Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

USD

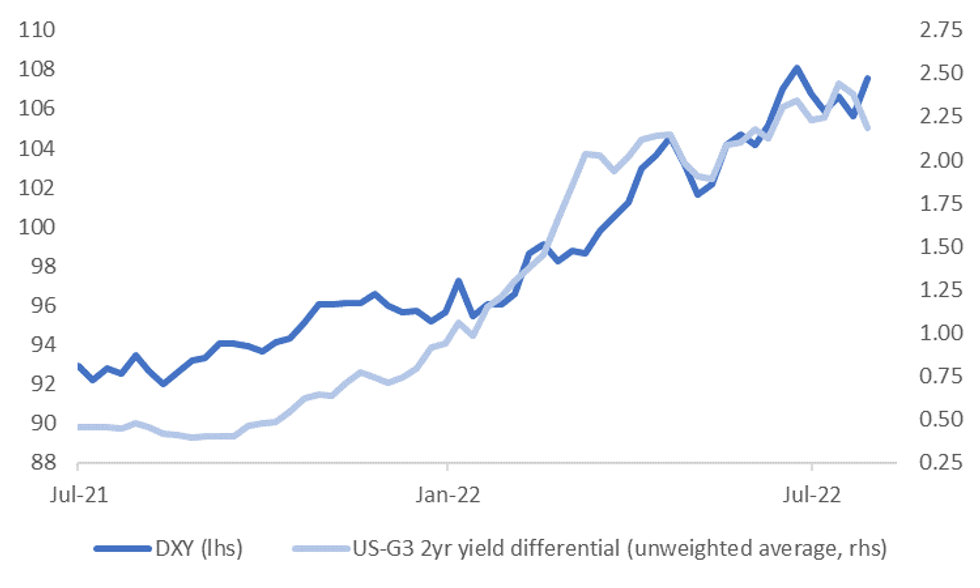

Current levels of the DXY index, near 107.60, would put weekly gains for the USD at just over 1.80%. This would be the strongest weekly gain for the index since early June. This week's strength is a little at odds with relative yield momentum. The first chart below overlays the DXY against the US-G3 average yield differential for the 2yr tenor. This is the opposite image to when we last presented this chart, when the USD index looked too low relative to yields.

Fig 1: DXY Index Versus US-G3 Yield Differential (2yr Tenor, Unweighted Average)

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

- This past week the yield differential has dropped by around 20bps for the 2yr tenor, on average. Looking at the 10yr yield differential points to a more modest drop of 5bps over the past week. However, the correlation has been stronger with the 2yr differential this year (91%), versus the 10yr (78%).

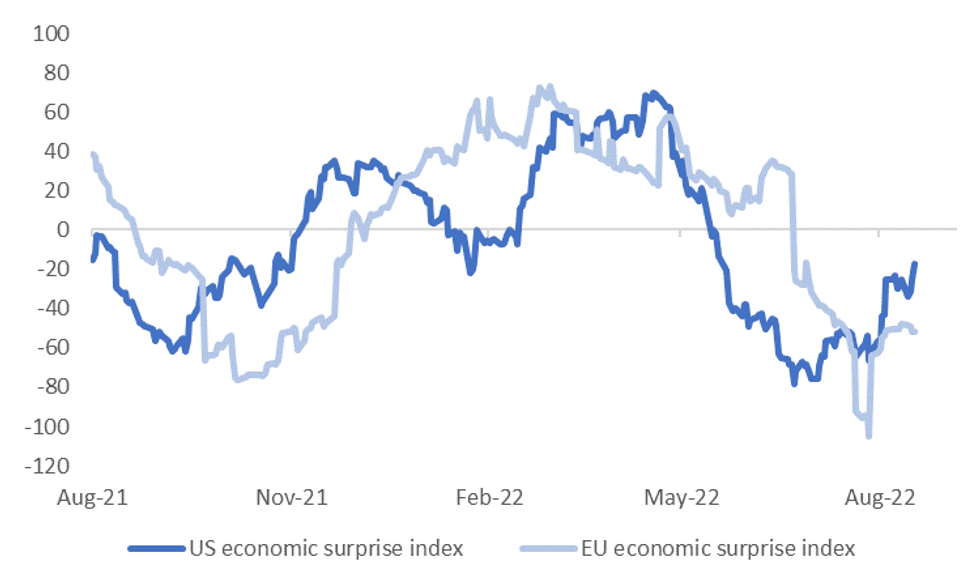

- One clear positive for the USD has been the on-going improvement in data momentum, at least at the aggregate level. The second chart below plots the Citi EASI readings for both the US and the EU. China's EASI is also off recent highs given the weaker than expected activity data from the start of the week. The bias has been to further revise down 2022 growth expectations for China.

- Although obviously such trends haven't been reflected in relative yield performance over the past week.

- All else equal, we might expect upside USD momentum to ease if we don't see some catch up in the yield space. On-going positive data surprises would help, but clearly there will also be a lot of focus on next week's Jackson Hole symposium, where Chair Powell will speak on Friday (the 26th of August).

Fig 2: Citi US & EU EASIs

Source: Citi/MNI/Market News/Bloomberg

Source: Citi/MNI/Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok