Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GLOBAL

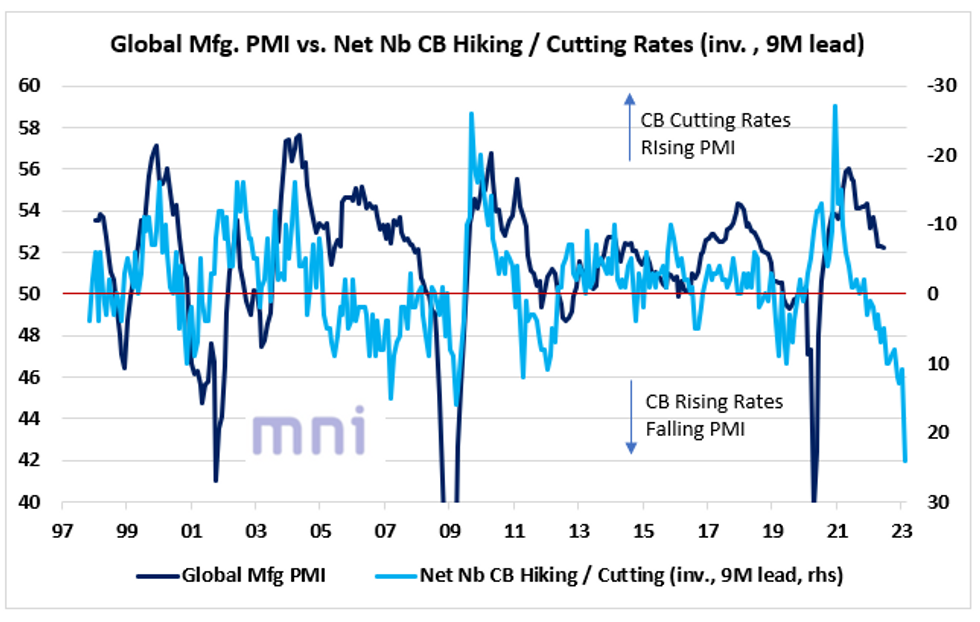

- Since the start of the year, we have seen that a rising number of economic and financial ‘leading’ indicators have been pricing in a significant deceleration in the economic activity in the coming 6 to 12 months.

- Even though the Ukraine war shock is going to accelerate the process, global growth has been slowing down even before the February breakout, leaving market visibility extremely poor in the short to medium term .

- The rise in risk off sentiment particularly since the start of June has led to a surge in price volatility and a strong preference for the US Dollar, with the DXY index breaking above the 107 level yesterday before edging slightly lower.

- The chart below shows that the aggressive tightening run by central banks in the past year is still pricing in a significant plunge in the global manufacturing PMI in the coming months (‘proxy’ for real time growth).

- Out of the 38 central banks tracked by the BIS, 26 raised interest rates in June to tame inflation and support the domestic currency.

- CBR is the only major central bank that cut rates last month, bringing its policy rate down to 9.5%, mentioning in its statement that 'inflation is slowing faster and the decline in the economic activity is of a smaller magnitude' than expected earlier this year.

- Hence, the light blue line represents the net central bank hikes in June (25), which has historically acted as a strong ‘leading’ indicator of the global economic activity.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok