Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

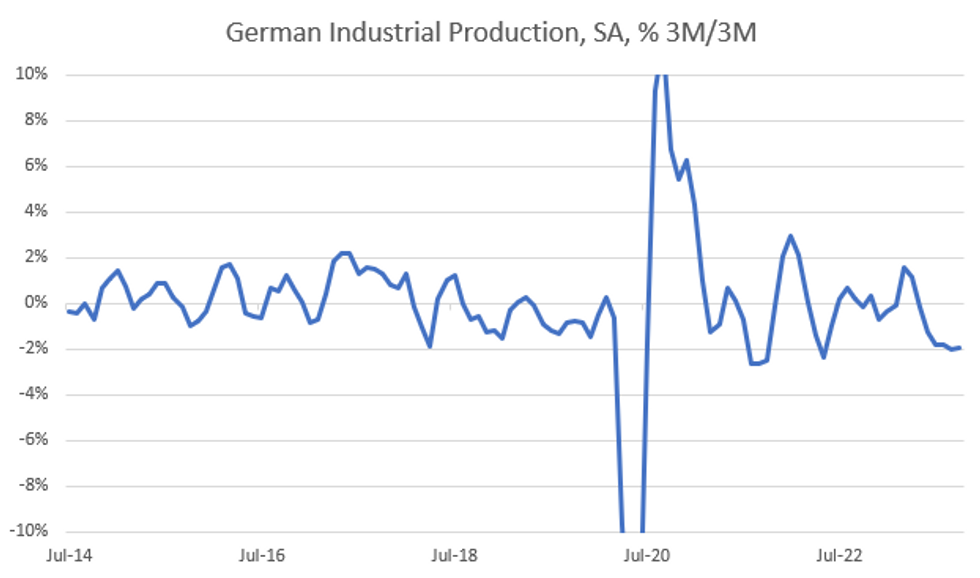

German October Industrial Production data missed expectations at -0.4% M/M (seasonally adjusted, +0.2% consensus, -1.3% prior, revised from -1.4%) and -3.5% Y/Y (working day adjusted, -3.0% cons, -3.6% prior, revised from -3.7%).

- This was the fifth monthly decline in a row, though the less volatile 3M/3M measure ticked up slightly to -1.9% from -2.0% in September.

- The decline was broad-based but particularly driven by a soft month in the equipment manufacturing sector (-6.3% M/M vs +3.9% prior), matching developments from October factory orders. Automobile production recovered slightly after last month’s decline (+0.7% M/M vs -5.0% M/M).

- Excluding the energy and construction sectors, the report paints a weak, but slightly stronger picture versus September on all of a monthly, yearly, and three-monthly comparison (-0.5% M/M, -3.2% Y/Y and -1.9% 3M/3M vs -1.7%, -3.5% and -2.1% respectively).

- The energy-intensive sector continues to suffer, production declined a further -1.4% M/M in October (vs -1.1% prior). The recently announced energy tax relief might provide some slight support for the industry starting in January but is not expected to provide a major shift in German industrial competitiveness.

- This industrial production report is consistent with recent data releases (October factory orders / November manufacturing PMI / October trade balance) which have suggested that the economic decline in Germany is flattening out slightly.

- After Wednesday's substantial factory orders data miss (which as MNI noted actually saw a decent "core" reading), an IP miss vs the consensus coming into the week may have been partially priced in. However, the IP release provided a slight bid to Bund futures, which ticked up over 15 ticks to around 135.1.

Destatis, MNI

Destatis, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok