Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CREDIT MACRO

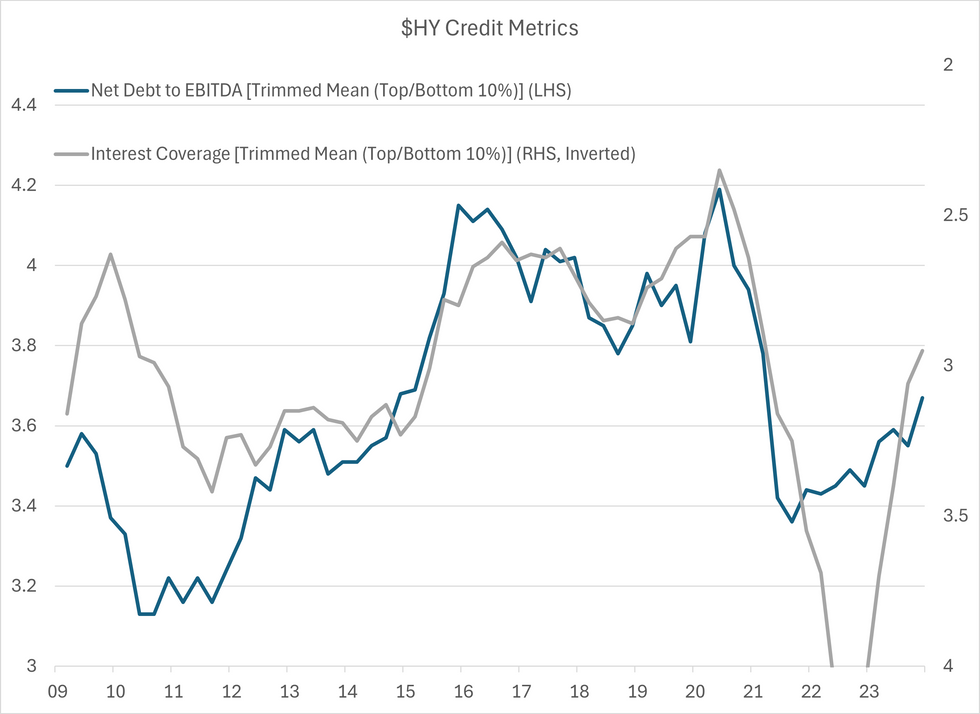

- $HY headlined relatively healthy metrics - Interest coverage fell from 3.1* to 3* - the most muted fall since 2Q 2022. Only sector that showed significant deterioration in ICR's was energy - falling from 5.1* to 4.2*.

- Net leverage however did rise from 3.55* to 3.67* while gross leverage fell - slightly confusing given cash still increased (as % of debt from 12.1% to 12.7%). Jump in net leverage seems to have been driven by Auto's (+0.5*), technology (+0.18*) & Electric (+0.3*).

- No noticeable differences in medians (vs. trimmed means) reported for above.

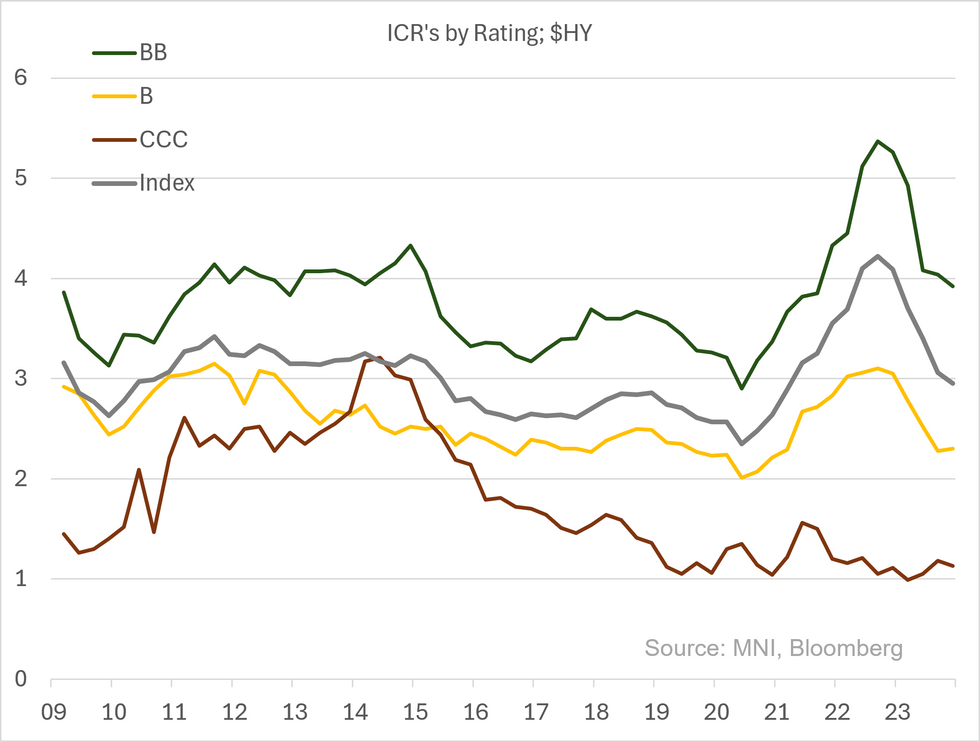

- There were some positives for $CCC credit; ICR's (just) holding above 1* (at 1.1*), FCF to total debt rising to positive levels (-0.8 to +0.6) & cash on hand increasing to highest levels (as % of debt) since Q2 2022. ICR's at ~historic lows does little for pro-CCC arguments that point to historic wides.

- As a aside, Single B's are the best performing in dollar markets YTD (-33bps) - no noticeable change in credit metrics for it in Q4.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok