Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

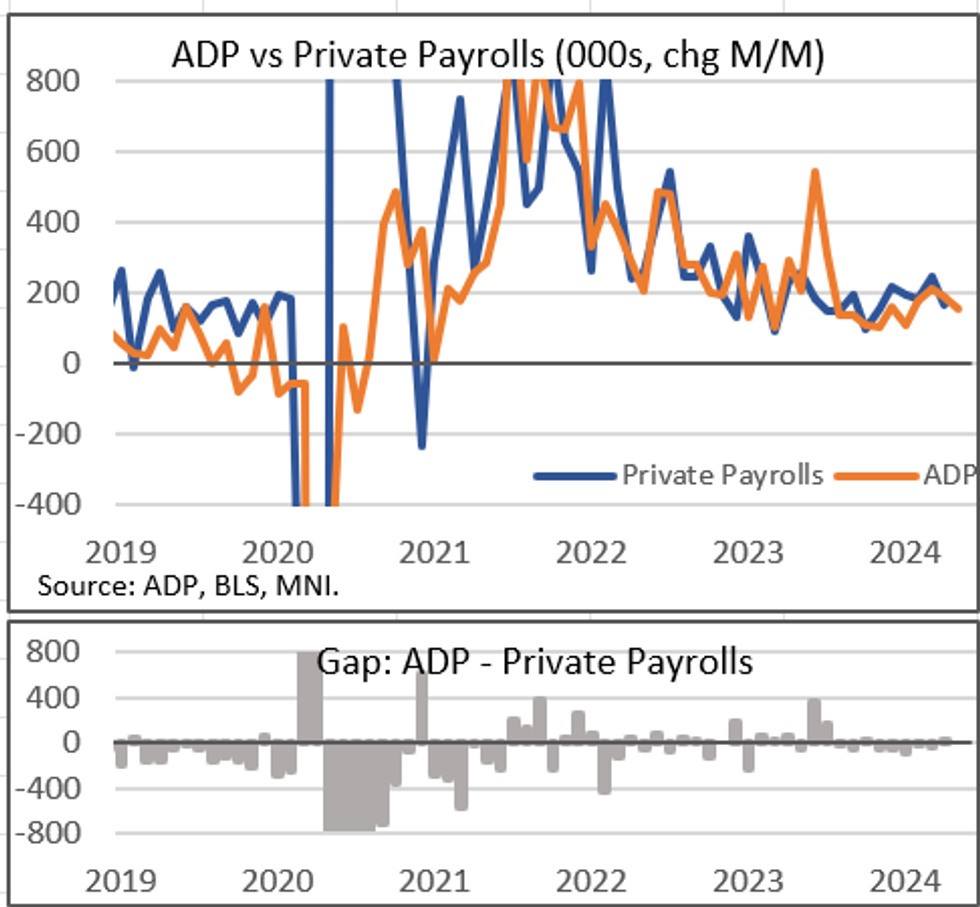

ADP private payroll gains totalled 152k in May, below the 175k consensus and a 4-month low for the series.

- April's figure was only slightly downwardly revised (to 188k from 192k), a moderate change versus previous large revisions.

- Firms with 500+ employees led gains, with +98k (+100k prior), with hiring slowing in firms with 1-49 employees (total -10k vs +37k prior).

- The ADP series hasn't been a great predictor of the corresponding month's private payroll gains in the nonfarm report, but it's been close enough in magnitude to give a sense of general sense, albeit often underestimating the NFP figure.

- April's 192k ADP (pre revision) vs NFP private payrolls 167k was about as close as it got this year, with significant undercounts in the previous 5 months.

- Our early read of private payrolls expectations from sell-side analysts is for +150-170k of a +200k payroll gain (note that this was very close to the ADP consensus), so May's ADP shouldn't move the needle too much for Friday's release.

- If anything, the history of ADP undercounting NFP private payrolls suggest modest upside risks to Friday's figure, though we wouldn't read much into it in any case given the history of large revisions.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok