TRANSPORTATION

- Reminder Avinor is Norwegian state-owned co that operates "43 airports" and services "50m passengers annually"; half of which travel to/from Oslo Airport (capital).

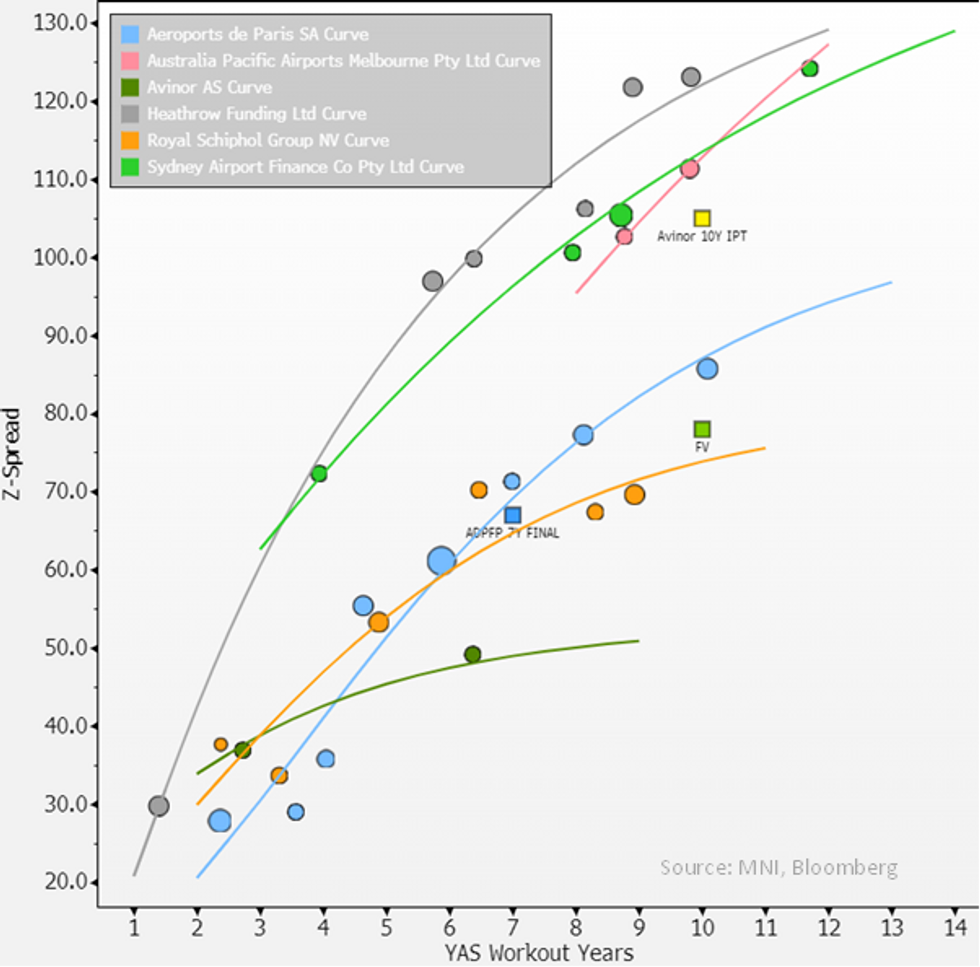

- Comps are Schipol (A2/A), the owner & operator of Amsterdam Airport and Aeroports de Paris (NR/A Neg/BBB+), operator of the 3 main airports in Paris.

- Re. standalone ratings; Avinor is Baa2 rated (4 notch uplift), Schipol Baa1 (2-notch) & ADEFP A- on S&P (1-notch).

- Re. Avinor 30s, looks like it has been left well tight - curve is flat even for A-grade (below). Spread over time is messy as well (& names have had rating changes through Covid). We largely ignore it for pricing.

- We don't think final can come inside Schipol 33s (8.9yr) at Z+70 - its equal rated on S&P and 1-notch higher standalone on Moody's - we spread new issue +8bp to it at Z+78. That leaves it above the Schipol curve but fair to us given ADPFP 10y trades at Z+86. We think anything more than 8bps makes the ADPFP look cheap.

- UoP is left broad, we see it as net supply here with only small maturities this year. Front bond is €300m April 25s (at €97.5). Its been 4 years since its last bond issuance.

252 words