Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

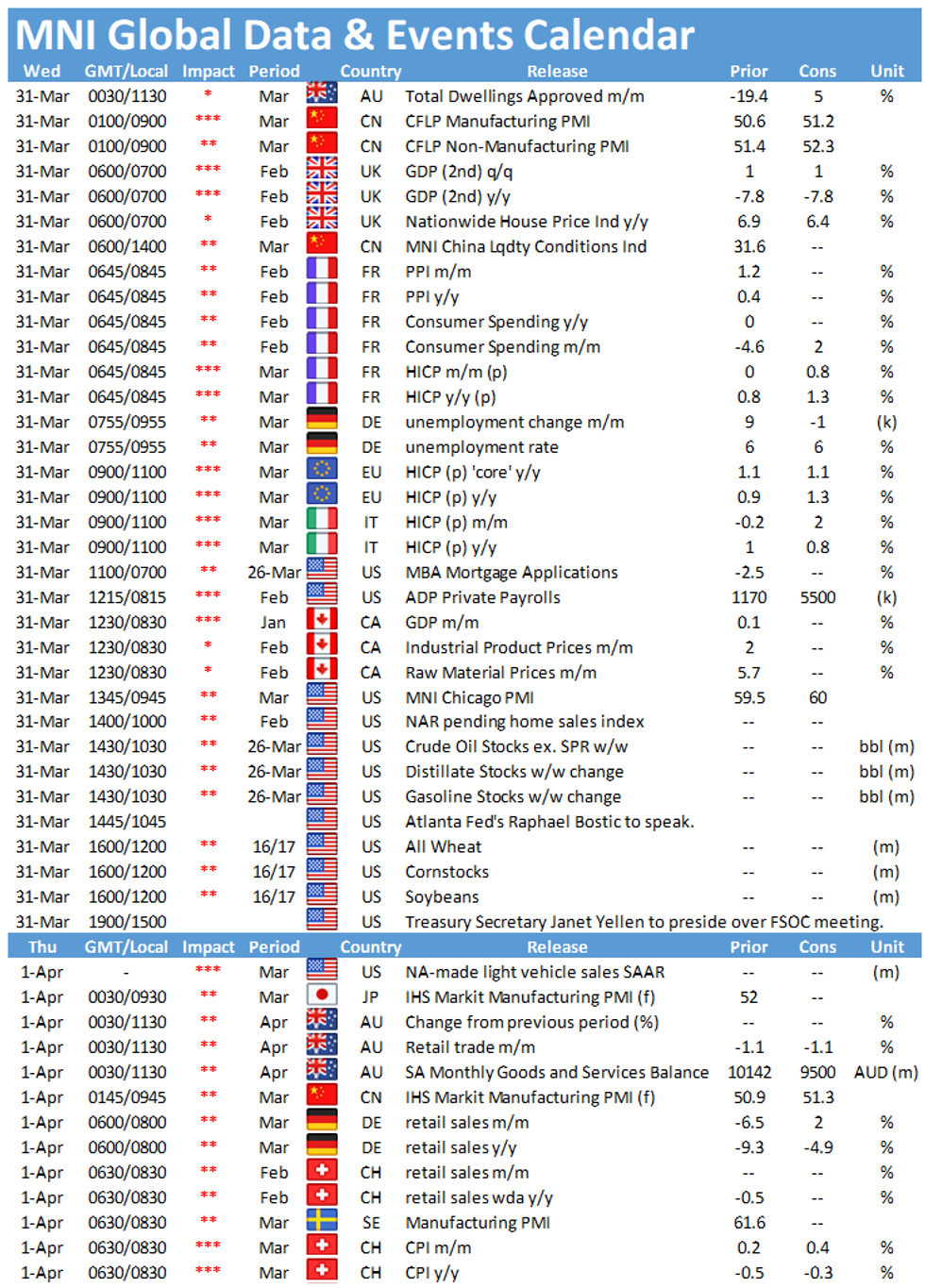

Wednesday morning kicks off with the UK's final Q4 GDP figures at 0700BST, followed by EZ flash inflation at 1000BST. In the North Americas, the release of Canadian GDP figures at 1330BST will be closely watched.

UK final GDP seen at flash

The final print of GDP is expected to register in line with the flash estimate showing an uptick of 1.0% in Q4 on a quarterly basis. Annual GDP fell by 7.8% according to the flash estimate. While private consumption remained subdued due to the lockdowns, down 0.2%, government spending recovered further to 6.4%. Business investment picked up as well in Q4 by 1.3%, however, it remains below the pre-pandemic level. Over 2020, GDP was down 9.9% which is the largest annual fall on record. Looking ahead, Q1 is likely to see a decline as the lockdown continued throughout the quarter. The BOE expects GDP to fall by 4.0% in Q1, according to the February forecast. The second quarter in 2021 is likely to see a strong rebound as the economy is gradually reopening.

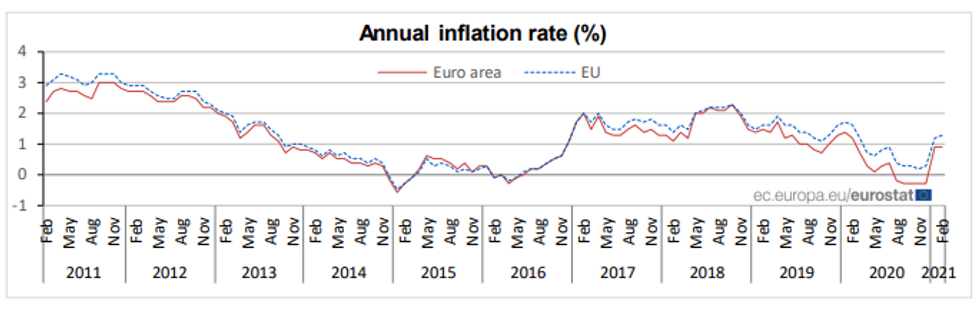

EZ inflation forecast to rise

The headline HICP rate is forecast to edge up to 1.4% in March, after recording 0.9% in both January and February. The increase is likely driven by energy inflation, considering the sharp fall in oil prices in March 2020. Core inflation is expected to remain unchanged at February's level of 1.1% in March. Already available state level data is line with market forecasts. Spanish inflation rose 0.3pp to 1.2%, while the German HICP increased 0.4pp to 2.0%. French and Italian HICP figures are also due on Wednesday. While French inflation is projected to rise to 1.5%, the Italian index is seen lower at 0.8% in March. Survey evidence such as the flash EZ composite PMI suggested higher prices for both goods and services in March, as firms face higher costs.

Source: Eurostat

Canadian economy projected to grow in January

Gross domestic product is seen rising 0.5% in January following a slowdown of 0.1% in December as second-wave lockdowns were imposed. That rebound would put the economy on track for another solid increase in Q1 following the annualized Q4 gain of almost 10%. Unexpected strength amid second-wave lockdowns has boosted expectations the BOC will taper QE at its April 21 meeting. Investors should also look for whether there is a flash estimate for February.

The events calendar throws up a quiet schedule on Wednesday. The only speeches to look out for include Atlanta Fed's Raphael Bostic and Treasury Secretary Janet Yellen.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.