Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Tech sector sold, with FAANG names all lower pre-market

- Markets cautious ahead of Powell's Semi-Annual Testimony

- Commodity strength persists, WTI futures curve now solidly north of $50/bbl

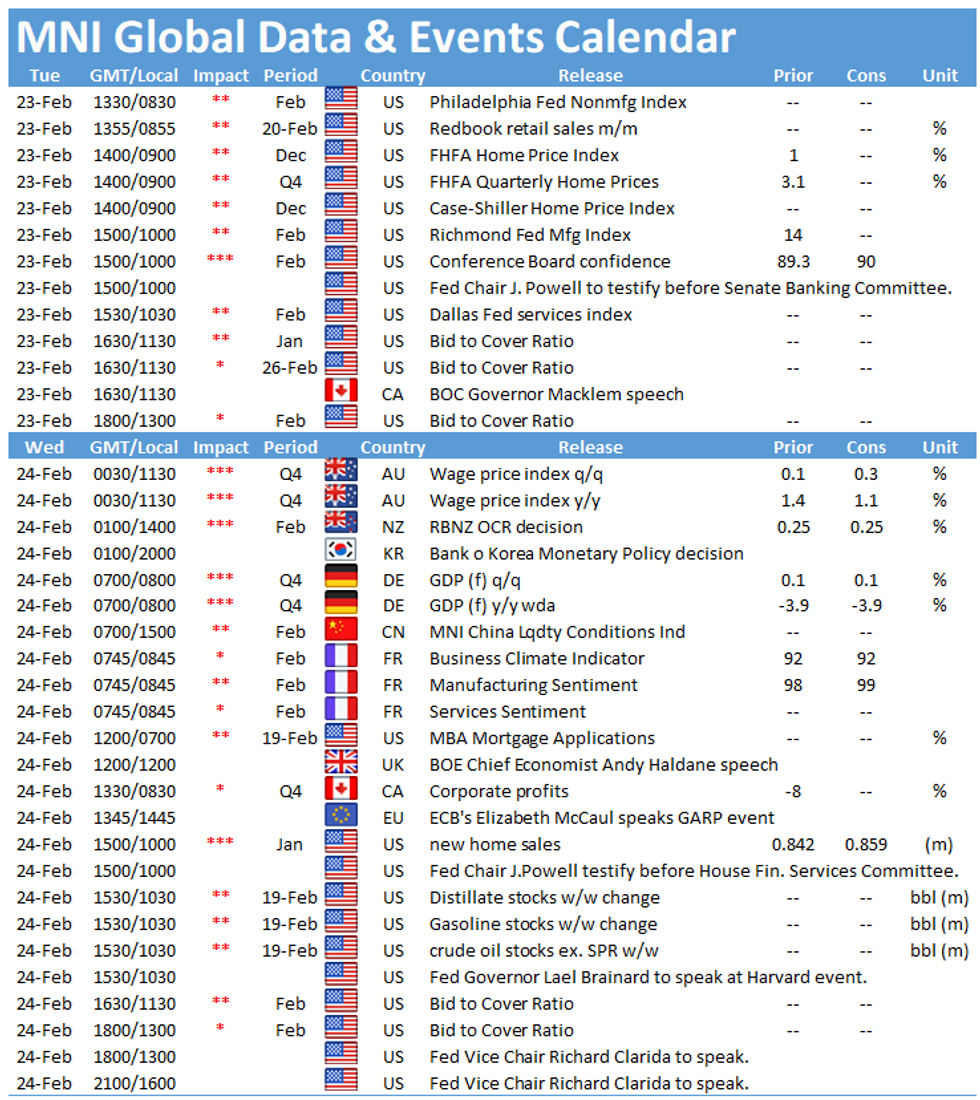

US TSYS SUMMARY: Sideways Trade Ahead Of Powell

Tsy yields have edged down from session highs with futures steady and rangebound ahead of Fed Chair Powell's Congressional appearance.

- Mar 10-Yr futures (TY) up 1/32 at 135-11.5 (L: 135-07.5 / H: 135-15.5)

- The 2-Yr yield is unch at 0.1108%, 5-Yr is down 0.5bps at 0.5938%, 10-Yr is unch at 1.3653%, and 30-Yr is up 1.1bps at 2.1838%.

- Powell appears before the Senate Banking Committee at 1000ET to deliver the Semiannual Monetary Policy Report. Prepared statement typically released for this at 0830ET.

- As we await Powell, stock weakness has stolen most of the headlines, with the Nasdaq futs off 2+% early (for good measure, Bitcoin off 17% at one point). USD bouncing from early lows too.

- In data: consumer confidence and Richmond Fed manufacturing at 1000ET.

- In supply, 1130ET sees auction of 42-day bills for $30B and 52-week bills for $34B; at 1300ET, $60B 2Y Note auction. NY Fed buys ~$2.425B of 1-7.5Y TIPS.

EGB/GILT SUMMARY: Offered

European bonds have sold off sharply this morning and curves have bear steepened while equities are broadly lower on the day.

- Gilts have traded weaker with cash yields 1-4bp higher and the curve 3bp steeper.

- UK labour market data was mixed. Wages inc bonuses increased 4.7% Y/Y in December vs 4.1% expected (ex bonus was 4.1% vs 4.0% survey), while 3m/3m employment fell 114k vs -30k survey. The UK's progress on vaccinations and the government's decision yesterday to publish its roadmap for exiting lockdown, have underpinned the shift in risk sentiment towards UK assets. Cable is now eyeing 1.41.

- Bunds have similarly sold off with the 2s30s spread 4bp wider on the day.

- OATs have slightly underperformed bunds. The curve is now 5b0 steeper.

- BTPs have been the worst performer in the region with yields at the long end of the curve up 7bp.

- The final January CPI print for the eurozone matched the initial estimate (0.9% Y/Y).

EUROPE OPTIONS FLOW SUMMARY

Eurozone:

RXJ1 170/168.5ps 1x2, sold at 8.5 in 3k

RXJ1 173/174cs 1x1.5, bought for 10 in 3k

RXJ1 173/174cs vs 170.5/170ps, bought the cs for flat in 1k

UK:

2LM1 99.62/99.37/99.12p fly sold down to 5 in 5k

EUROPEAN ISSUANCE: Italy, Netherlands, UK Auctions

Italy sells E2.5bln of Sep-22 CTZ

Average yield -0.308% (-0.277%), Bid-to-cover 1.66x (1.46x)

Netherlands DSTA sold E1.715bln of the 0.50% Jan-40 Green DSL

Average yield: 0.104% (-0.019%), Price: 107.41 (110.18)

UK DMO sells GBP2bln nominal of 0.625% Oct-50 Gilt

Avg yld 1.302% (0.837%), bid-to-cover 2.20x (2.38x), tail 0.3bps (0.3bps)

FOREX: GBP Strength Persists as Markets Endorse Path Out of Lockdown

GBP's impressive performance over the past fortnight extended further in overnight Asia-Pac trade, with GBP/USD striking a new cycle high up at $1.4098. This shifts technical targets higher, with $1.4167 the longer-term target - a key retracement of the 2016 high - 2020 low.

Focus turns to the semi-annual testimony from Fed's Powell later today, with the Fed chair appearing in front of the Senate Banking Committee at 1500GMT onwards. The Bank of Canada governor is also due to speak.

Alongside GBP strength, the USD also trades well but is still uncomfortably close to the near-term support for the USD index at 90.05. US Treasury yields are more stable relative to yesterday's open, although weakness in equities persists. The e-mini S&P is at new weekly lows, opening a gap of over 100 points with last week's all time highs.

On the data front, US consumer confidence crosses, seen showing a modest improvement from the prior reading.

OPTIONS: Expiries for Feb23 NY cut 1000ET (Source DTCC)

EUR/USD: $1.2135-55(E2.4bln-EUR puts), $1.2195-00(E1.0bln-EUR puts), $1.2300(E788mln-EUR puts)

USD/JPY: Y103.50-55($772mln), Y104.70-80($760mln), Y104.90-105.00($1.0bln), Y105.75($735mln), Y105.95-00($769mln)

EUR/GBP: Gbp0.8750(E551mln-EUR puts)

USD/CHF: Chf0.8870-80($610mln-USD puts)

AUD/USD: $0.7770-75(A$642mln), $0.7900(A$622mln)

AUD/JPY: Y83.00(A$494mln)

USD/CNY: Cny6.42($505mln)USD/MXN: Mxn20.60($500mln)

EQUITIES: Stocks Ebbing Lower, Tech Names Deflating

Equities are again lower pre-NY hours, with the e-mini S&P off close to 30 points ahead of the opening bell and opening further the gap with all time highs to over 100 points.

Tech names are underperforming pre-market, with some of the larger names suffering pre-market. The likes of Apple, Facebook and Alphabet are lower by as much as 3%, but particular weakness is noted in Tesla, which has slipped over 8% as the stock follows bitcoin lower (XBT has slipped as much as 18% today alone). Fair values are uniformly negative, with futures continuing to trade cheap relative to the underlying.

Support for the e-mini S&P undercuts at the 50-dma of 3790.46, but the 50% retracement of the February rally at 3807.88 could also provide some support.

COMMODITIES: WTI Futures Surge, Prices North of $50/bbl Across the Curve

Despite modest weakness at the tail-end of last week, WTI and Brent crude futures resumed the bull trend Monday, with futures across curve benefiting. Contracts across the curve are now north of $50/bbl for the first time since early last year, cementing the recent bullish trend and showing markets that oil strength is becoming priced in over the longer-term.

Monday's rally has bled well into Tuesday trade, with new cycle highs of $63/bbl printed for WTI. Similarly for Brent, $66.79 is the new high watermark.

For precious metals, the recovery from last week's lows continued overnight, with prices edging to $1816.03 before softening into the COMEX open. The Gold/Silver ratio continues its downtrend, re-approaching the early February and multi-year lows to start the week.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.