Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

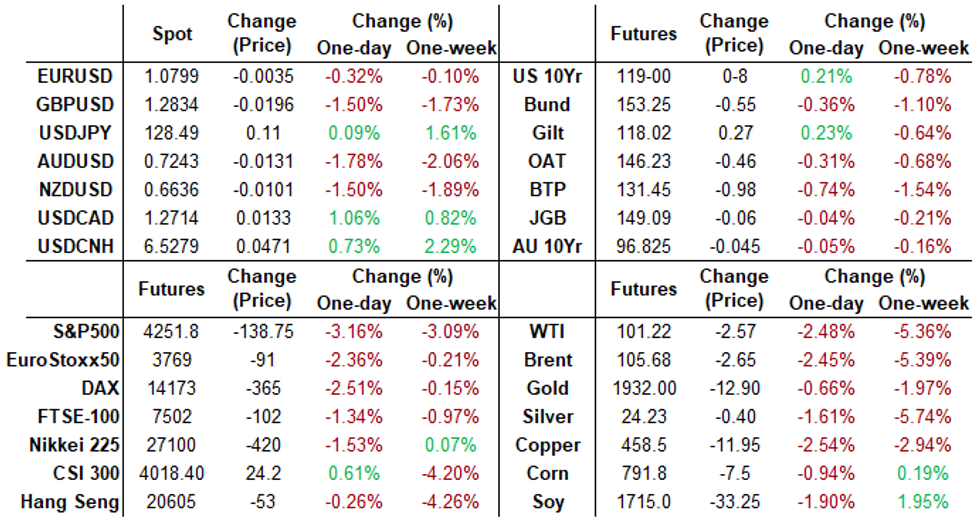

Cleveland Fed Mester Pushes Back on 75Bp May Hike, Favors 50Bp

Rates trade modestly higher after the bell, recovering a portion of Thursday's sell-off. Bonds see-sawed +/- a few ticks around steady in early trade before making session highs around 1000ET, 30YY slipped to 2.8850% before climbing and holding a range from noon on around 2.9470%.- Short end rates were under pressure for much of the session recovered slightly after the bell as Cleveland Fed Mester pushed back on any need for 75bps hike at May 4 FOMC, in favor of 50bp moves.

- Curves bounced off flatter levels: After tapping 42.0 ahead Mon's open, 2s10s fell to 14.108 low in the first half as markets price in the off chance of 75bp hike at the May 4 FOMC. Bbg noted Fed Swaps priced in 250bp in hikes by year end.

- Nomura analysts anticipate the Fed to make two consecutive 75bp hikes (June and July) after a 50bp hike on May 4:

- "For some time, our view has been that if the Fed could hike 200bp at one meeting without significantly affecting market functioning, they would. So far, markets have been reluctant to price 75bp hikes, but stronger pricing for such a move would likely ease the path for the FOMC and participants could likely forge a consensus on such action quickly".

- Fed enters Policy blackout at midnight tonight.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.0000 to 0.32643% (-0.00343/wk)

- 1M +0.03557 to 0.70343% (+0.10900/wk)

- 3M +0.02971 to 1.21371% (+0.15100/wk) ** Record Low 0.11413% on 9/12/21

- 6M +0.10214 to 1.82371% (+0.26700/wk)

- 12M +0.16628 to 2.60671% (+0.38514/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.33% volume: $70B

- Daily Overnight Bank Funding Rate: 0.32% volume: $264B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.26%, $906B

- Broad General Collateral Rate (BGCR): 0.30%, $339B

- Tri-Party General Collateral Rate (TGCR): 0.30%, $328B

- (rate, volume levels reflect prior session)

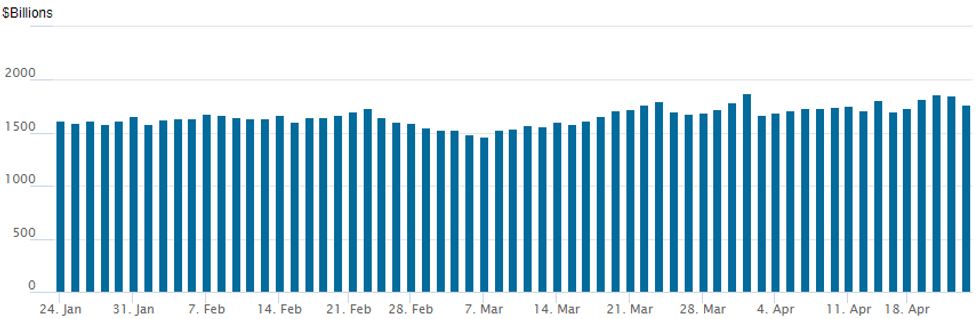

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage receded to 1,765.031B w/ 81 counterparties from prior session 1,854.700B. Compares to all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Gyrations in underlying FI futures Friday spurred buyers of wing insurance (low delta calls and puts), challenging environment for active traders. Bonds see-sawed around steady before rallying around midmorning, curves flattening with short end rates underperforming all session.- Bonds trimmed gains by noon, holding to a narrow range while the short end pared losses after Cleveland Fed President Mester pushed back on any need to hike 75 bp at the May 4 FOMC in an interview on CNBC after the close. Note, lead quarterly Eurodollar futures EDM2 traded 98.11 (-0.065) after the bell vs. 98.050 session low.

- 3,400 Sep 97.75/98.00/98.25/98.50 call condors

- Block, +10,000 Sep 96.00 puts, 7.0 ref 97.275

- Overnight trade

- 5,000 Gold Jul 96.50/96.87 put spds

- 8,500 Sep 97.00 puts, 18.0

- 4,000 Jun 98.25 calls vs. 97.00/97.25 put spds

- Block, 6,000 Dec 95.87 puts, 15.0

- 3,000 Sep 97.12/97.37 put spds

- 12,000 FVM 113/114 1x2 call spds, 5.5

- over 22,000 FVM 114 calls, 12.5-13

- 4,000 FVK 112.75 calls, 1

- 3,000 TYM 117/117.5 put spds, 10

- 2,000 USM 132/136 put spds, 34

- 5,000 FVM 112/113/114 call flys, 18.5

- Block, 12,500 FVM 111.5 puts, 34.5 vs. 7,500 FVM 112.5 puts, 62 at 0916:37ET repeated at 0630ET

- Overnight trade

- 13,600 TYK 118 puts, 3

- 12,200 TYM 115 puts, 13

- 6,600 FVM 111.5/112.5 call spds

- 5,000 FVM 111.5/113/114.5 put flys

- 5,000 TYM 120 puts161-156

- 2,000 TYM 115/117 put spds

FX: Equity Declines See Antipodean FX Plummet, GBPUSD Lowest Since Oct ‘20

- The extended selloff across major equity benchmarks, coupled with the upward pressure on core yields has continued to filter through to currency markets on Friday.

- Weakness in the Chinese Yuan has been persistent throughout the week as concerns over the Chinese growth outlook weighed on the local currency. USDCNY has broken some key technical resistance lines (200DMA, LT downward trending line) and looking at the WoW change (>2%), it represents the biggest move since the August 2015 ‘devaluation’, which generated a market shock with the SP500 falling by over 10%.

- Increased hawkishness towards the FED and the weakening Yuan have added significant headwinds for risk-tied currencies, including the emerging market basket, while continuing to support a bullish outlook for the US Dollar.

- AUD and NZD have been the hardest hit on Friday, both down over 1.5%, as weaker commodity prices contributed towards the perfect bearish storm for Antipodean FX.

- In similar vein, GBPUSD retreated close to 1.5% as sterling also fell victim to the risk-off sentiment. Cable extended aggressively through support and the bear trigger at 1.2974, Apr 13 low, in early European trade and was unable to recover. The break of this level confirms a resumption of bearish activity and an extension of the primary downtrend. Moving average studies also point south, highlighting current market sentiment which saw the pair trade as low as 1.2829 – lowest since October 2020.

- USDJPY remains close to unchanged on Friday, however, headlines continue to spark volatility in the Yen. USDJPY briefly traded back above the 129 handle, narrowing the gap with cycle highs at 129.40, however the pair retraced to around 128.50 approaching the close.

- The Bank of Japan meet next Thursday, a meeting that is garnering a bit more attention given the significant JPY weakening in recent weeks. Immediate focus in the Euro area will be on the French Presidential election results. The last opinion polls to be carried out ahead of the 24 April run-off election between Macron and Marine Le Pen continue to show the incumbent widening the gap in the last stages of the campaign.

Expiries for Apr25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0700(E712mln), $1.0800-03(E521mln), $1.0825(E502mln), $1.0925(E503mln)

- AUD/USD: $0.7350(A$804mln)

EQUITIES: Late Equity Roundup: Bearish Threat Realized

Stocks extending session lows in late Friday trade while earlier vacillations in Treasuries have died down ahead the close.

- SPX eminis have gradually broken several key support levels on the day, through psychological whole-figure support of 4300.0, ESM2 currently at 4282.0, -108.5 (-2.47%) puts late attention on 4247.89 76.4% Fibonacci retracement of the Mar 15 - Mar 29 rally. Beyond that, next key support is at 4129.50 (Low Mar 15).

- Latest earnings cycle that kicked off Monday winds down ahead the weekend. American Express (AXP) and Verizon (VZ), Schlumberger (SLB) and Newmont (NEM) annc'd pre-open, NEM weaker on profit miss/forward guidance.

- SPX leading/lagging sectors: Consumer Staples sector outperformed (-0.63%) lead by household and personal product makers; Materials (-1.35%) and Energy sector (-1.49%) followed.

- Laggers: Industrials and Communication Services near tied (-3.25) followed by Consumer Discretionary (-2.56%)

- Meanwhile, Dow Industrials currently trades -840.47 (-2.42%) at 33952.18, Nasdaq -301.5 (-2.3%) at 12872.68.

- Dow Industrials Leaders/Laggers: Proctor & Gamble (PG) outperformed -- near steady at 162.67, while Coke (KO), JNJ, IBM and Intel between -0.50-0.65. Leading laggers: Caterpillar extends the slide (-16.33 at 216.24), United Health (-13.34 at 524.10) and Goldman Sachs (-11.18 at 323.12)

Stocks saw late buying around lows after Cleveland Fed Pres Mester on CNBC said there's no need for a 75bp hike at the May 4 FOMC. SPX eminis climbed from 4275.0 low to around 4310.0 -- before selling off to 4252.0 low on the close.

COMMODITIES: Oil Ending The Week Down On Demand Fears

- Oil prices are ending the week down almost 5% as demand concerns from ongoing China lockdowns are seen to outweigh lower supply, in particular Russia with April output announced earlier in the week to be down 0.9mln bpd from March at 10.1mln bpd.

- This has come despite US and Canadian producers not being tempted to profit from high prices, with a small increase/decrease in rig counts respectively.

- WTI is -1.6% at $102.11 to leave it down -4.5% on the week where it’s ranged from $100.7 to $109.81, now comfortably below resistance at $109.2 (Apr 18 high) with support still formed by the 50-day EMA of $97.37.

- Brent is -1.6% at $106.62 to leave it down -4.5% on the week. Support is seen close by at $104.65 (Apr 20 low) after which it could open the 50-day EMA of $102.56.

- Gold meanwhile ends the week sharply softer, -0.9% on the day for -2.2% on the week at $1934.04 as Fed hike expectations drive a surge in Treasury yields (2Y up 26bps on last Fri close), taking away some of the allure of gold. Talks between the UN and Putin could be the next geopolitical trigger point.

- With the bearish threat remaining present, it sits closer to support at the 50-day EMA of $1927.5 having fleetingly cleared it earlier. Resistance remains the bull trigger of $1998.4 (Apr 18 high).

- Final mention for European natural gas, -5% today and -10% on the week as the EU has suggested companies could keep paying for it in euros.

Monday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/04/2022 | 0900/1100 |  | FR | Presidential Election 2nd Round | |

| 25/04/2022 | 0700/0900 | ** |  | ES | PPI |

| 25/04/2022 | 0800/1000 | *** |  | DE | IFO Business Climate Index |

| 25/04/2022 | 0900/1100 | ** |  | EU | Construction Production |

| 25/04/2022 | 1000/1100 | ** |  | UK | CBI Industrial Trends |

| 25/04/2022 | 1300/1500 | ** |  | BE | BNB Business Sentiment |

| 25/04/2022 | 1430/1030 | ** |  | US | Dallas Fed manufacturing survey |

| 25/04/2022 | 1500/1100 |  | CA | BOC Gov Macklem testifies at parliamentary committee | |

| 25/04/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 25/04/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 25/04/2022 | 1700/1900 | | EU | ECB Panetta Speech at Columbia University |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok