Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER CYCLICALS

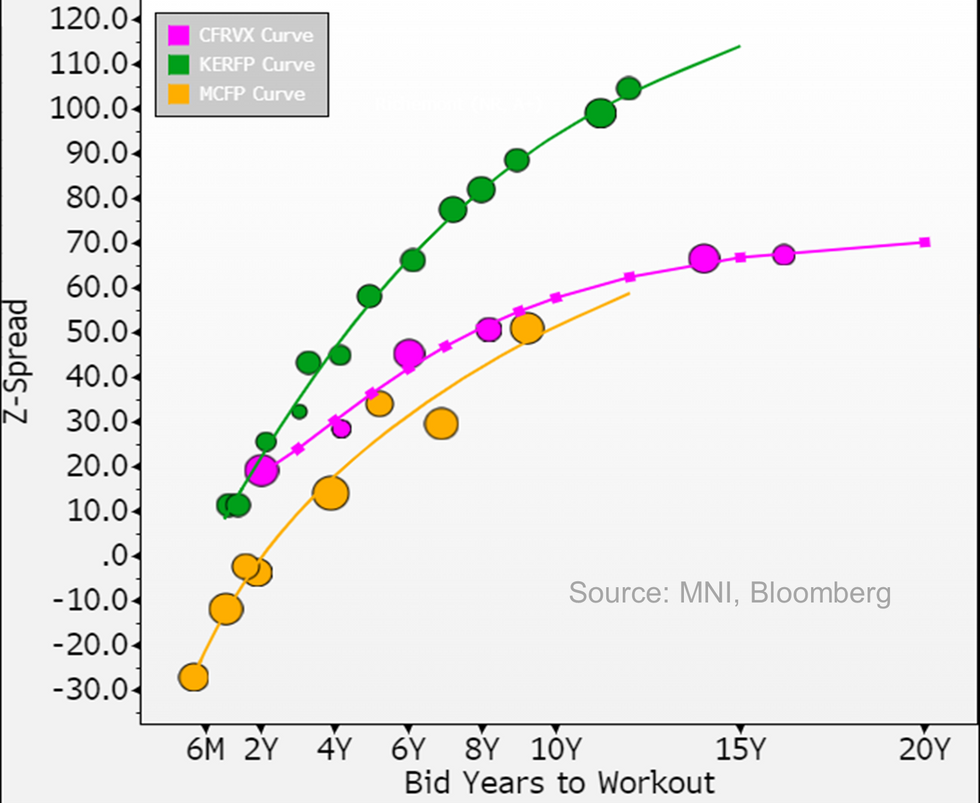

Kering (NR, A Neg) € lines +5-9bps wider & £26/32's +6-7 - firmly priced for downgrade here (which we expect now)

- As an aside Equity {KER FP Equity} sell-off still leaves it higher on the year after a +11% rally that wasn't on fundamentals - we see it currently trading at forward P/E of 15.2 vs. ~14* earlier this year leaving more downside for equities on relative terms.

- On credit; S&P, the sole rater on Kering, moved its outlook to neg in Mid-Feb post FY23 results - spreads did underperform/move wider on it but not the extent of today's moves. On sales it was looking for a "gradual" recovery to +4-6% (headline not organic seems) over next couple of years (2024-25). It expected FY23 FOCF at €2.9b to improve to €3-3.5b this year and €3.5-4b in 2025 - improvements on sales growth, stable capex & normalising WC were the drivers.

- It's fcsts were ~in-line with consensus at the time but are now well above market expectations for €2.8b/€3.2b in operating cash flows over next 2 years. Analyst comments today point to another 5-15% in cuts to FY24 earnings, uncertain how many of those revisions has already been captured in today's numbers we are quoting (that are down on the day).

- The sales/FCF revision down should be enough for a downgrade but still only a small dent on BS (subject to acquisition/Capex though)- it runs leverage at 1.3* with net debt of €8.5b (up from 0.3* in FY22) - that was after €1.75b in dividends from €1.98b in FCF net of RE acquisitions (€3.3 excluding) at a 56% pay-out ratio.

- That was higher than its target 50% pay-out ratio & leaves headroom to cut dividends if it chooses to - interim dividend expectations are unch at €4.5/share or ~€550m. No buyback last year, policy is "flexible".

- S&P saw FY23 leverage at 2.2* (up from 1.1*) which it expected to remain flat - we don't see that happening now - before falling 2025 to 1.8*-2*; downgrade was on leverage remaining above 2*.

Downgrade has been firmly priced in this morning - 30's give +20bps to Richemont (NR, A+) & outside the sector now trades in line with Booking.com/BKNG (A3/A-).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok