Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EMERGING MARKETS

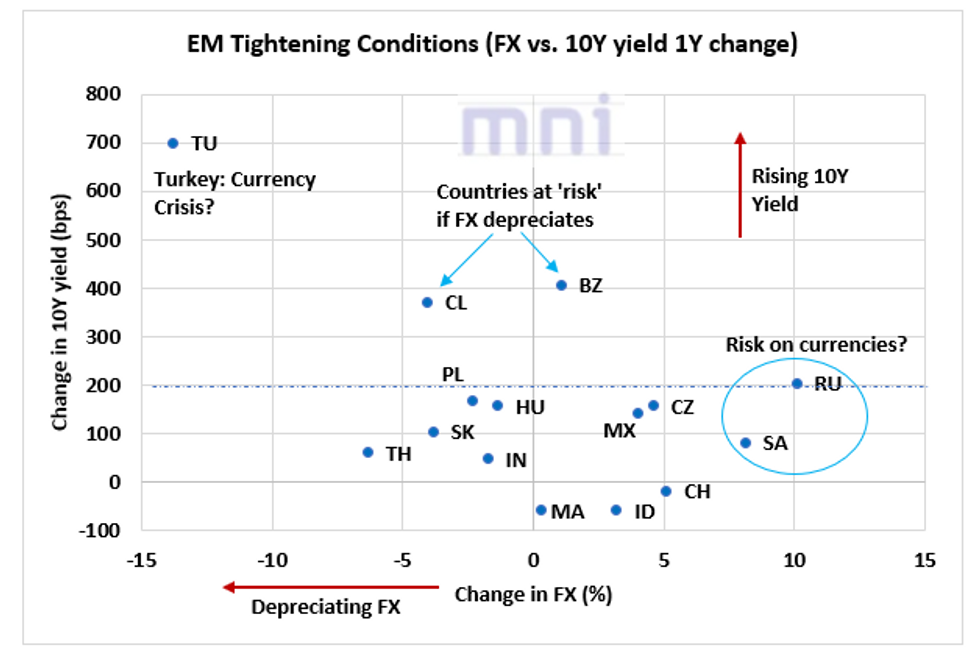

- In the past year, we have seen that the surge in global liquidity combined with the decrease in uncertainty (amid rising vaccination rates) have led to a strong recovery in global asset prices, with an improvement in financial conditions in some EM economies.

- The scatter plot below shows the changes in the 10Y yield (in bps) with the changes in the currency (in %, relative to the US Dollar) for the major EM economies in the past year.

- We have seen that the rise in inflationary pressures since the start of the year has resulted in EM central banks surprising markets by running a more aggressive tightening cycle.

- In the EM world, a sharp tightening in financial conditions with soaring LT bond yields combined with strong depreciation in the currency have historically led to more uncertainty over the economic outlook and generally tends to weigh on risky assets.

- Not surprisingly, Turkey has been the outlier in the EM world, with the lira down nearly 14% and Turkish LT bond yield up 700bps in the past year. Dovish CBRT combined with the surge in economic and political uncertainty have been weighing on Turkish risky assets.

- On the other hand, the global risk-on environment combined with the surge in energy prices have been strongly supportive for ZAR (risk-on currency) and RUB (sensitive to oil prices) in the past year.

- Investors will closely watch the dynamic of the BRL and CLP exchange rates in the medium term; both countries remain vulnerable to currency weakness in the coming weeks after the 10Y yield of each country is up by approximately 400bps in the past 12 months.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok