Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

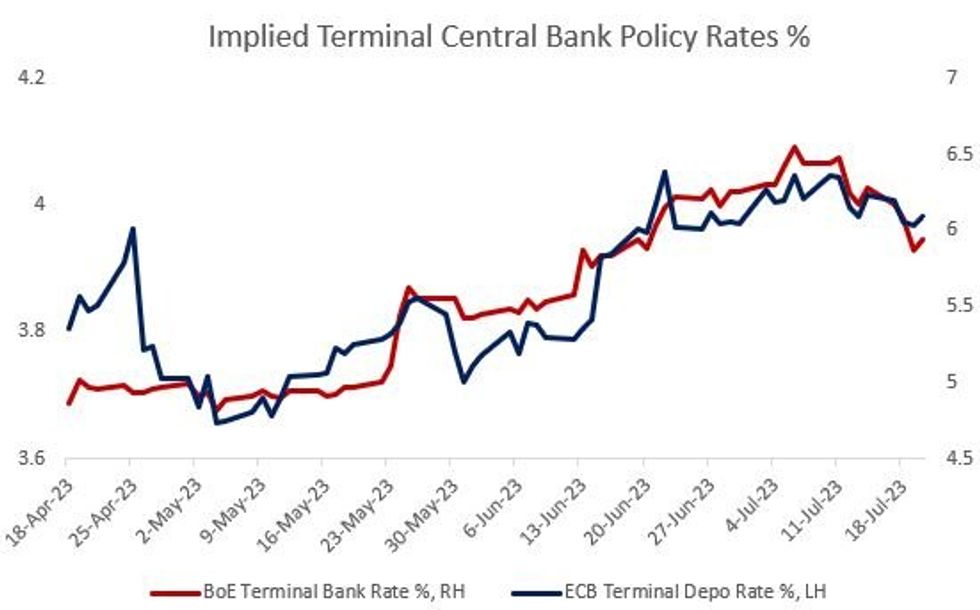

UK and Eurozone central bank tightening expectations firmed Thursday alongside a sell-off in US rates.

- BoE terminal Bank Rate pricing +7.2bp to 5.94% (94bp of further hikes left in the cycle to Feb 2024). Peak pricing is up 12bp from Wednesday's post-UK CPI lows, but remains below the 6% threshold, let alone July's highs above 6.50%. UK retail sales feature first thing Friday morning as a potential macro catalyst., particularly for the August MPC (for which a 50bp hike remains roughly 45% priced vs 25bp 55%). Cumulative hikes through Sept are priced at 66bp, and Nov at 83bp.

- ECB terminal depo Rate pricing +1.3bp to 3.98% (48bp of further hikes left in the cycle to Dec 2023). ECB peak pricing remains firmly anchored, having closed within 5bp of the 4.00% implied mark since June 19. We continue to await a decisive catalyst to change this, with next Thursday's ECB meeting messaging potentially key (though for the meeting itself, a 25bp hike is 95+% priced).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok