Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

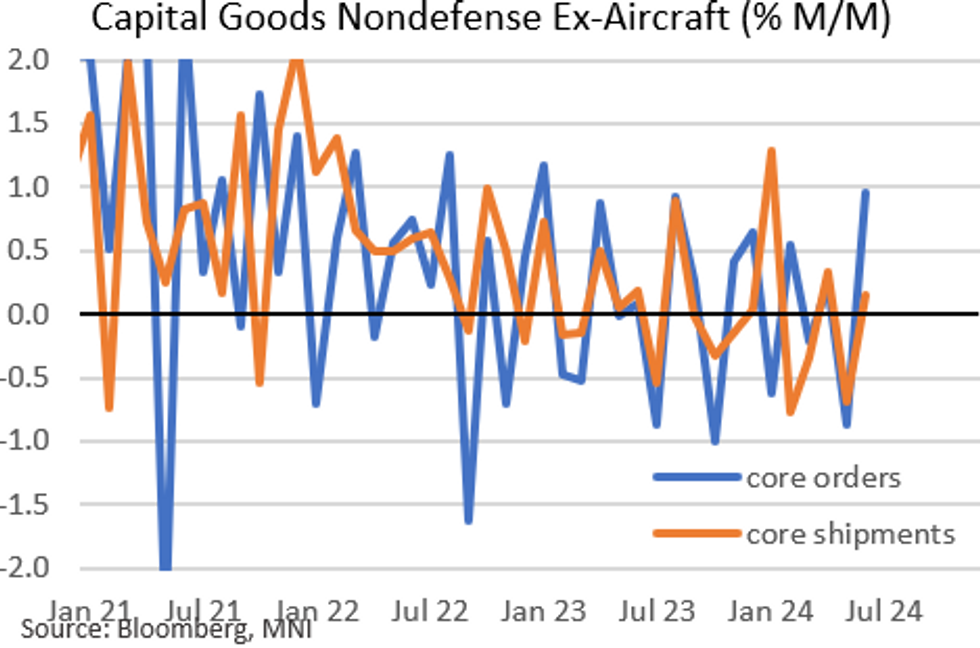

June's advance durable goods report was extremely mixed, with the more important (and less volatile) core readings offsetting severe weakness in overall orders.

- Headline durable goods orders unexpectedly collapsed in June, falling the most (-6.6% M/M vs +0.3% expected, +0.1% prior) since the start of the Covid pandemic (April 2020 -20.0%). The seasonally-adjusted level of durable goods orders thus fell back to levels not seen since November 2021.

- However, this was largely non-core driven: nondefense aircraft and parts came in at -127% M/M, with the level of net orders negative for the first time since July 2020. Note that, separately, per various industry publications, Boeing reported sharply negative net aircraft orders in June, which this may reflect. Excluding transportation, new orders rose 0.5%, which was actually above the 0.2% expected (and -0.1% prior).

- The key nondefense capital goods orders excluding aircraft category saw 1.0% growth, vs 0.2% expected (and reversing May's -0.9% decline, rev from -0.6%). That was the fastest growth rate since January 2023, pushing the series to an all-time high (on a SA basis), though the 3M/3M annualized rate merely steadied out at 0.0% (-0.8% prior).

- In terms of ongoing activity, core shipments bounced back in June to +0.1% from -0.7% in May (rev from -0.5%), though the 3M/3M annualized rate fell further negative, to -2.3% - lowest since July 2020.

- Overall, when stripping out the volatile components, this report suggests flat sequential business investment at the end of Q2, though the overall outlook remains soft.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok