Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (Washington)

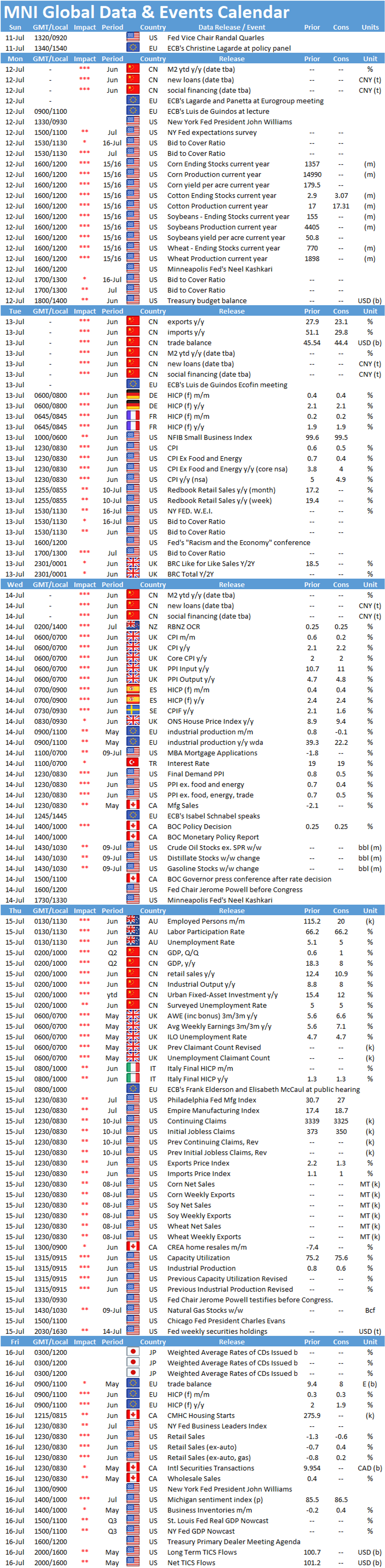

Key Things to Watch:

- Tuesday, July 13 – U.S. CPI

- Price pressures continued through June as labor shortages and ongoing supply chain disruptions hampered goods production and demand rose solidly. U.S. CPI in June should increase 0.4% in June following a stronger 0.7% increase in May, according to Bloomberg. From a year earlier, CPI should grow 4.9%, little changed from the May's 5% y/y gain.

- Excluding food and energy prices, CPI should increase 0.5% m/m and 3.8% y/y, according to Bloomberg.

- Analysts say high inflation readings are being amplified by base effects and more transitory factors should begin to fade soon, but things like higher will likely keep inflation running above 2.5% through 2022.

- Wednesday, July 14 – UK Inflation

- UK inflation is expected to have edged higher again in June, with data released Wednesday likely to show headline CPI rise 0.2% m/m and 2.2% y/y. Core inflation is expected to show a 2.0% y/y gain, in line with the May reading.

- The move will see prices move further away from the Bank of England's 2% target, but the Monetary Policy Committee has already said it will look through what it sees as transitory inflation.

- Friday, July 16 – U.S. Retail Sales

- U.S. retail sales likely dipped again in June as spending slowed further after a stimulus-fueled surge in the spring. Total sales should fall 0.6% after dropping 1.3% in May, according to Bloomberg.

- That should mostly be driven by a decline in vehicle sales, analysts say. Excluding car sales, retail sales should increase 0.4%, according to the Bloomberg consensus. Excluding both vehicle and gas station sales, retail sales are expected to increase 0.2% following May's 0.8% decline.

MNI Washington Bureau | +1 202-371-2121 | brooke.migdon@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok