Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROPEAN INFLATION

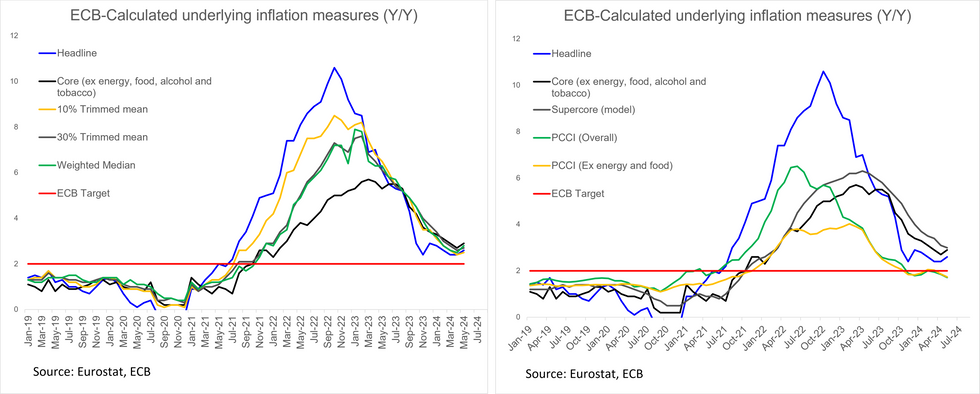

The ECB’s underlying inflation metrics registered a broad-based softening in June, despite overall core inflation remaining at 2.9%.

- Although few new policy signals are expected at tomorrow’s ECB meeting, the disinflationary development of underlying inflation metrics should give Governing Council members confidence that inflation is still on its way back to target – even as some components (i.e. services) remain sticky.

- This development also supports market pricing, with OIS pricing an ~80% implied probability of a 25bp cut through the September meeting.

- Both headline and core PCCI remained below 2% in June, at 1.71% Y/Y and 1.74% respectively (broadly unchanged to May’s levels).

- Supercore was 2.9% Y/Y - below 3% for the first time since February 2022.

- The weighted median measure saw the most notable fall, to 2.2% Y/Y (vs 2.8% in May).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok