Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ECB

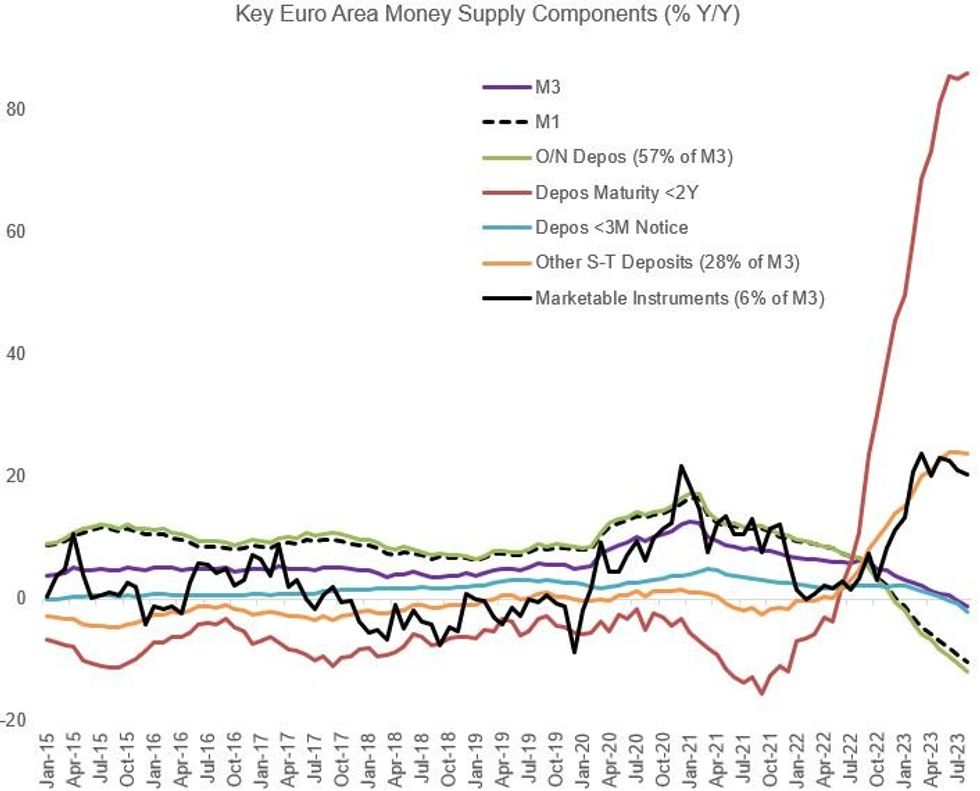

Today's release of August monetary aggregates showed an accelerating pullback in overall money supply growth, including a continued pullback in bank deposits.

- The 1.3% Y/Y M drop in M3 was greater than the -0.4% in July (and a little below the consensus median of -1.0% expected) with M1 at -10.4% (-9.2% Jul). Both were the biggest falls in euro area history.

- The M3 drop was largely on the back of falling overnight deposits, which make up the majority of money supply. Looking bigger picture, M1 money supply (currency in circulation + overnight deposits) has been falling Y/Y since the end of 2021 and is likely to continue so long as interest rates remain elevated vs recent history.

- As the chart shows, sub-3 month notice deposits have started to decline, contrasted with strong growth in deposits maturing in <2Y.

- ECB's Schnabel addressed money market developments in a speech this week, pointing out that M1 rose to 73% of M3 at its peak during the pandemic vs a historical proportion of 40% seen prior to the global financial crisis, due to the low opportunity cost of holding highly liquid deposits over most of the past decade (ie, interest rates were low).

- But that's begun reversing since rates have been rising. Schnabel: "Households and firms are actively and rapidly rebalancing their portfolios towards time deposits and other instruments with higher rates of remuneration, contributing to the sharp fall in M1....Portfolio rebalancing has also resulted in 'money destruction', in the sense that depositors are using bank deposits to purchase instruments outside the scope of M3 from non-money-holding institutions" including government bonds.

- In this regard Schnabel says "considerable further declines in M1 can be expected", potentially on the order of E2trn (vs E10.5trn currently).

- Her conclusion is that rebalancing "will not in itself affect consumption and saving decisions", and the decline in M1 growth "says relatively little about the extent of the slowdown in economic activity in the euro area and the future evolution of inflation."

Source: ECB, MNI Calculations

Source: ECB, MNI Calculations

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok