Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

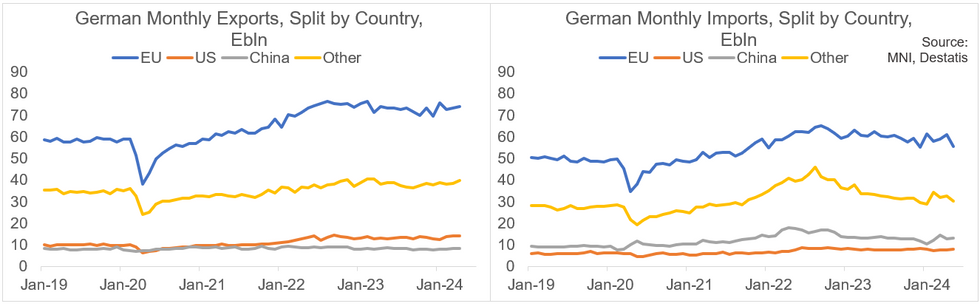

The German trade surplus widened more than forecast, to E24.9bln (seasonally-adjusted, vs E20.3bln cons; E22.2bln prior, revised from E22.1bln) amid a heavy drop in imports of 6.6% M/M (vs -1.0% cons; +1.2% prior, revised from +2.0%). Exports also fell but less so than imports, at -3.6% M/M (vs -2.8% cons; +1.7% prior, revised from +1.6% prior).

- While these are nominal, not real, figures and thus don't account for price volatility, to put it into perspective, the trade surplus widened to the equivalent of about 6.2% of nominal GDP on a 12-month rolling basis - up from about 6.0% last month and the highest since March 2020.

- Two conclusions remain:

- Even though the higher trade surplus will be accounted for positively from a GDP growth perspective, diminishing bilateral trade volumes (the sum of ex- and imports, which are back to December 2023 levels) can be considered a rather weak sign for the German economy going forward.

- The data adds to the narrative of stalling intraregional trade in the EU ('EUROZONE: Stalling Intraregional Trade': MNI, Jul 4).

- The declines were quite broad-based. Exports to the EU (-2.5% M/M vs +1.2% prior), the US (-2.9% M/M vs -0.7% prior), China (-10.2% M/M vs +1.0% prior) and the ex-EU/US/CN category (-4.9% M/M vs +2.4% prior) all fell. Imports fell considering EU (-8.9% M/M) and the ex-EU/US/CN (-8.2% M/M) categories, which inclines from the US (+4.6% vs -0.7% prior) and China (+1.7% M/M vs -12.3% prior) were not able to make up for.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok