Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED’S COLLINS SAYS FURTHER TIGHTENING COULD BE WARRANTED - MNI

- BIDEN WEIGHS REVERSAL ON $6BN FOR IRAN AFTER HAMAS ATTACK - BBG

- UK COMPANIES STRUGGLING WITH LABOUR SHORTAGES - CBI - MNI BRIEF

- MORE FLEXIBILITY ON RISING INFLATION - BOJ NOGUCHI - MNI BRIEF

- JAPAN SEP PPI RISE SLOWS ON 2.0% VS. AUG 3.3% - MNI BRIEF

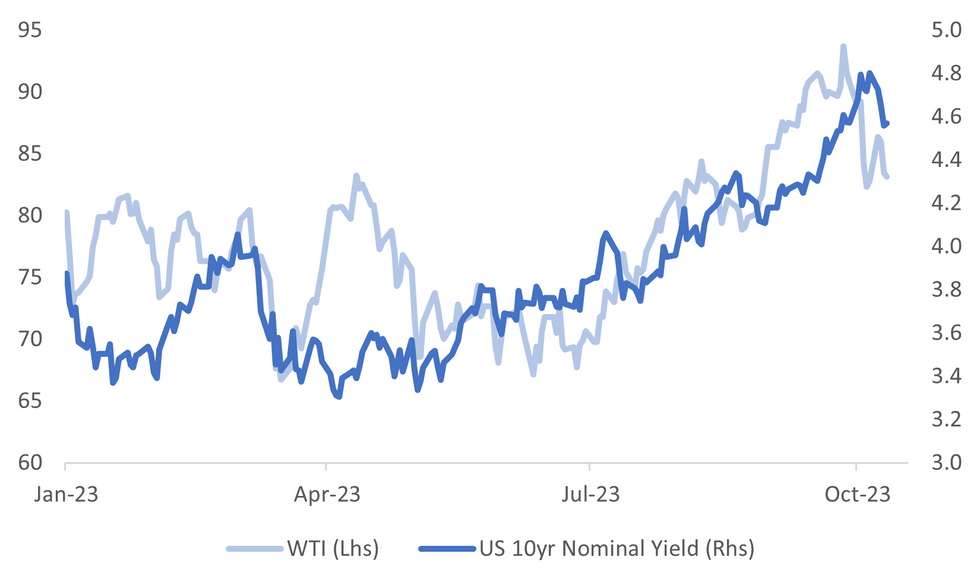

Fig. 1: WTI & Nominal US 10yr Government Bond Yield

Source: MNI - Market News/Bloomberg

U.K.

LABOUR: Labour shortages continued to be a strain on UK businesses in the last 12 months, a Confederation of British Industry survey shows, with more than 70% of respondents reporting problems hiring staff. (MNI BRIEF)

HOUSING: “The UK housing market showed signs of stabilizing in September as borrowing costs continued to ease amid hopes the Bank of England may be finished raising interest rates, a survey found.” (BBG)

EUROPE

EU/CHINA: “The European Union’s top diplomat has waited all year for the right moment to visit China. Now, he’s finally arriving with the differences between Brussels and Beijing looking larger than ever.” (BBG)

ECB: “The European Central Bank should consider only paying interest on 90% of the money banks keep in their deposit accounts, Governing Council member Robert Holzmann said. “ (BBG)

ECB: “European Central Bank Governing Council member Boris Vujcic said it’s too soon to declare victory over inflation as key developments in the euro-zone economy will only play out over time.” (BBG)

U.S.

FED: Federal Reserve Bank of Boston President Susan Collins Wednesday left open the potential for more policy tightening to bring inflation sustainably back toward the 2% target and affirmed high-for-long interest rates are likely. (MNI)

US/IRAN: “Biden administration officials are leaving open the possibility of re-freezing $6 billion in Iranian oil money that was released as part of a prisoner swap amid growing bipartisan criticism after Iran-backed Hamas militants attacked Israel.” (BBG)

US/IRAN: “U.S. President Joe Biden warned Iran against getting involved in Israel's conflict with Hamas amid fears of a wider regional conflict, while ongoing Israeli air strikes around the Gaza Strip drove hundreds of thousands from their homes.” (RTRS)

POLITICS: “Republicans who control the U.S. House of Representatives on Wednesday nominated Steve Scalise to serve as speaker following last week's ouster of Kevin McCarthy, but delayed further action when he appeared to be short of the support needed to win a vote of the full chamber.” (RTRS)

OTHER

OIL: The American Petroleum Institute reports US commercial inventories of crude oil rose by a massive 12.9 million barrels last week, a source citing the data says, while gasoline supplies increased by 3.6 million barrels. The bearish results were released ahead of official EIA inventory data due tomorrow morning. (Dow Jones)

ISRAEL: “Prime Minister Benjamin Netanyahu, hours after forming an emergency government and wartime cabinet, foreshadowed a major ground attack on Gaza by promising to destroy Hamas.” (BBG)

JAPAN: Bank of Japan board member Asahi Noguchi said on Thursday that the BOJ will need to increase the flexibility of easy policy to continue yield curve control when the expected inflation rate begins rising. (MNI BRIEF)

JAPAN: The y/y rise in Japan's corporate goods price index slowed to 2.0% in September from August's revised 3.3% for the ninth straight deceleration, indicating that pass-through of cost increases continued but at a slower pace, data released by the Bank of Japan showed Thursday. (MNI)

AUSTRALIA: “Australia’s banking regulator said the pockets of stress that have appeared in the nation’s housing market since interest rates started ramping up aren’t becoming more widespread.” (BBG)

CHINA

STOCK MARKET: “China’s sovereign fund, Central Huijin Investment, has doubled down on its investments in the country’s “Big Four” state-owned banks for the first time since 2015. Bank of China, Agricultural Bank of China, China Construction Bank, and Industrial and Commercial Bank of China confirmed the news.”(Xinhua Finance)

ECONOMY: “China’s Q3 GDP growth may reach over 4% as the economy shows more signs of recovery. Retail sales are expected to rebound to about 5.5% in September, supported by the lower comparison base for the same period last year alongside a boost to domestic tourism driven by the Hangzhou Asian Games and the recent Golden Week holiday, said Wen Bin, chief economist at China Minsheng Bank. “ (Securities Daily)

ECONOMY: “Xinhua News Agency reported that Chinese Vice President Han Zheng met in Beijing on Wednesday with Wallenberg, chairman of the board of directors of Swedish Bank Ruida Group, and said that the economy has generally rebounded for the better this year and the expected growth target for the whole year is expected to be achieved.” (XINHUA/BBG)

GEOPOLITICS: “China’s special envoy on Middle East issues is expected to speak Thursday with Israeli officials, according to Israel’s Ambassador to China.” (BBG)

CHINA MARKETS

MNI: PBOC Drains Net 346 Bln Via OMO Thurs; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY162 billion via 7-day reverse repo on Thursday, with the rate unchanged at 1.80%. The operation has led to a net drain of CNY346 billion after offsetting the maturity of CNY508 billion reverse repos today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8324% at 09:36 am local time from the close of 1.9247% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 41 on Wednesday, the same as the close on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

PBOC Yuan Parity Lower At 7.1776 Thursday Vs 7.1779 Wednesday.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1776 on Thursday, compared with 7.1779 set on Wednesday. The fixing was estimated at 7.2946 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND SEP REINZ HOUSE SALES Y/Y 5.1%; PRIOR 9.2%

NEW ZEALAND SEP FOOD PRICES M/M -0.4%; PRIOR 0.5%

JAPAN SEP PPI Y/Y 2.0%; MEDIAN 2.4%; PRIOR 3.3%

JAPAN SEP PPI M/M -0.3%; MEDIAN 0.1%; PRIOR 0.3%

JAPAN AUG CORE MACHINE ORDERS Y/Y -7.7%; MEDIAN -6.7%; PRIOR -13.0%

JAPAN AUG CORE MACHINE ORDERS M/M –0.5%; MEDIAN 0.6%; PRIOR -1.1%

JAPAN SEP BANK LENDING INCL TRUSTS Y/Y 2.9%; PRIOR 3.1%

JAPAN SEP TOKYO AVG OFFICE VACANCIES 6.15%; PRIOR 6.40%

AUSTRALIA OCT CONSUMER INFLATION EXPECTATION 4.8%; PRIOR 4.6%

SOUTH KOREA BANK LENDING TO HOUSEHOLD TOTAL KR1079.8t; PRIOR KR1074.9T

MARKETS

Marginally Cheaper In Asia, CPI On Tap

TYZ3 deals at 108-02, +0-04, a 0-05 range has been observed on volume of ~65k.

- Cash tsys sit ~1bp cheaper across the major benchmarks.

- Tsys ticked away from early session highs, there was no obvious headline driver for the move lower; perhaps local participants used the recent richening to close long positions ahead of today's CPI print.

- The move lower didn't follow through with the proximity to todays CPI print limiting activity and tsys held cheaper in narrow ranges for the remainder of the session.

- FOMC dated OIS remain stable pricing a terminal rate of 5.40% in December with ~60bps of cuts by September 2024.

- The highlight of today's session is the aforementioned CPI print, we also have Fedspeak from Logan, Bostic and Collins as well as the latest 30-Year Supply.

JGBS: Futures Richer, Twist-Flattening Of the Curve, Awaiting US CPI Data

JGB futures are richer at 145.51, +27 compared to the settlement levels, slightly below the high of 145.58 set in the Tokyo morning session.

- In addition to the previously outlined domestic data drop, which included PPI data, local participants have had to digest a speech from BOJ Board Member Noguchi. Noguchi stated that “the biggest focus is whether wage hike momentum will be maintained or not.” He added that “Japan needs to shake off the 'zero norm' of prices and wages in order for a nominal wage increase to exceed 2% as a trend” and “3% nominal wage growth would correspond with a 2% inflation target”.

- Local participants have also likely been on US tsys watch ahead of US CPI data later today. Cash US tsys sit ~1bp cheaper across the major benchmarks.

- The cash JGB curve has bull-flattened beyond the 1-year (+1.0bp), with yields 0.5bp to 5.1bps lower. The benchmark 10-year yield is 1.4bps lower at 0.755% versus the cycle high of 0.814% set late last week.

- The swaps curve has twist-flattened, pivoting at the 3s, with rates 0.1bp higher to 1.8bps lower. Swap spreads are generally wider across maturities.

- Tomorrow, the local calendar sees Weekly International Investment and M2 & M3 Money Flows.

AUSSIE BONDS: Richer, Narrow Ranges, AU-US 10Y Differential Too Negative

ACGBs (YM +3.0 & XM +7.0) sit richer after dealing in relatively narrow ranges in the Sydney session. The local calendar was light today, with the previously outlined October Consumer Inflation Expectations as the sole release.

- Hence, local participants have likely eyed US tsy dealings in the Asia-Pac session for guidance ahead of the release of US CPI later today. Cash US tsys sit ~1bp cheaper across the major benchmarks. Bloomberg consensus is expecting core CPI to print +0.3% m/m (4.1% y/y) in September versus +0.3% and 4.3% prior.

- Cash ACGBs are 3-7bps, with the AU-US 10-year yield differential 1bp higher at -21bps.

- A regression of the AU-US cash 10-year yield differential and the AU-US 1Y3M swap differential over the current tightening cycle indicates that the 10-year yield differential is currently 27bps too negative versus its fair value (i.e., -21bp versus +6bp). (See link)

- Swap rates are 2-7bps lower, with the 3s10s curve flatter and EFPs little changed.

- Bills strip pricing is mixed, -1 to +3.

- RBA-dated OIS pricing is flat to 3bps softer across meetings. Terminal rate expectations sit at 4.19%.

- Tomorrow, the local calendar is empty.

NZGBS: Richer But Closed At Session Cheaps, Awaiting US CPI Data

NZGBs closed richer but at session cheaps, with benchmark yields 3-5bps higher. Despite a flurry of domestic news, including updates on REINZ house prices, food prices, and the release of the RBNZ annual report, none of these factors significantly impacted the market.

- Local participants seemed to be more attuned to the developments in US tsy dealings during the Asia-Pac session, especially in the wake of yesterday’s twist flattening.

- US tsys have been marginally pressured in recent dealing, although there hasn’t been any headline driver. Perhaps local participants are using the recent richening to close long positions ahead of this evening’s CPI print. Cash US tsys sit ~1bp cheaper across the major benchmarks.

- It's worth noting that NZGBs exhibited a slight underperformance versus US tsys, with the NZ-US 10-year yield differential finishing 1bp wider.

- The relatively low cover ratios, in the 2.5-3.0x range, seen at today’s bond auctions possibly contributed to the weaker relative performance.

- Swap rates closed 1-6bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed flat to 2bps softer across meetings. Terminal OCR expectations closed 1bp softer at 5.69%.

- Tomorrow, the local calendar sees Business NZ Mfg PMI and Card Spending data.

- Before that, attention turns to the release of US CPI data for September later today.

FOREX: Narrow Ranges In Asia

There have been narrow ranges across the G-10 space in Asia, with little follow through on moves. US Tsy Yields are a touch firmer across the curve and Oil is lower briefly erasing all the gains seen since the Hamas attack on Israel. US Equity Futures are firmer as are regional equities.

- AUD/USD is marginally firmer and last prints at $0.6415/20. Technically the outlook remains bearish, support comes in at $0.6287 2.00 projection of the Jun 16-Jun 29-Jul 13 price swing. Resistance is at $0.6445, high from Oct 11.

- Kiwi is the weakest performer in the G-10 space. NZD/USD fell ~0.3% from peak to trough, however the move didn't follow through and the pair now sits ~0.1% below opening levels.

- Yen is little changed and is consolidating above ¥149 this morning. USD/JPY is still in an uptrend, key support is at ¥147.43 the low from Oct 3 and resistance is at ¥150.16 high from Oct 3 and bull trigger.

- Elsewhere in G-10 CHF is the strongest performer at the margins however liquidity is generally poor in Asia.

- The highlight of todays session is the September CPI print from the US. Prior to that in Europe the August GDP print from the UK is due.

EQUITIES: Broad Based Gains, China Buying Of State Banks Aids Sentiment

Regional Asia Pac equities are higher pretty much across the board. Strong gains have been evident for Hong Kong and China mainland shares, as well as Japan and South Korea. The follows positive US gains in Wednesday trade, while US futures have maintained positive momentum today. Eminis were last near 4422, back close to both the 50 and 100 day simple MAs. Nasdaq future are up by 0.29%, matching Emini gains.

- Sentiment has likely been aided by a tick down in oil benchmarks, as the risk of escalating Middle East conflict appears to have subsided for now. Still, US yields are a touch higher.

- China's mainland shares have tracked higher into the break, near +1% for the CSI 300. Reports of China's sovereign wealth fund buying local bank stocks has been a source of support (see this BBG link).

- Hong Kong shares are also tracking higher, the HSI near session highs, with gains close to 2%.

- Japan's Topix is +1.3%, while the Nikkei 225 is around 1.6% higher. The tech sensitive electrical appliances sector is leading the move. Bets the Fed is complete in terms of its tightening cycle is aiding broader sentiment in the space.

- Similarly, the Kospi is up 1%, building on yesterday's impressive gain, while the Taiex is up 0.65%.

- In SEA, Singapore's benchmark is up nearly 1%. Thailand stocks are down modestly, but this follows strong gains yesterday.

OIL: Oil Erases Post Weekend Gains Before Stabilizing

The first part of the session saw oil benchmarks drifting lower. WTI got to lows just under $82.80/bbl, which unwound all of the gains post Hamas's surprise attack on Israel over the weekend. WTI recovered some ground from there, the benchmark last near $83.10/bbl. This leaves us down a further 0.45%, following Wednesday's 2.88% loss.

- Brent was last near $85.60/bbl, down modestly from Wednesday closing levels and having followed a similar trajectory to WTI.

- Focus remains on risks of escalation in the Israel/Hamas conflict, particularly in terms of Iran. However, US intelligence agencies have reportedly stated they don't have any evidence Iran directed the Hamas attack (see this BBG link for more details). Still, the US authorities aren't ruling out fresh sanctions against Iran.

- Outside of geopolitics, coming up in the US session is official oil inventory data.

GOLD: Rallies Into 20-Day EMA

Gold is 0.2% higher in the Asia-Pac session, after closing 0.8% higher at 1874.36 on Thursday.

- Lower bond yields, dovish Fedspeak and increased geopolitical risks combined to promote a bid for the yellow metal.

- There is a growing consensus among US policymakers in favour of a more cautious stance regarding further monetary tightening. Recent dovish statements from officials such as Atlanta Fed President Raphael Bostic, Vice Chair Philip Jefferson, and Dallas Fed President Lorie Logan have prompted STIR to reduce their expectations for additional rate hikes this year.

- The focus now turns to US CPI data, which is released later today.

- Bulls will now look to breach the 20-day EMA ($1,878.2/oz), in a bid to turn the technical tide more in their favour, according to MNI’s technicals team.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/10/2023 | 0600/0700 | ** |  | UK | UK Monthly GDP |

| 12/10/2023 | 0600/0700 | ** | | UK | Index of Services |

| 12/10/2023 | 0600/0700 | *** | | UK | Index of Production |

| 12/10/2023 | 0600/0700 | ** | | UK | Trade Balance |

| 12/10/2023 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 12/10/2023 | 0740/0940 |  | EU | ECB's Elderson attends EC Summit | |

| 12/10/2023 | 0900/1000 | | UK | BoE's Pill speaks in Marrakesh | |

| 12/10/2023 | 1100/1300 | | EU | ECB's Panetta participates in IMF panel | |

| 12/10/2023 | 1230/0830 | *** |  | US | Jobless Claims |

| 12/10/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 12/10/2023 | 1230/0830 | *** | | US | CPI |

| 12/10/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 12/10/2023 | 1500/1100 | ** | | US | DOE Weekly Crude Oil Stocks |

| 12/10/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 12/10/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 12/10/2023 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 12/10/2023 | 1700/1300 | | US | Atlanta Fed's Raphael Bostic | |

| 12/10/2023 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 12/10/2023 | 1800/1400 | ** | | US | Treasury Budget |

| 12/10/2023 | 2000/1600 | | US | Boston Fed's Susan Collins |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.