Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

USD

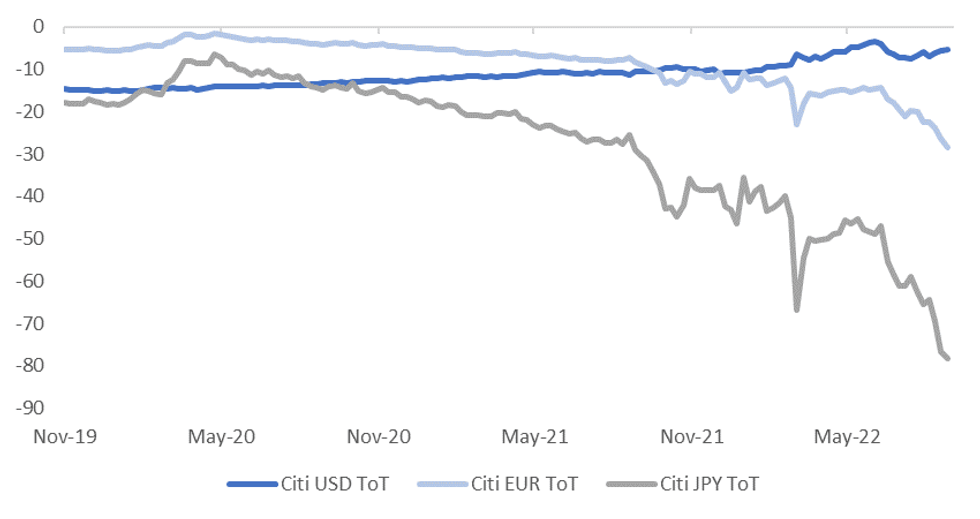

Relative terms of trade trends continue to favor the USD over EUR and JPY. The first chart below plots the Citi terms of trade proxies for each of these currencies. Whilst the USD measure has edged higher in recent weeks, the EUR and JPY measures continue to trend down. It's also not just price measures that are trending wrong for these economies, but also actual supply. This is obviously a focus point for the EU area at the moment and as we approach the winter months.

Fig 1: Citi Terms Of Trade Proxies for USD, EUR & JPY

Source: Citi/MNI/Market News/Bloomberg

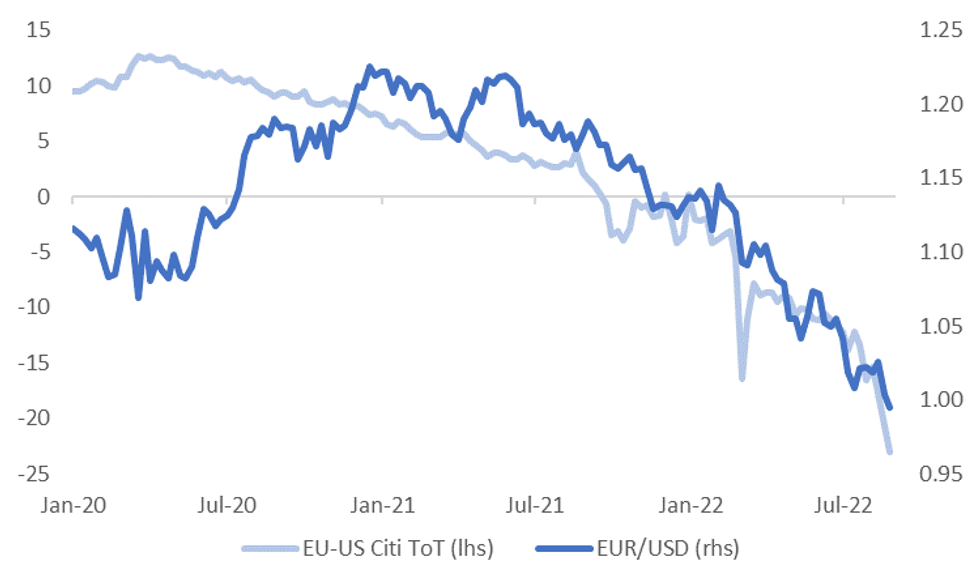

- The second chart below plots the differential between the EU and US Citi ToT proxies, against spot EUR/USD. As we have highlighted previously, the correlation between the two series has strengthened over the past 12 months. The rolling 6 month correlation is only just off recent highs at 72% (versus 80%).

- All else equal, the relative ToT proxy continues to suggest downside in EUR/USD.

- For JPY, the negative terms of trade shock, coupled with record wide trade deficits, has likely helped reduced its sensitivity to broader risk aversion moves, albeit at the margins.

- This year, the USD/JPY correlation with the VIX has been close to flat, but last year it was -37%.

- Relative terms of trade shifts have clearly aided the recent USD's ascent. This support may persist from sometime yet, although focus towards the end of the week will clearly shift to Powell/Jackson Hole.

Fig 2: EUR/USD & Relative Citi EUR-USD Terms Of Trade Proxy

Source: Citi/MNI/Market News/Bloomberg

Source: Citi/MNI/Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok