Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI US MARKETS ANALYSIS - BoE's Saunders Strikes A Hawkish Note

HIGHLIGHTS:

- USTs continue to gain following Fed Chair Powell's dovish tone in front of Congress yesterday

- Gilts sold off following hawkish comments from the BoE's Saunders

- UK payroll data indicate a surge in employment in June.

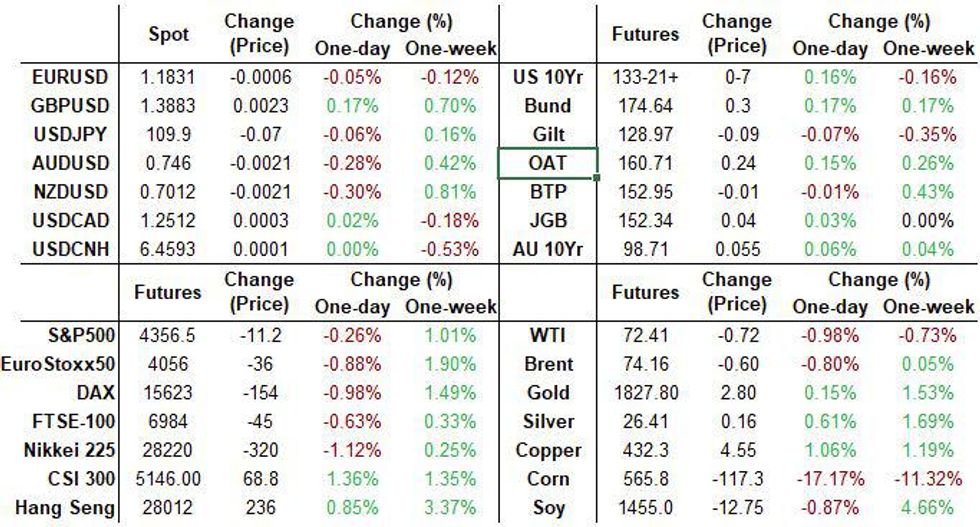

US TSYS SUMMARY: Strength Continues Ahead Of Jobless Claims Data, Powell Round 2

Treasuries continue to strengthen Thursday with the curve bull flattening, continuing yesterday's move triggered by Fed Chair Powell maintaining a dovish tone in congressional testimony.

- Tsys are off best levels overnight (10Y yields hit 1.3089%, nearing last Friday's lows) though, on hawkish commentary by the Bank of England's Saunders (0600ET) sending Gilts lower and Bunds/Tsys with them.

- The 2-Yr yield is down 0.2bps at 0.2211%, 5-Yr is down 1.6bps at 0.7784%, 10-Yr is down 1.9bps at 1.3273%, and 30-Yr is down 2.2bps at 1.9487%. Sep 10-Yr futures (TY) up 6.5/32 at 133-21 (L: 133-15.5 / H: 133-26) on strong volume (~400k).

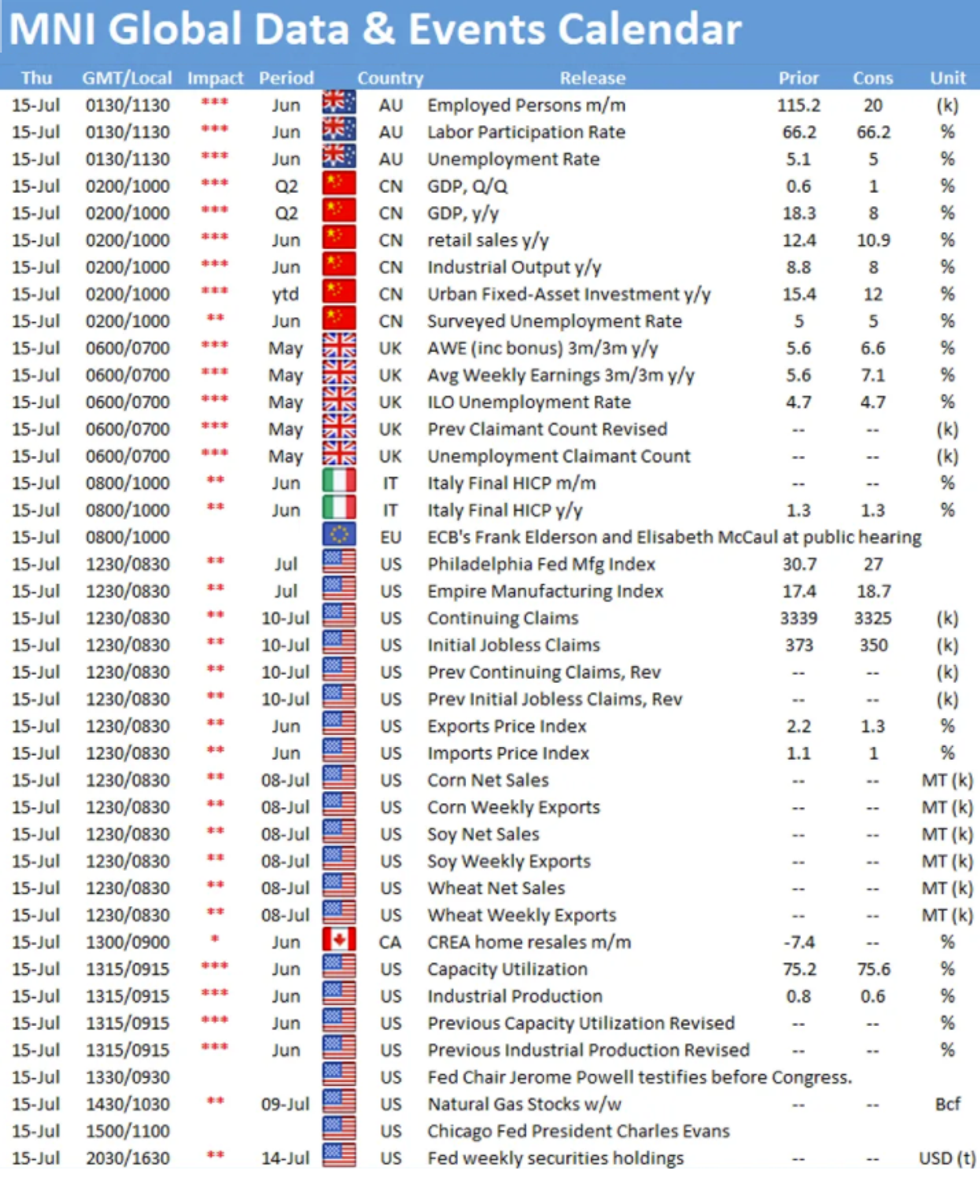

- Apart from Powell's Day 2 of testimony (before the Senate, 0930ET), we get Fed commentary from Chicago's Evans at 1100ET.

- In data: weekly jobless claims / Empire State / Philly Fed at 0830ET, with ind prod. at 0915ET.

- Supply consists of $75B of 4-/8-week bill auctions at 1130ET; NY Fed buys ~$12.425B of 0-2.25Y Tsys.

EGB/GILT SUMMARY: Saunders Comments Trigger Gilt Selling

EGBs have broadly firmed while gilts have sold off alongside a further losses for equities.

- Gilts initially edged higher early into the session before selling off sharply at 1100GMT when the BoE's Saunders suggested that it may soon be appropriate to withdraw the pandemic stimulus. Gilt yields are now 1-3bp higher with the curve bear flattening.

- The headline results from today's UK employment report were a touch weaker than expected with job gains of 25k 3m/3m vs 91k expected. However, HMRC's PAYE data indicate a 356k surge in payrolls for June. Further fueling the debate on inflation, average weekly earnings (inc bonuses) pushed up to 7.3% Y/Y in May, up from 5.6% the previous month.

- Bunds have been bid with yields broadly 1-2bp lower on the day and the curve 2-3bp flatter.

- The OAT curve has similarly bull flattened with the 2s30s spread 2bp narrower.

- BTPs have firmed slightly, but have lacked much direction with trading near yesterday's close.

- Supply this morning came from France (OATs, EUR10.497bn & Linkers, EUR1.73bn), Spain (Bonos/Oblis, EUR5.366bn), Ireland (ITBs, EUR750mn).

EUROPEAN ISSUANCE UPDATE

FRANCE AUCTION RESULTS - MT OATS

| Coupon | 0% | 0% | 2.75% | 0.75% |

| Maturity | Feb-24 | Feb-26 | Oct-27 | Nov-28 |

| Instrument | OAT | OAT | OAT | OAT |

| Amount | E4.457bln | E2.57bln | E1.82bln | E1.65bln |

| Previous | E4.789bln | E3.098bln | E1.485bln | E2.405bln |

| Avg yield | -0.63% | -0.52% | -0.42% | -0.30% |

| Previous | -0.53% | -0.48% | -0.57% | -0.03% |

| Bid-to-cover | 2.31x | 2.45x | 2.39x | 2.73x |

| Previous | 2.49x | 2.09x | 2.20x | 2.28x |

| Price | 101.650 | 102.450 | 120.150 | 107.840 |

| Previous | 101.470 | 102.390 | 123.480 | 105.860 |

| Pre-auction mid | 101.633 | 102.397 | 120.088 | 107.767 |

| Previous | 101.447 | 102.340 | 105.792 | |

| Previous date | 20-May-21 | 18-Mar-21 | 19-Nov-20 | 20-May-21 |

FRANCE AUCTION RESULTS - LINKERS

| 0.10% Jul-31 OATei | 0.10% Jul-36 OATei | |

| Amount | E995mln | E735mln |

| Previous | E897mln | E950mln |

| Avg yield | -1.43% | -1.21% |

| Previous | -1.27% | -0.96% |

| Bid-to-cover | 2.21x | 2.26x |

| Previous | 2.20x | 2.32x |

| Price | 116.61 | 121.79 |

| Previous | 114.81 | 117.34 |

| Pre-auction mid | 116.487 | 121.583 |

| Previous | 114.691 | 117.133 |

| Previous date | 17-Jun-21 | 20-May-21 |

SPAIN AUCTION RESULTS: 3/7/10/15-year Bonos/Oblis

| Coupon | 0.25% | 0% | 0.50% | 4.20% |

| Maturity | Jul-24 | Jan-28 | Oct-31 | Jan-37 |

| Instrument | Bono | Bono | Obli | Obli |

| Amount | E1.292bln | E1.617bln | E1.424bln | E1.033bln |

| Previous | E1.353bln | E2.164bln | E8bln | |

| Avg yield | -0.47% | -0.08% | 0.35% | 0.67% |

| Previous | -0.10% | 0.01% | 0.54% | |

| Bid-to-cover | 2.80x | 1.63x | 1.79x | 1.52x |

| Previous | 2.26x | 1.16x | ||

| Price | 102.214 | 100.544 | 101.464 | 151.835 |

| Previous | 101.613 | 99.922 | 99.579 | |

| Pre-auction mid | 102.127 | 100.482 | 101.348 | 151.627 |

| Previous | 99.882 | |||

| Previous date | 09-Jan-20 | 17-Jun-21 | 22-Jun-21 |

IRELAND AUCTION RESULTS: 5-Month ITBs

| Type | 5-month ITB |

| Maturity | Dec 20, 2021 |

| Amount | E750mln |

| Target | E750mln |

| Previous | E750mln |

| Avg yield | -0.62% |

| Previous | -0.62% |

| Bid-to-cover | 2.1x |

| Previous | 2.45x |

| Previous date | Jun 17, 2021 |

FOREX - Dollar stays offered

USD trade in negative territory in G10, albeit still flat against NZD, AUD and SEK.

- US yields have drifted lower, providing some better selling interest in the Greenback.

- It has been a mixed early session for the Pound, initially went bid on the Govie open, but fully reversed during the cash Equity open on Asos falling over 10% on profit warnings, hurting sentiment.

- The pound has since, once again reversed its price action, with Cable back in the Green on the broader base offered Dollar.

- Safe haven FX, CHF and JPY are leading against the USD in G10s, up 0.47% and 0.33% respectively.

- Big selling in the German Dax, dragged Equities lower, following Siemens Gamesa falling some 15% on profit warning.

- Equities have since recovered some ground.

- Looking ahead, US, IJC, Phili Fedf and IP are the notable data.

- Speakers include, ECB Lagarde and Yellen releasing podcast conversation, BoE Saunders, Fed Evans, and Powell this time before Senate,

FX OPTION EXPIRY

FX OPTION EXPIRY (updated, closest ones)

Of note: AUDUSD 2.15bn at 0.75- EURUSD: 1.1800 (653mln), 1.1805 (250mln), 1.1900 (372mln), 1.1910 (366mln)

- USDJPY: 109.80 (500mln), 109.90 (200mln), 110.05 (545mln), 110.10 (370mln), 110.35(284mln)

- AUDUSD; 0.7470 (249mln), 0.7500 (2.15bn)0.7510 )297mln)

- USDCAD: 1.2500 (421mln)

Price Signal Summary - Bunds Are Approaching The Bull Trigger

- In the equity space, bullish conditions remain intact in the S&P E-minis. Attention is on 4400.00 next. EUROSTOXX 50 futures remain above last week's low of 3951.50. The contract is trading near initial resistance at 4101.50, Jul 1 high where a break would neutralise recent bearish price signals and signal scope for a stronger recovery.

- In FX, the USD outlook remains bullish. EURUSD resumed its downtrend Tuesday, breaching the recent low of 1.1782, Jul 7 low. The focus is on 1.1704, Mar 31 low. Gains are considered corrective. Resistance is at 1.1881, Jul 9 high. The GBPUSD outlook remains bearish. The focus is on the support and bear trigger at 1.3733, Jul 2 low. Resistance is at 1.3937, the 50-day EMA. USDJPY failed to hold onto yesterday's high and tackle resistance at 110.82, Jul 7 high. The reversal lower suggests the recent 3-day recovery has been a correction and is over. Support at 109.53, Jul 8 low and the short-term bear trigger appears exposed.

- On the commodity front, Gold has overcome resistance offered by the 50-day EMA. The break higher strengthens bullish conditions with attention on $1833.7 (tested this morning) and $1853.3, 50.0% and 61.8% retracement levels of the Jun 1 - 29 decline. Brent (U1) futures are lower and attention turns to support at $72.11, Jul 8 low. A break would be bearish. WTI (Q1) key support to watch is at 70.76, Jul 8 low.

- Within FI, Bund futures have recovered off yesterday's low. Conditions remain bullish. Attention is on 174.77, Jul 8 high and the bull trigger. A break would open 174.97, Mar 3 high (cont). Gilt futures found support at yesterday's low. Broader conditions are bullish and the recent pullback is considered corrective. Attention is on 129.92, Jul 8 high and the bull trigger.

EQUITIES: Weakness across European and US indices

- Japan's NIKKEI down 329.4 pts or -1.15% at 28279.09 and the TOPIX down 23.55 pts or -1.2% at 1939.61

- China's SHANGHAI closed up 36.089 pts or +1.02% at 3564.59 and the HANG SENG ended 208.81 pts higher or +0.75% at 27996.27

- German Dax down 170.7 pts or -1.08% at 15611.49, FTSE 100 down 42.34 pts or -0.6% at 7049.73, CAC 40 down 50.05 pts or -0.76% at 6509.52 and Euro Stoxx 50 down 39.34 pts or -0.96% at 4058.46.

- Dow Jones mini down 134 pts or -0.38% at 34678, S&P 500 mini down 14.5 pts or -0.33% at 4352.25, NASDAQ mini up 12 pts or +0.08% at 14905.25.

COMMODITIES: Oil lower, copper higher

- WTI Crude down $0.86 or -1.18% at $72.3

- Natural Gas up $0.00 or +0.03% at $3.662

- Gold spot down $0.6 or -0.03% at $1825.63

- Copper up $3.15 or +0.74% at $429.9

- Silver up $0.02 or +0.07% at $26.2526

- Platinum up $8.04 or +0.71% at $1139.67

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok