Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

- This week, market will be closely watching China inflation data coming out on June 9 (with CPI and PPI expected to rise to 1.6% and 8.5% in May, respectively) and new updates on Total Social Financing (TSF) and money supply.

- We have seen that China 'liquidity' has been tightening in the past few months with the annual change in the 12-month sum of TSF falling from over 10tr CNY in October 2020 to 3.1tr CNY in April 2021.

- With aggregate financing (combining banking and shadow banking activity) expected to reach 2tr CNY in May, the annual change in 12m sum will then fall to less than 0.5tr CNY (see chart).

- A a reminder, a contraction in Chinese credit and liquidity has generally been marked by a correction in risky assets (such as equities) and commodities in the next 6 to 9 months.

Source: Bloomberg/MNI

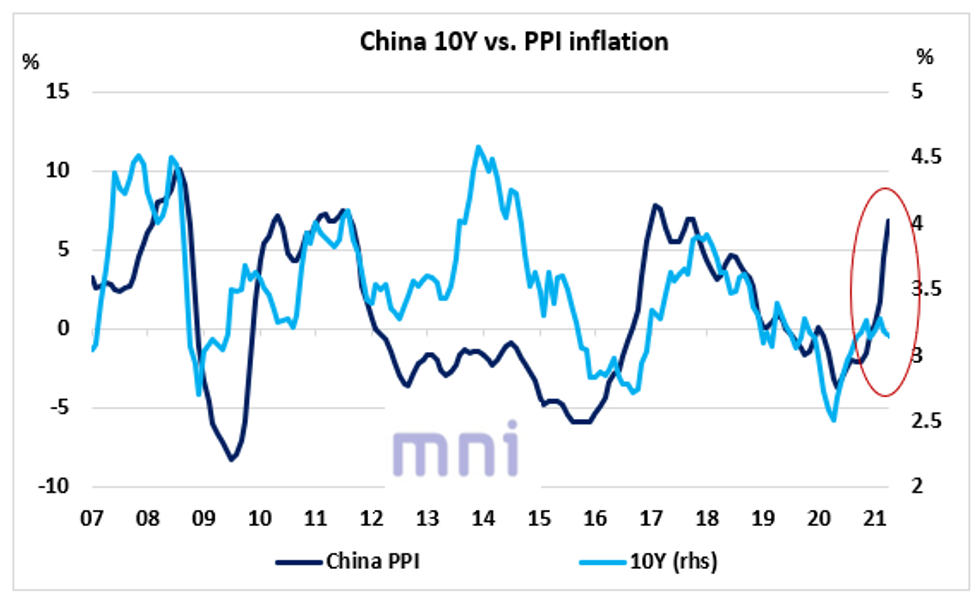

- Interestingly, the spike in China PPI ( which has historically strongly co-moved with China 10Y) has not been followed by an increase in China 10Y yield; the chart below shows the recent strong divergence between the two times series.

- In the past cycle, some investors have been using the PPI inflation as a proxy for China inflation after the relationship between the 10Y and CPI inflation broke down in 2013.

- The 10Y yield has been retracing higher since the start of the month, currently standing slightly below its 50D SMA resistance at 3.15%; next level to watch on the topside stands at 3.18% (100D and 200D SMA).

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok