Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

TWD

USD/TWD continues to push higher, the pair last 31.30/35, +0.30% for the session so far. This puts spot levels back to mid November levels from last year. The pair is comfortably above all key EMAs, with the rising 20-day last just above 31.00. The 1 month NDF sits close to spot levels, last at 31.33, down slightly from NY closing levels on Thursday.

- Levels wise for USD/TWD, early Nov levels from last year in the 31.65/31.95 region may beckon as an upside target. On the downside, outside of the 20-day EMA, early July lows came in just under 31.10.

- Cross asset headwinds persist for TWD. Local equities are down a further ~1% today. Yesterday saw just over $1.3bn in offshore equity outflows, the largest single outflow day since early June last year.

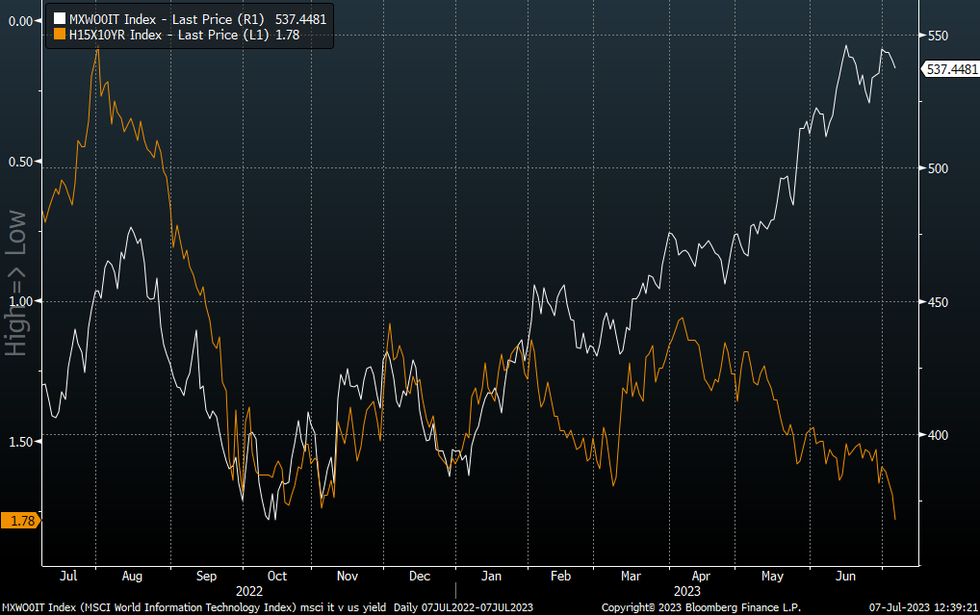

- The chart below overlays the US 10yr real yield (inverted on the chart) against the MSCI IT equity index. The move higher in real yields is starting to take some of the wind out of the equity rebound seen in recent months. Taiwan's TWSE has a 38.90% weight for the semi-conductor index, so some spill over could be expected to local equities and TWD if current US yield trends persist.

- On the data front, later today we have June trade figures. Export growth is expected at -15.7% y/y, an improvement on the prior -21.7% y/y. Yesterday, June CPI came in a touch below expectations (1.75% y/y, forecast 1.80%).

Fig 1: US Real Yield (Inverted) Versus MSCI IT

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok