Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

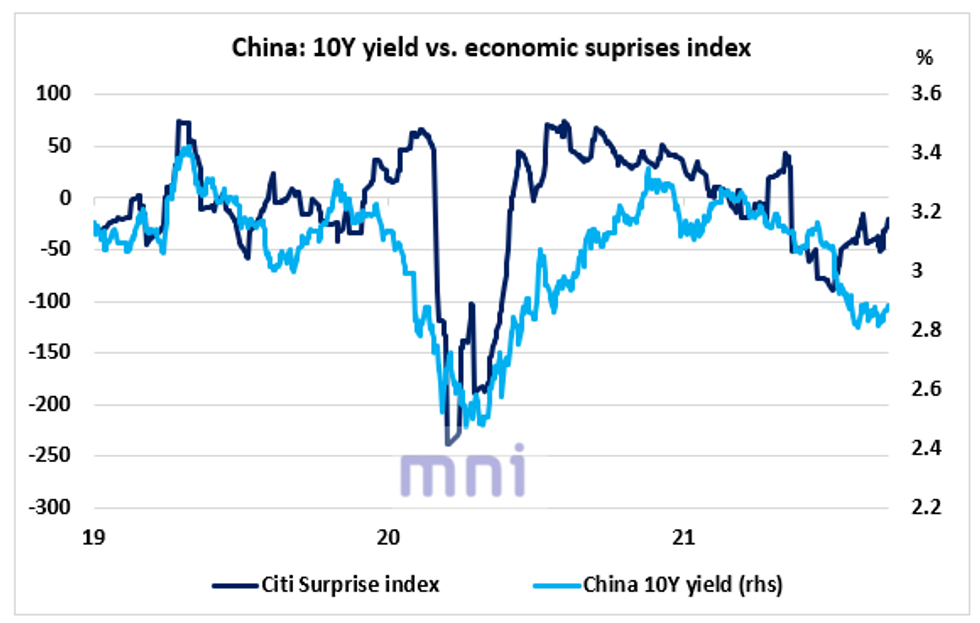

- Since the start of the year, bond investors globally have not been sensitive to the inflation narrative and have been attributing more weigh to the rising uncertainty over the economic recovery.

- We previously saw that while inflationary pressures keep growing in China (PPI rose to 9.5% in August, a 13-year high), the 10Y yield has been constantly trending lower, down 50bps from its November 2020 high of 3.36%.

- However, the chart below shows that China 10Y yield has been more sensitive to the economic surprises index in the past 3 years; a sharp fall in Chinese data has generally been associated with a negative retracement in the 10Y yield and vice versa.

- The sharp contraction in liquidity combined with the rise in contagion risk amid Evergrande 'collapse' are posing a threat to domestic asset prices, which could lead to further downside revisions in growth expectations in the short term.

- Hence, preference for LT government bond yields could continue to remain elevated, limiting the upside consolidation in China 10Y yield.

- The 10Y yield is currently testing its 50DMA at 2.88% ; a break above that level would open the door for a move up to 3% (100DMA). On the downside, key support stands at 2.80%, which represents the 61.8% Fibo retracement of the 2.46% - 3.36% range.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok