Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

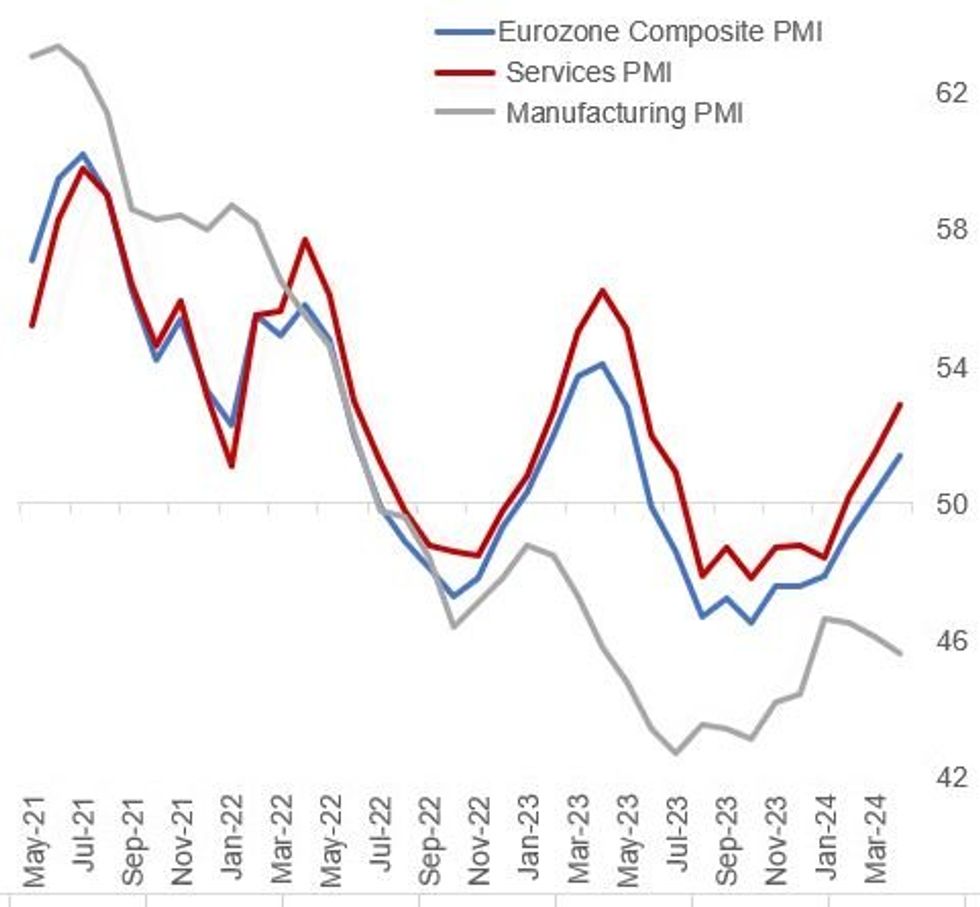

Eurozone flash PMIs for April came in unexpectedly strong on aggregate, with Services at 52.9 (51.8 expected, 51.5 prior) offsetting an unexpected pullback in manufacturing to 45.6 (46.5 expected, 46.1 prior). While these figures had been telegraphed in advance by similar surprises in the German and French reports released earlier, they pointed to the Eurozone economy emerging from recessionary conditions, if somewhat unevenly.

- The composite reading of 51.4 (50.7 expected, 50.3 prior) was the highest since May 2023, and the 2nd consecutive print above 50.0 after 9 months in contractionary territory. For Services, this was the 3rd straight expansionary reading (also an 11 month high), while Manufacturing has weakened for 3 consecutive months and has been in contraction for 22 straight months.

- The HCOB/S&P Global report noted that "price pressures also picked up across the eurozone alongside the improvement in output and hiring, often linked to higher wage bills. Input costs and average selling prices both rose at faster rates, reflecting stubbornly elevated price pressures in the service sector." Renewed wage-led service price pressures will give the ECB something to think about ahead of the June meeting, where a cut appears to be the central case for the Governing Council.

- Additionally, "especially solid growth outside of France and Germany was again reported...output rose for a fourth consecutive month in April in response to robust growth in the service sector and near-stable manufacturing output", auguring well for Italy and Spain in the final April prints.

- Other highlights from the report: "New orders for services rose in April at the fastest pace since May of last year, up for a second straight month, but new orders for manufactured goods fell at an increased rate."

- "The rate of net job creation accelerated to the highest since last June. A ten-month high rate of employment growth in the service sector drove the increase."

- "A pull-back in service sector confidence, to a three-month low, contrasted with improved optimism in the manufacturing sector, where output expectations rose their highest since February of last year."

Source: HCOB, S&P Global, MNI

Source: HCOB, S&P Global, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok