Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE

Recent data suggests that the Eurozone labour market - arguably the strongest element of the bloc's economy right now - has turned the corner in a softening direction, after an extended period of unexpectedly solid employment growth. Today's PMIs were a case in point, showing the first fall in the Eurozone employment subindex in almost three years.

- However, the deterioration in actual employment levels and unemployment rates has been slow-moving and it's unclear whether it will be fast enough to give the ECB confidence it is on track to hit its inflation target, until further evidence develops later in 2024.

- November PMIs for example showed stubbornly high input costs for services firms, which is primarily a wage issue, and the EC services surveys suggests more optimism on hiring going forward. And while wage growth is slowing, it is still well above levels consistent with 2% inflation.

- “If wage growth remains at a level that is not compatible with the 2.0%, there is unfortunately nothing we can do even if there is a recession... with wage growth of around 5%, we will not lower interest rates — even if the economy shrinks slightly,” Belgian central bank Governor Wunsch told Boersen-Zeitung in an interview published today, as cited by Bloomberg.

- ECB Chief Economist Philip Lane in May 2022 provided a rough guide to assessing wages vs productivity vs inflation: "under typical conditions and allowing for labour productivity growth at about one per cent, nominal wage growth at three per cent is consistent with the two per cent inflation target".

- Two problems in that formula for achieving the 2% target: nominal wage growth is well above that cited level, and productivity is well below that level.

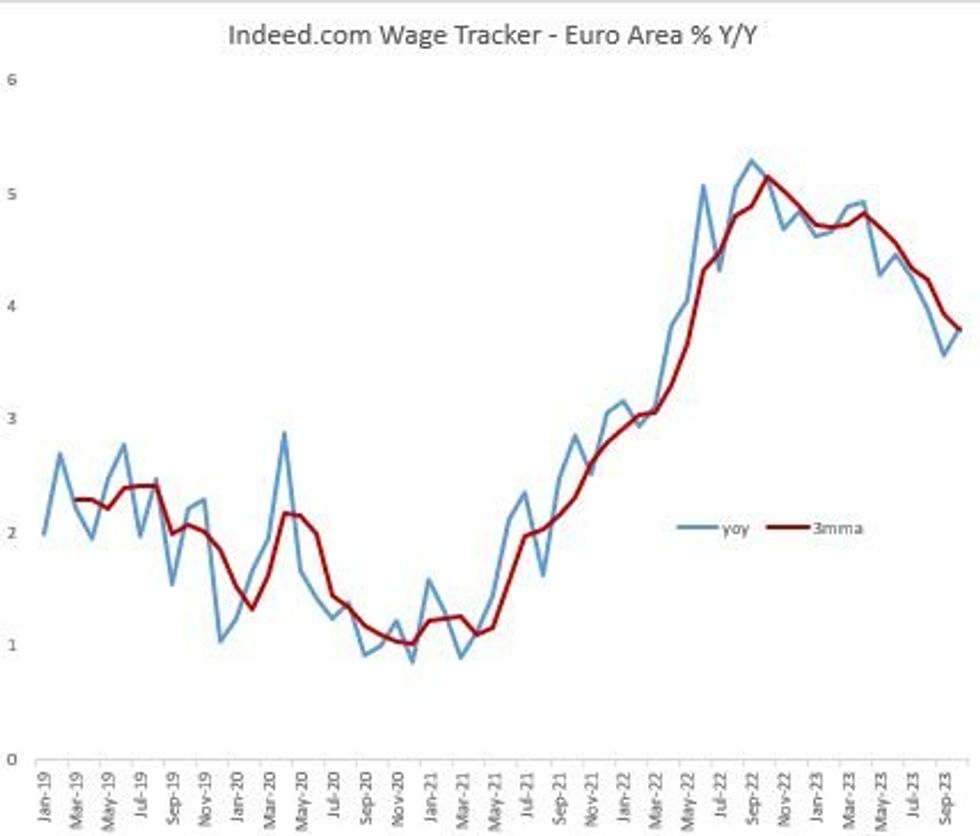

- By all metrics, wage growth remains well above-average going into Q4 2023. The ECB's negotiated wages tracker showed 4.7% growth in Q3, with national central banks showing 5-6% growth in wages implied by agreements reached for 12 months ahead; the Indeed.com Wage Tracker based on job adverts, often cited by ECB economists as a more up-to-date measure, showed a 3.8% Y/Y rise in October.

Source: Indeed.com, MNI

Source: Indeed.com, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok