Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

The August NFIB small business survey Optimism Index printed 91.3, down 0.6pp and a touch below the expected 91.5. Many of the themes that have been prevalent this year were repeated in the August report, with most sub-categories relatively steady in comparison to the previous 3 to 6 months.

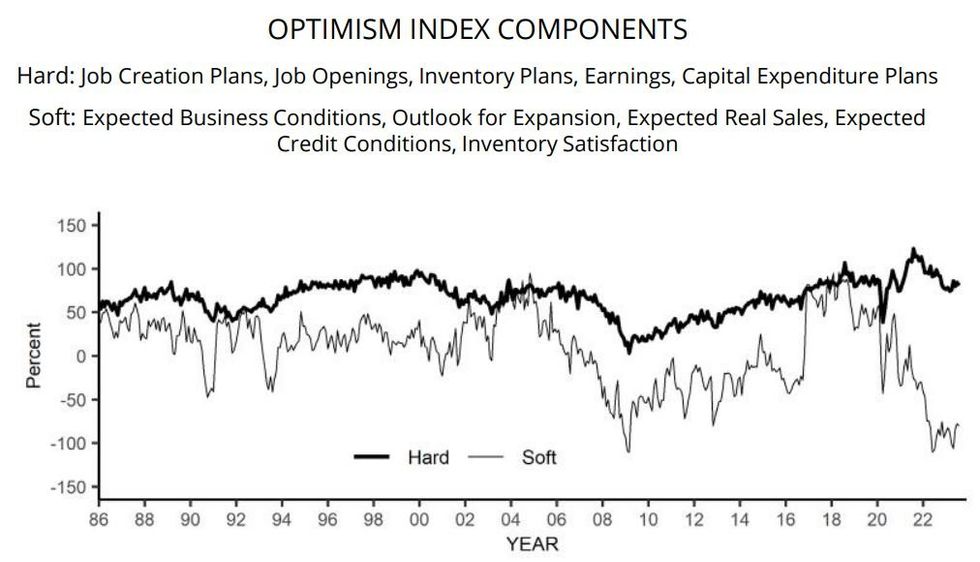

- The bifurcation between steady/strengthening "hard" index components (job creation plans, job openings, inventory plans, earnings, capex) vs depressed "soft" (expected biz conditions, expansion outlook, expected real sales / credit conditions, inventory satisfaction) continued. See chart.

The inflation, labor market, and credit conditions components will bear closest scrutiny - and they remained mixed. Quality of labor (cited by 24% of respondents) and Inflation (23%) remain the biggest problems for small businesses.

- Labor market results suggested some signs of loosening on the hiring side, offset by expected wage growth. While hiring plans ("increase" minus "decrease" in the next 3 months) were unchanged at a net 17%, in line with the averages of the previous 9 months, the "percent with positions not able to fill right now" slipped to 40% - lowest since Feb 2021 - from 42% the previous 2 months. Compensation changes slipped 2pp to a net 36%, joint-lowest since May 2021, but compensation plans rose to the highest net percentage of the year at 26% (+5pp).

- Inflation pressures remained salient but mixed. Net actual price changes ticked up 2pp to 27%, but that's the 2nd lowest since Mar 2021. Net price plans ticked up 3pp to 30%, the 2nd highest of the year, though below the 31%-to-54% range that prevailed for most of 2021-22.

- There were few signs of duress in credit availability. While interest rates paid remained high, loan availability vs 3 months ago improved to a net -4% from -6%, representing the least negative level since June 2022.

Source: NFIB August Survey

Source: NFIB August Survey

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok