Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Markets wary of any further Archegos fallout

- Equity indices stable, but off Friday highs

- Focus turns to Biden outlining US economic plan on Wednesday

US TSYS SUMMARY: On The Front Foot, With Archegos Fallout Eyed

Treasuries are on the front foot to start the week, with the curve seeing some modest bull flattening.

- 2-Yr yield is down 0.2bps at 0.1367%, 5-Yr is down 1.6bps at 0.8492%, 10-Yr is down 2.1bps at 1.6549%, and 30-Yr is down 2bps at 2.3577%.

- Jun 10-Yr futures (TY) up 2/32 at 131-26.5 (L: 131-20.5 / H: 131-31.5), respectable volumes (~360k as of 0630ET).

- The fallout from the Archegos hedge fund blow-up took center stage over the weekend (hitting some bank prime brokerages), though limited spillover into Tsys apart from a sharp fall from session highs this morning following Bunds, as wires reported Deutsche Bank was not as hard hit as some of its peers.

- Stock futs a little lower vs Friday's end-of-session jump.

- Also Sunday, WH Press Sec Psaki noted that Pres Biden will split his economic plan into two, laying out infrastructure proposals in Pittsburgh on Weds (details TBA), and other programs (incl health and child care) in April.

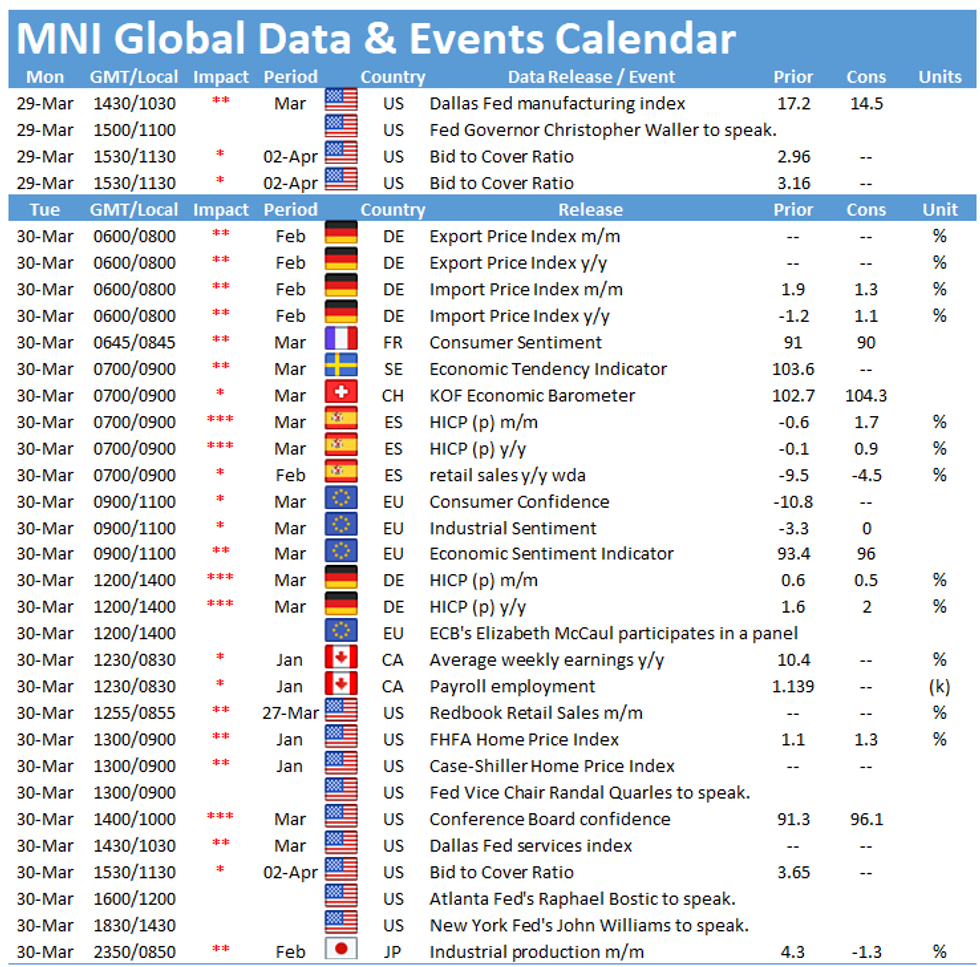

- A quiet schedule today. 1030ET sees Dallas Fed Manufacturing, while at 1100ET Fed Gov Waller delivers his first comments since joining the Board in December.

- In supply, $111B of 4-/8-week bills auctioned at 1130ET. NY Fed buys ~$8.825B of 2.25-4.5Y Tsys.

EGB/GILT SUMMARY: Soft Start

European sovereign bonds have broadly started the week on a soft note, while equities and FX are trading mixed.

- Following a strong open, gilts initially sold off but soon recovered lost ground to trade marginally above the Friday close. The curve is a touch steeper on the back of the short-end outperforming.

- Bunds similarly sold but loss recovery has been limited so far. Cash yields are within 1bp of the Friday close.

- OATs are broadly 1bp higher on the day, with the curve close to flat overall. Last yields: 2-year -0.400%, 5-year -0.6046%. 10-year -0.0974%, 30-year 0.7737%.

- BTPs have underperformed core EGBs with cash yields 1-2bp higher.

- UK mortgage approvals for February came in lower than expected at 87.7k vs 95.0k survey.

FOREX: GBP Bounces Further From Last Week's Low

- GBP is the strongest currency so far in G10, buoyed as the UK takes its first step in unwinding Coronavirus restrictions after a lengthy lockdown. GBP/USD is again testing the 50-dma at 1.3838 after a protracted spell of weakness at the beginning of last week. The GBP strength has pressured EUR/GBP to new 2021 lows, narrowing the gap with 2020's bottom at 0.8282.

- US equity futures are lower, rolling off the sharp rally into the Friday close. This has helped support CHF this morning, rising against most other majors.

- SEK trades poorly, extending the general downtrend seen since the beginning of 2021, helping put EUR/SEK and USD/SEK at the best levels of the year.

- No tier one data crosses Monday, with just a speech from Fed's Waller due. Waller joined the FOMC in December last year, and today's speech will be his first public comments in the role.

FX OPTIONS: Expiries for Mar29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700-15(E610mln), $1.1800(E367mln-EUR puts), $1.1935(E1.1bln), $1.1950(E728mln), $1.2000(E910mln)

- USD/JPY: Y107.00($841mln), Y107.80($708mln), Y108.70-75($1.9bln), Y108.95-109.10($671mln)

- EUR/GBP: Gbp0.8585-90(E1.2bln-EUR puts), Gbp0.8595-0.8600(E835mln-EUR puts), Gbp0.8605-10(E840mln-EUR puts)

- AUD/USD: $0.7700-05(A$519mln)

- USD/CNY: Cny6.51($645mln), Cny6.55($880mln)

- USD/ZAR: Zar15.40($538mln)

Price Signal Summary - USD Maintains A Softer Tone

- In the equity space, S&P E-minis found support last week at 3843.25, the Mar 25. The recovery means the 50-day EMA remains intact. Initial resistance to watch is 3978.50, Mar 18 high. A break would resume the uptrend and expose 4000. Key short-term support is at 3843.25. EUROSTOXX 50 has traded to a fresh trend high today. This reinforces the underlying bullish theme and opens 3889.08, 1.618 projection of Dec 21 - Jan 8 rally from Jan 28 low

- In the FX space, EURUSD maintains a weaker tone. The focus on 1.1752 next, 1.236 projection of the Jan 6 - Feb 5 - Feb 25 price swing. The GBPUSD outlook remains bearish and recent gains are likely a correction. The pair last week cleared a bull channel base drawn off the Nov 2 low. The focus is on 1.3641, 38.2% of the Sep 23 - Feb 24 bull cycle. Resistance, at the former channel base, is 1.3854. USDJPY remains bullish having traded to fresh 2021 highs Friday. The break opens 110.00 and the 110.63 Fibonacci projection, 0.764 of the Mar - Apr 2020 rally from the Jan 6 low.

- On the commodity front, Gold is consolidating with support at $1719.3, Mar 18 low. A break above $1755.50 is needed to trigger a fresh round of gains. This would open the 50-day EMA at $1773.9. A break of support would be bearish. Resistance to watch in Brent (K1) is at $65.12, Mar 22 high. In WTI (K1), the resistance level to watch is $62.04, Mar 22 high. A break off these two hurdles would be bullish.

- In the space, Bunds (M1) are lower this morning however recent gains suggest scope for an extension higher. The next resistance is at 172.78, 0.764 projection of the Feb 25 - Mar 11 - Mar 18 price swing. 171.73, the 20-day EMA marks support. Gilts (M1) last week cleared resistance at 128.33, Mar 16 high, suggesting scope for an extension higher. The next key resistance is at 129.27, Mar 2 high.

EQUITIES: European Indices Mixed, But Bank Stocks Hit

- After the solid close on Wall Street Friday, European indices got off to a good start Monday, before performance turned more mixed ahead of the NY crossover. Germany's DAX and France's CAC-40 are higher by 0.4% or so, while Spain's IBEX-35 is underwater by a similar margin.

- Bank stocks are a laggard across the continent, with banks holding exposure to Bill Hwang's Archegos Capital hit hard from the off. Among the largest decliners are Credit Suisse and Deutsche Bank.

- US futures are softer, with the e-mini S&P lower by just over 15 points as markets roll off the strong close Friday.

COMMODITIES: Oil Steady as Ever Given Partially Refloated

- Oil prices are broadly flat, but came under some early pressure on news that engineers had 'partially' refloated in the Suez Canal - although the ship is still blocking traffic. WTI trades either side of $60.50/bbl, keeping first resistance in tact at last week's $61.36/bbl.

- Silver and gold are a touch lower, with silver prices off just over 1% as markets look to test the 200-dma at $24.7656. Silver fell below the support last week on an intraday basis but recovered ahead of the close. A close below this mark would be a bearish signal, opening a deeper move toward the 2021 low of $24.0570.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok