Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Turkey Central Bank

Executive Summary

- The CBRT is facing an acute currency crisis with markets now anticipating emergency hikes or FX interventions & unconventional policy tools as the lira devalues at an accelerating clip on ultra-loose monetary policy settings.

- Deanchored expectations, alongside increased dollarisation and weak monetary policy credibility, continue to provide snowballing risks to the inflation outlook and further TRY weakness in the absence of real policy rates.

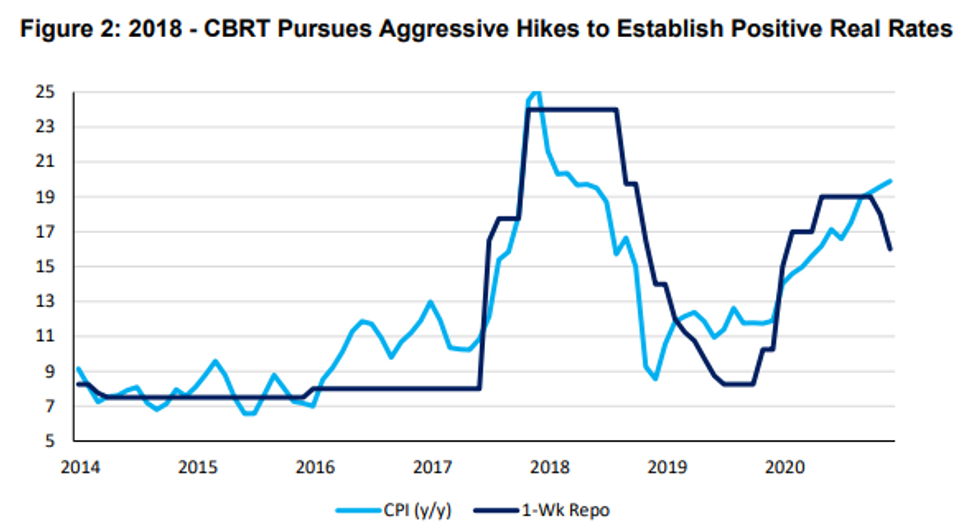

- With 2018 in mind, the establishment & maintenance of real policy rates provides a potential solution, but clashes with Erdogan's political ambitions ahead of 2023 elections - placing a theoretical cap on emergency hikes around +400-500bp

- Turkey's policy difficulties are likely to continue as long as Erdogan remains in power with sole control over the leadership structures at the CBRT - keeping TRY assets in a self-fulfilling cycle of depreciation until a credible policy framework can be established.

Full Preview Here:

TRY Currency Crisis - 24.11.21.pdf

Turkey currently faces an inordinately difficult task of anchoring inflation expectations and re-establishing CBRT credibility in the face of broad, and accelerating currency weakness. This leaves the CBRT with a stark menu of policy options from which to choose to stem the risks to the real economy. Among the best options are delivering positive real rates through a series of large emergency rate hikes, but the bank could also resort to previously used non-standard policy tools to counter TRY weakness. These include rate corridors, tweaking reserve requirements at state banks, clamping down on currency speculation and the likely last resort: capital controls

MNI London Bureau | +44 020-3983-7894 | murray.nichol@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok