Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

- Nonfarm labour productivity was roughly as expected in the preliminary Q2 release, falling -4.6% Q/Q saar after -7.4% as output fell -2.1% and aggregate hours worked rose 2.6% in a release that can be used to argue that both GDP should be revised up and/or payrolls revised down.

- With hourly compensation jumping 5.7% (but -4.4% in real terms), ULCs saw a smaller moderation than expected from 12.7% to 10.8% (cons 9.5%).

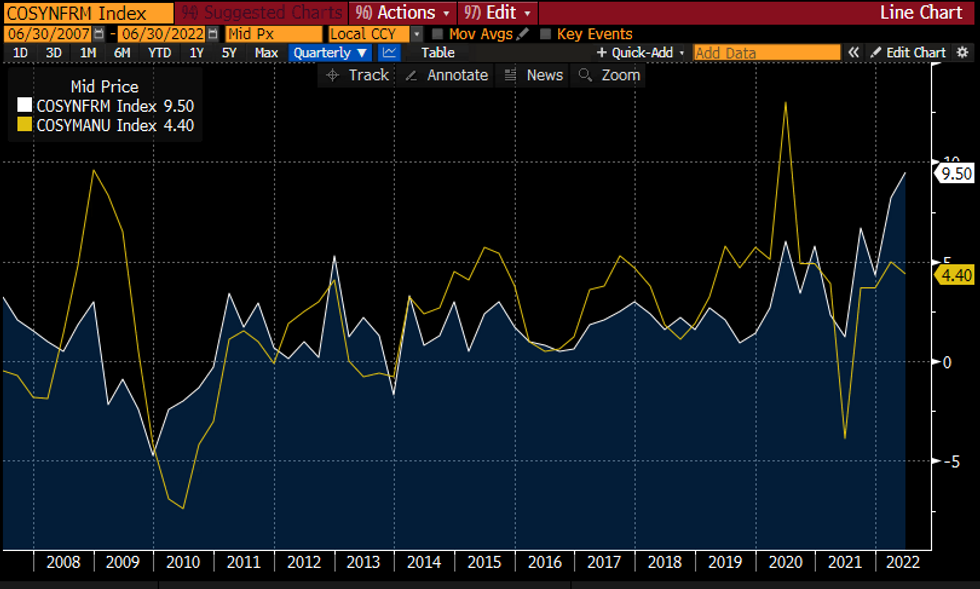

- There are clear differences by industry though, supporting the view of a rotation towards services. Manufacturing labour productivity jumped 5.5% which outside of immediate pandemic distortions pushed the first, admittedly small, decline in mfg ULCs since 2Q18 (-0.5% Q/Q) with Y/Y growth at 4.4% vs 9.5% for all nonfarm business.

- The data have helped drive a pause in the belly-led sell-off in Treasuries, with larger rallies in the belly and long-end on the release leaving the curve with a bear flattening with 2YY +4.2bps and 10YY +2.4bps on the day.

% Y/Y ULC for nonfarm business (white) and manufacturing (yellow)Source: Bloomberg

% Y/Y ULC for nonfarm business (white) and manufacturing (yellow)Source: Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok