead, UK CPI data will provide some interest during London hours, as will Eurozone GDP. Further out, Wednesday’s NY docket consists of the minutes from the most recent FOMC monetary policy meeting, retail sales data, weekly MBA mortgage apps. 20-Year Tsy supply and Fedspeak from Governor Bowman (although the topics of the discussion may limit the room for comments on monetary policy).

JGBS: Twisting Flatter

JGB futures stuck to a very narrow range during the Tokyo morning, dealing either side of late overnight levels before hitting the lunch bell -12. When it comes to wider cash JGB trade it would seem that the curve took direction from the twist flattening of the U.S. Tsy curve on Tuesday, which we suggested may be the case ahead of the Tokyo open, with the major benchmarks running 1bp cheaper to 2bp richer across the curve, as 20+-Year paper richens.

- There hasn’t been much in the way of meaningful domestic headline flow, with the monthly trade balance data revealing a record wide deficit in adjusted terms, while core machinery orders was marginally softer than expected, but still rose in M/M terms. These data points failed to impact the space, as is the norm.

- BoJ Rinban operations yielded the following offer/cover ratios:

- 1- to 3-Year: 1.99x (prev. 1.80x)

- 5- to 10-Year: 2.13x (prev. 2.97x)

- 25+-Year: 3.61x (prev. 3.44x)

- There shouldn’t be much impact from these cover ratios, outside of the potential for light support for the 5- to 10-Year zone.

AUSSIE BONDS: Bear Flattening

Aussie bonds operate off their extremes, with cheapening in ACGBs on the back of the RBNZ’s monetary policy decision helping to pull the space away from best levels observed after a modest miss in Q2 wage price inflation data provided support. Cash ACGBs run 2.5-4.5bp cheaper across the curve, with 5s leading the way lower. YM is -4.5, back from a brief look above its overnight high, while XM is -4.0 after failing to test its own overnight extremes. EFPs are wider, with the 3-/10-Year box flattening, while Bills run 1 tick richer to 6 ticks cheaper through the reds.

- In terms of the details, Q2 wage price data saw a slight miss in both headline readings (+2.6% Y/Y vs. BBG median +2.7%; +0.7% Q/Q vs. BBG median +0.8%). A note that the reading was in line with the projections in the RBA’s latest SoMP and is not expected to move the needle re: the RBA’s near-term rate hike trajectory.

- STIR market pricing re: tightening for the RBA’s Sep meeting initially blipped lower to ~37bp before rising to ~41bp after the RBNZ’s monetary policy decision, sitting little changed from levels observed ahead of today’s risk events.

- The latest round of ACGB May-32 supply saw mediocre demand, with the cover ratio declining to 2.65x from the 3.00x observed at the previous auction, below the six-auction average of 2.83x. Things were firmer on the pricing side, with the weighted average yield printing 0.72bp through prevailing mids (per Yieldbroker). The lack of relative value due to the flatness of the ACGB curve as well as the structurally rich status of the line (due to its benchmark 10-Year status) likely contributed to the softer cover ratio at the auction, with the continued sidelining of international investors on uncertainty re: RBA policy, as well as the proximity of the auction to today’s Antipodean risk events, providing additional headwinds for demand.

- Looking ahead, labour market data for July will headline Thursday's domestic data docket, with little else on offer.

AUSSIE BONDS: AOFM sells A$800mn of the 1.25% 21 May 2032 Bond, issue #TB158:

The Australian Office of Financial Management (AOFM) sells A$800mn of the 1.25% 21 May 2032 Bond, issue #TB158:

- Average Yield: 3.2691% (prev. 3.5425 %)

- High Yield: 3.2725% (prev. 3.5450%)

- Bid/Cover: 2.6500x (prev. 3.0025x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield: 2.8% (prev. 84.2%)

- Bidders 48 (prev. 41), successful 22 (prev. 15), allocated in full 16 (prev. 8)

EQUITIES: Higher In Asia; Walmart Earnings Lifts Retailers

Major Asia-Pac equity indices are higher at typing, bucking a mixed lead from Wall St. Retail-related equities across the region were bid after Walmart’s better-than-feared earnings beat on Tuesday, while Chinese developers are on track to close higher for a second day.

- To elaborate, sentiment in China-based developers continues to improve amidst recent reports of increased house purchasing inquiries in cities with lower mortgage down payment ratios, with the Hang Seng Mainland Properties Index (+1.0%) on track to notch a second day of gains, extending a rise off of recently made record lows.

- The Hang Seng is 0.8% firmer at writing, seeing the finance (+0.6%) and property (+0.4%) sub-indices lead the way higher. China-based tech rose modestly (HSTECH: +1.0%) alongside a strong rally in Meituan (+4.7%), although the performance in the latter comes after a 9.1% decline on Tuesday.

- The CSI300 is 0.7% better off after reversing earlier losses, on track for its highest daily close in over two weeks. Real estate names outperformed (CI300 Real Estate Index: +2.9%), augmenting relatively shallow gains observed across much of the CSI300.

- The ASX200 is off its extremes, trading 0.3% higher at writing. Losses in healthcare and tech were countered by gains in the consumer staples sub-gauge (+1.6%), with retailers such as Woolworths (+1.4%) outperforming.

- E-minis operate on either side of neutral levels at typing after a fairly limited Asia-Pac session so far, sitting just off fresh multi-month highs made on Tuesday.

OIL: A Little Above Multi-Month Lows; Iranian Matters At The Fore

WTI is ~+$0.60 and Brent is ~+$0.50 at typing, edging away from their respective multi-month lows made on Tuesday.

- To recap, both benchmarks shed ~$3 apiece on Tuesday for a third consecutive lower daily close, with WTI hitting levels last witnessed in end-Jan during the session. The weakness in crude was facilitated by perceived progress in a U.S.-Iran nuclear deal, adding to pressure from wider worry re: global economic growth.

- To elaborate on the former, BBG sources have pointed to the EU describing Iran’s response to its “final draft” as “constructive”, with the Biden administration due to respond as well. The U.S. State Dept has however maintained that the Islamic Revolutionary Guard Corps will remain a designated terrorist organisation - a sticking point in past negotiations. A note that Goldman Sachs has since weighed in on the agreement as “unlikely” in the short-term (details fleshed out in earlier bullets).

- The prompt spreads for WTI and Brent have continued their descent, printing ~$0.40 and ~$0.61 respectively at typing, a little above fresh multi-month lows observed on Tuesday.

- WTI rose off worst levels on Tuesday after the latest round of API inventory estimates, with reports pointing to a significant drawdown in gasoline stocks, easing worry from some quarters re: demand destruction, while a decline in crude, distillate, and Cushing hub stockpiles was reported as well. Up next, U.S. EIA data is due later today, with BBG median estimates looking for drawdowns in crude and gasoline stockpiles.

GOLD: Treading Water Above $1,770; FOMC Minutes Eyed

Gold is little changed, printing ~$1,776/oz at writing. The precious metal operates a little above one-week lows, with recent Dollar strength providing evident headwinds for the space.

- To recap, the precious metal closed ~$4/oz lower on Tuesday, worsening Monday’s steep ~$23/oz decline amidst an uptick in U.S. real yields, with the USD (DXY) closing little changed on the day, holding on to the bulk of its gains from a two-day rally prior.

- Measures of investor interest have continued to weaken as well, with total known ETF holdings of gold on track to fall for a ninth consecutive week, hitting levels last witnessed in end-Feb at typing.

- Looking ahead, focus will centre on the minutes for the Fed’s July FOMC, with U.S. MBA mortgage applications, retail sales data, and Fedspeak from the Fed’s Bowman expected to provide additional points of interest prior (noting that Bowman’s scheduled speaking topics may limit the scope for commentary on monetary policy).

- From a technical perspective, Tuesday’s moves lower in gold has seen it break initial support at ~$1,772.0/oz (20-Day EMA), exposing further support at $1,754.4/oz (Aug 3 low, key short-term support). On the other hand, initial resistance is seen at $1,807.9/oz (Aug 10 high and bull trigger).

FOREX: Antipodeans Dominate

AUD and NZD FX flows have dominated today, following key event risks in both economies.

- AUD/USD dipped sub 0.6990, following the weaker than expected Q2 wages print, which came in at 0.7% versus 0.8% expected. Annual growth was also weaker than expected at 2.6%YoY, but in line with the recent RBA forecast projection. AU rates dipped on the data print, but there wasn't a great deal of follow through. The 2yr bond yield is back to levels that prevailed prior to the data release (2.77%).

- Helping these moves was a hawkish 50bps RBNZ hike, the central raised their OCR peak to above 4%, while also noting a larger increase was considered at the meeting. NZD/USD spiked higher, gaining above 0.6380 before selling interest emerged. We dipped back below 0.6340 during RBNZ Governor Orr's press conference as he stated the central bank didn't get close to a 75bps hike announcement today. NZD/USD is now back at 0.6350.

- AUD/NZD initially dipped sub 1.1000, touching a low of 1.0990 before support kicked in. We are back around 1.1030/35 now. Note the 100 day MA comes in at 1.1014 for the cross.

- Tight ranges have prevailed elsewhere, with EUR/USD not getting much beyond a 1.0165/1.0180 range. USD/JPY has had a wider range, with a brief dip below 134.00 supported. We are now back at 134.15. US equity futures have been quiet, not too far away from flat for most of the session, while US yields have been relatively steady as well.

- Coming up, focus will turn to UK inflation data, flash EZ GDP and U.S. retail sales. Comments are also due from the Fed's Bowman. Elsewhere, the FOMC will release the minutes from its most recent monetary policy meeting.

FX OPTIONS: Expiries for Aug17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1000-15($1.2bln), $1.0190-00($727mln), $1.0300(E697mln)

- USD/CAD: C$1.2855($515mln), C$1.3065($864mln)

- USD/CNY: Cny6.7600-14($685mln)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/08/2022 | 0600/0700 | *** |  | UK | Producer Prices |

| 17/08/2022 | 0600/0700 | *** | | UK | Consumer inflation report |

| 17/08/2022 | 0600/0800 | ** |  | NO | Norway GDP |

| 17/08/2022 | 0830/0930 | * | | UK | ONS House Price Index |

| 17/08/2022 | 0900/1100 | * |  | EU | Employment |

| 17/08/2022 | 0900/1100 | *** | | EU | GDP (p) |

| 17/08/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 17/08/2022 | 1230/0830 | *** | | US | Retail Sales |

| 17/08/2022 | 1330/0930 | | US | Fed Governor Michelle Bowman | |

| 17/08/2022 | 1400/1000 | * | | US | Business Inventories |

| 17/08/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 17/08/2022 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 17/08/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 17/08/2022 | 1820/1420 | | US | Fed Governor Michelle Bowman |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.