Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

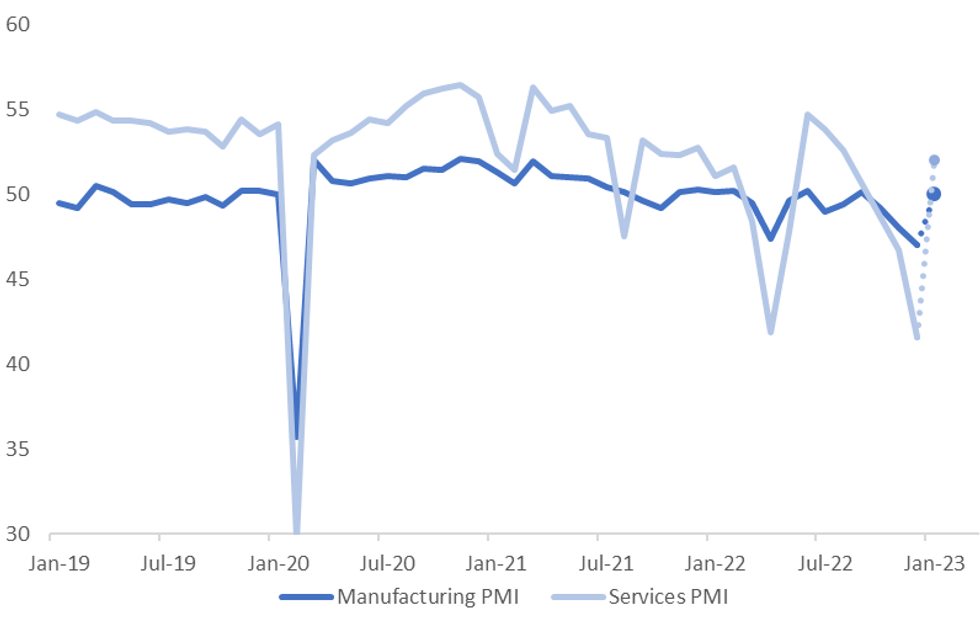

A reminder that tomorrow delivers the official manufacturing and non-manufacturing PMIs for Jan. The market is looking for a steep improvement, particularly in the non-manufacturing/services index, see the chart below. The consensus sits at 52.0, versus 41.6 in Dec. For manufacturing the consensus is 50.0 versus 47.0 in Dec.

- The range of expectations is quite wide, 45.0 to 53.3 for services, 48.5 to 52 for manufacturing.

- The anecdotes pointed to a noticeable improvement in activity through January as Covid cases subsided. Mobility indicators picked up, while spending and travel activity picked up through the LNY period, albeit not quite to pre Covid levels of 2019 (see this link for more details).

- How this translates into the PMIs remains to be seen, with an improvement obviously expected, but the risk of supply related disruptions something that can't be discounted.

- It's likely that China data will start to have more of impact now that we are clear of the Covid wave, and the market starts to assess how growth momentum is shaping up in the first part of 2023.

- China markets largely ignored disappointing data through Nov/Dec as it focused on the 2023 outlook following the pivot away from CZS.

Fig 1: China PMIs Expected To Rebound Sharply For January

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok