Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

- Markets more stable after Thursday's volatility

- WTI bounce nixed on Putin positivity

- Canadian jobs report, prelim UMich survey in view

US TSYS SUMMARY: Treasuries Soften On Putin Headline

- Cash Tsys sell-off on a headline from Putin seeing ‘certain positive developments’ in talks with Ukraine before giving back only a small part of the move as a transcript appeared less positive.

- The curve bear flattens on the day as the 2YY touches new post-pandemic highs and unwinds yesterday’s steepening with 2s10s at 26bps.

- 2YY +4.6bps at 1.742%, 5YY +2.8bps at 1.951%, 10YY +2.3bps at 2.009% and 30YY +1.2bps at 2.379%.

- TYM2 sits just 2 ticks lower on the day at 125-30+ on what has been extremely low volumes prior to a pick up on latest headlines. It sits just above support at 125-29 (Feb 25 low) after which it could open the bear trigger of 125-14+.

- Data: Preliminary U.Mich consumer survey for March(1000ET). Focus on inflation expectations after the long-term measure was trimmed a tenth to 3.0% in February.

- No Tsy issuance.

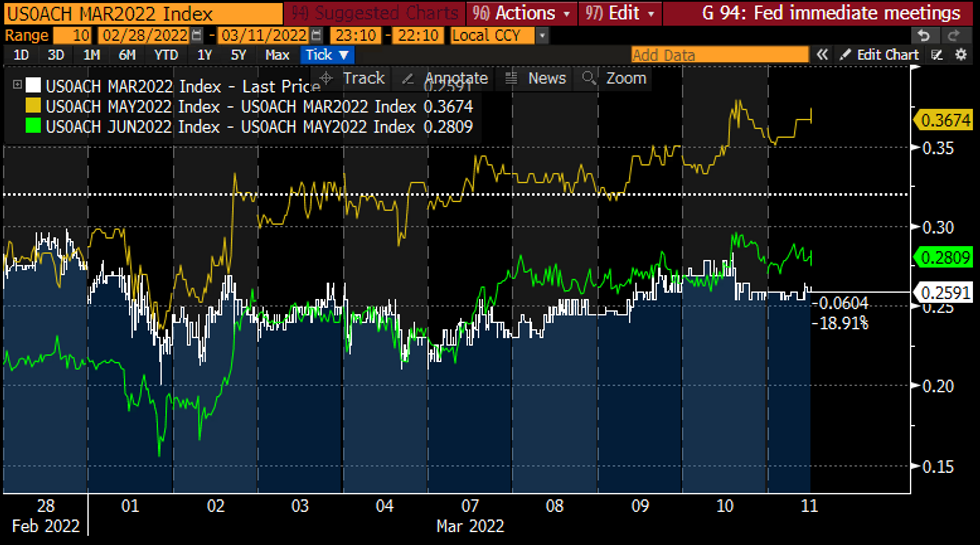

STIR FUTURES: Fed Funds Torn Between 25bp and 50bp In May

- Fed Funds futures pricing sits a little lower than yesterday’s highs on the ECB announcing it will slow asset purchases at a faster pace.

- Next week remains pinned around a 25bp hike (26bp currently), with the market torn between a 25bp and 50bp hike at the May meeting (37bps).

- Cumulative pricing further out sits at 91bps for June and 164bps for Dec.

- The preliminary U.Mich consumer survey for March is the only data of note today with focus on the inflation expectations components after the long-run measure was trimmed a tenth to 3.0% in February.

FOMC-dated Fed Funds futures. Showing pricing for individual meetings with March (white), May (yellow) and June (green)Source: Bloomberg

FOMC-dated Fed Funds futures. Showing pricing for individual meetings with March (white), May (yellow) and June (green)Source: Bloomberg

EGB/GILT SUMMARY: Trading Lower

European government bonds have traded weaker this morning alongside broad gains for equities and energy.

- Gilts initially opened higher and traded weaker through the morning with yields now up 2-3bp.

- It is a similar story for bunds, which have underperformed gilts. Cash yields are 1-5bp higher on the day with the curve bear flattening.

- OATs have traded weaker and the curve has similarly flattened. The 2s30s spread has narrowed 4bp.

- BTPs have lacked clear direction and trade mixed on the day.

- UK monthly GDP surprised sharply higher in January (0.8% M/M vs 0.1% expected) with the index of services, industrial production and construction output all recording faster than expected growth.

- The final estimate of German CPI for February matched the initial print (5.5% Y/Y), while the second estimate for Spain surprised higher (7.6% vs 7.5% expected).

- Supply this morning came from the UK (UKTBs, GBP2bn) and Italy (BTP, EUR7.75bn).

EUROPE ISSUANCE UPDATE

Italy sells:

- E2.75bln 0% Dec-24 BTP, Avg yield 0.570% (Prev. 0.690%), Bid-to-cover 1.52x (Prev. 1.38x)

- E3bln 0.45% Feb-29 BTP, Avg yield 1.470% (Prev. 1.520%), Bid-to-cover 1.39x (Prev. 1.46x)

- E2bln 0.95% Mar-37 BTP, Avg yield 2.11% (Prev. 1.19%), Bid-to-cover 1.37x (Prev. 1.54x)

EUROPE OPTION FLOW SUMMARY:

Eurozone:

RXM2 158.50/157.50ps bought for 22.5 in now 5k total, with 2.5k traded this morning

ERZ2 100/99.75/99.50p fly, bought for 3.25 in 10.8k

FOREX: Markets More Stable After Volatile Thursday

- Markets are more stable early Friday after a volatile Thursday session that saw Wall Street stocks finish with losses of 0.4-0.9%. European indices have inched off the lows ahead of the NY crossover, with most markets higher by 1% apiece. Currency markets are following suit, putting haven FX at the bottom of the pile. JPY underperforms all others, with the USD/JPY rate hitting a new multi-year cycle high overnight of 117.06.

- This puts the pair through the bull trigger at the break of 116.34/35, the Feb 10 / Jan 4 highs. The break higher confirms a resumption of the broader uptrend that started early Jan 2021. Attention turns to highs dating back to Jan 2017 - 117.53, the next objective, is the Jan 9 2017 high.

- AUD trades weaker, with the currency still under pressure after the bearish shooting star candle pattern posted on Monday. Recent weakness still suggests scope for a deeper correction and has exposed 0.7258/20, the 20- and 50-day EMA values and a key support zone.

- Regional currencies in close proximity to Ukraine are faring better, with NOK and SEK looking stable. The greenback

- The Canadian jobs report takes focus Friday, with markets expecting the unemployment rate to shed another 0.3ppts to reach 6.2%. Prelim Uni of Michigan data also crosses, with attention as ever on the inflation expectations component.

FX OPTIONS: Expiries for Mar11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0875-85(E710mln), $1.1200(E1.1bln)

- USD/JPY: Y114.00($526mln), Y114.50($1.2bln), Y114.75-90($1.3bln), Y115.25-30($1.1bln), Y115.75-90($1.4bln), Y116.00($1.9bln), Y116.15-25($1.1bln)

- AUD/USD: $0.7395-00(A$859mln)

- USD/CAD: C$1.2550($860mln), C$1.2710-25($617mln), C$1.2900($1.2bln)

Price Signal Summary - USDJPY Cracks Key Resistance To Resume Its Uptrend

- In the equity space, the trend needle continues to point south however for now, futures are trading above the Jan 24 low of 4094.25 and the key support. A break of this level would confirm a resumption of the downtrend. The 20-day EMA, at 4326.89, represents an important near-term resistance. A break of this EMA is required to suggest scope for a stronger short-term recovery towards the 50-day EMA at 4424.61. EUROSTOXX 50 futures remain vulnerable however a bullish corrective cycle is still in play following this week’s gains. The move higher is allowing an oversold condition to unwind. Resistance to watch is at 3830.60, the 20-day EMA. Clearance of this average would open the 50-day EMA at 3997.70.

- In FX, yesterday’s gains in EURUSD were considered corrective and the pair stalled at the 1.1121 resistance, the Jan 28 low and a recent breakout level. The downtrend remains intact - a resumption of weakness would open 1.0767 next, the May 7 2020 low. GBPUSD has traded lower today registering a fresh cycle low print of 1.3051. This opens 1.2933 next, the Nov 5 2020 low. Today’s key technical development in USDJPY is the break of resistance at 116.34/35, the Feb 10 / Jan 4 highs and a bull trigger. The break higher confirms a resumption of the broader uptrend that started early Jan 2021. Attention turns to highs dating back to Jan 2017 - 117.53, the next objective, is the Jan 9 2017 high.

- On the commodity front, the all-time high print in Gold of $2075.5 on Aug 7 2020 remains intact following Wednesday’s strong sell-off. The broader trend condition is bullish and the pullback is allowing an overbought condition to unwind. The next support is seen at $1961.2, Mar 7 low, while a firmer area of support lies at $1932.9, the 20-day EMA. Oil markets have been volatile this week but remain in an uptrend. The move lower in WTI is allowing the recent overbought trend condition to unwind. The next firm area of support is seen at the 20-day EMA, at $102.20.

- In the FI space, Bund futures maintain this week’s bearish theme. Recent weakness signals potential for a move towards key support at 161.50, the Feb 10 low and a medium-term bear trigger. Gilts have breached a number of important short-term supports this week. This has exposed the key support at 121.10, Feb 16 low.

EQUITIES: DAX Leading European Stocks Higher

- Asian markets closed mostly weaker: Japan's NIKKEI closed down 527.62 pts or -2.05% at 25162.78 and the TOPIX ended 30.49 pts lower or -1.67% at 1799.54China's SHANGHAI closed up 13.655 pts or +0.41% at 3309.747 and the HANG SENG ended 336.47 pts lower or -1.61% at 20553.79.

- European stocks are rising, led by German equities: German Dax up 179.73 pts or +1.34% at 13619.12, FTSE 100 up 76.7 pts or +1.08% at 7175.51, CAC 40 up 46.13 pts or +0.74% at 6247.51 and Euro Stoxx 50 up 31.84 pts or +0.87% at 3682.8.

- U.S. futures are higher, with tech leading: Dow Jones mini up 119 pts or +0.36% at 33271, S&P 500 mini up 19.5 pts or +0.46% at 4277, NASDAQ mini up 66.5 pts or +0.49% at 13652.5.

COMMODITIES: Crude Bounce Nixed on Putin's "Positive Shifts"

- Having slipped lower through the Thursday session, WTI crude futures bounced off the overnight lows to show back above $110/bbl, with reports of a pause for Iranian nuclear talks fueling a modest rally.

- The price action was, however, nixed by comments from Russia's President Putin who, according to Interfax, stated that there are "certain positive shifts in talks with Ukraine". Nonetheless, prices remain above support marked at the overnight lows of $104.50 and $103.63 below.

- The all-time high print in Gold of $2075.5 on Aug 7 2020 remains intact following Wednesday's strong sell-off. The broader trend condition is bullish and the pullback is allowing an overbought condition to unwind. The next support is seen at $1961.2, Mar 7 low, while a firmer area of support lies at $1932.9, the 20-day EMA.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/03/2022 | 0700/0800 | *** |  | DE | HICP (f) |

| 11/03/2022 | 0700/0700 | ** |  | UK | UK monthly GDP |

| 11/03/2022 | 0700/0700 | ** | | UK | Index of Services |

| 11/03/2022 | 0700/0700 | *** | | UK | Index of Production |

| 11/03/2022 | 0700/0700 | ** | | UK | Output in the Construction Industry |

| 11/03/2022 | 0700/0700 | ** | | UK | Trade Balance |

| 11/03/2022 | 0800/0900 | *** |  | ES | HICP (f) |

| 11/03/2022 | 1330/0830 | ** |  | CA | Capacity Utilization |

| 11/03/2022 | 1330/0830 | *** | | CA | Labour Force Survey |

| 11/03/2022 | 1330/0830 | * | | CA | Household debt-to-disposable income |

| 11/03/2022 | 1500/1000 | *** |  | US | University of Michigan Sentiment Index (p) |

| 11/03/2022 | 1500/1000 | * | | US | Services Revenues |

| 14/03/2022 | 0700/0800 | *** |  | SE | Inflation report |

| 14/03/2022 | 0745/0845 | * |  | FR | Foreign Trade |

| 14/03/2022 | 0745/0845 | * | | FR | Current Account |

| 14/03/2022 | 1000/1100 | ** |  | EU | industrial production |

| 14/03/2022 | 1100/1200 | | EU | ECB Elderson Speech at European Banking Institute | |

| 14/03/2022 | - | | EU | ECB Lagarde & Panetta at Eurogroup Meeting | |

| 14/03/2022 | 1500/1100 | ** | | US | NY Fed survey of consumer expectations |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok