Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

China activity data for October was weaker across the board relative to expectations. IP growth moderated to 5.0% y/y, (5.3% expected, 6.3% prior), while retail sales fell -0.5% (0.7% expected, 2.5%) prior. Fixed asset investment was 5.8% YTD y/y, (5.9% expected and prior outcome same), with property investment remaining a drag -8.8% YTD y/y. Property sales remained around recent lows at -28.2%. The unemployment rate was steady at 5.5%, in line with forecasts.

- The IP detail showed slowing in commodity related sectors (coal, steel etc), while the tech related computer segment continued to weaken.

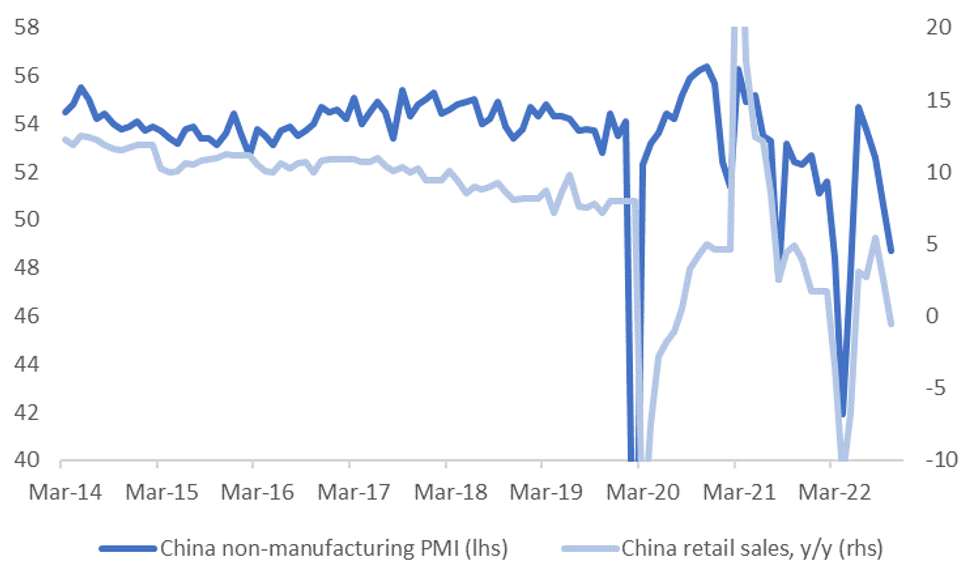

- For retail sales, spending related to outdoor activities fell sharply, in line with covid-related restrictions. A lot of other categories recorded negative y/y prints though signifying a weaker consumer backdrop. The chart below overlays the services PMI against y/y retail sales.

- Private sector FAI was weak (+1.6% y/y, we were at 8.4% y/y in March), with the slack being picked up by state owned enterprises (10.8% y/y). The jobless rate held steady at 5.5% in an encouraging sign for labor market dynamics.

- As the China statistics authorities stated post the release of the data, the foundation for economic recovery is not solid yet. It remains to be seen if the recent policy shifts show up in the next round of survey data (like PMIs etc).

- The impact on China asset sentiment hasn't been large though. USD/CNH spiked above 7.0600 post the data, but is now back to around 7.0470, while China equities are recovering, but overall gains are modest so far.

Fig 1: China Retail Sales Versus Non-Manufacturing PMI

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok