Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWITZERLAND DATA

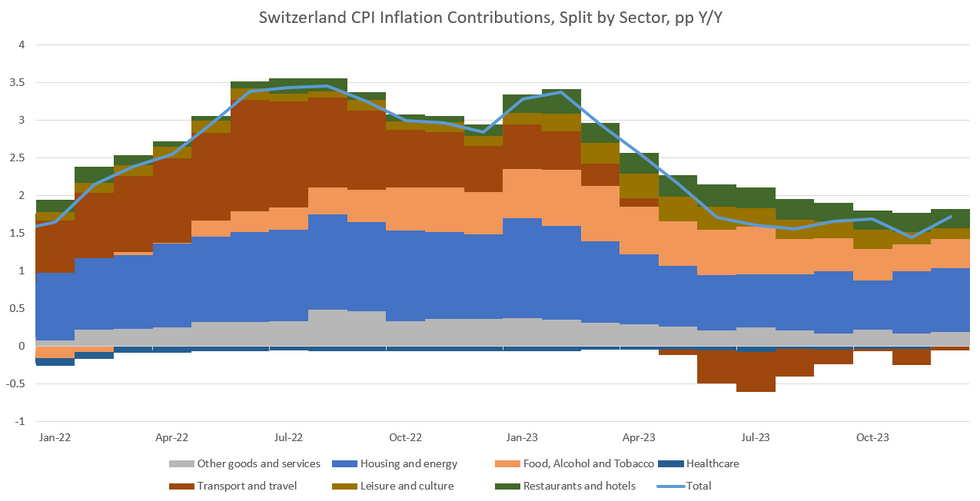

Swiss December CPI came in slightly higher than expected at +1.7% Y/Y (vs 1.6% cons and 1.4% prior) and 0.0% M/M (vs -0.1% cons and -0.2% prior). This puts quarterly average inflation for Q4'23 at 1.6%, meeting SNB expectations from their December rate decision. The core reading came in at +1.5% Y/Y (vs 1.4% cons and prior).

- Looking at individual components, goods prices deflated on a monthly basis (-0.5% M/M), offsettingservices price inflation, which printed at 0.4% M/M.

- On a more granular level, inflation was driven higher by supplementary accommodation (+22.4% M/M, contributing 0.121pp to the headline M/M figure), public long distance transport (+3.7% M/M, +0.045pp), air transport (6.4% M/M, 0.037pp), and hotels (2.5% M/M, 0.036pp). Negative impacts came from petrol prices (-3.6% M/M, -0.056pp), international package holidays (-4.4% M/M, -0.048pp), and medicines (-1.3% M/M, -0.038 pp).

- The SNB expected Swiss inflation to tick up in December and the coming months on higher electricity prices, rents, and VAT (which increased to 8.1% in January from 7.7%). In December, the “housing and energy” compartment of inflation contributed negatively to the total figure, however (-0.1% M/M, -0.026pp contribution).

- The details of the December report thus hint at upside risks to the SNB's latest inflation forecasts which stand at 2.1% and 2.2% for Q1 and Q2’24, respectively. Namely, if the SNB's expectations for increasing electricity and rent price inflation materialize in the months ahead, and the uptick in the accommodation/transport categories persists rather than being a one-off.

MNI, BFS

MNI, BFS

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok