Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY

The latest round of strong US labour market data (detailed elsewhere) pushes BTP futures to new intraday lows, fully paring the recovery seen following this afternoon's 15-year syndication announcement. Our technical analyst notes that a clear break of last week's low of 116.98 is required to confirm a resumption of the recent bearish cycle.

- The 10-year BTP/Bund spread widened over 1bp following the syndication announcement, and now trades 3.4bps wider at 153.3bps. This morning, the spread opened below 150bps at its tighest levels since early-2022.

- BTP yields have accordingly reached new daily highs, with yields now 6-7.5bps higher, following on from this morning's higher-than-expected Spanish inflation data, 5/10-year BTP auctions and stronger-than-expected domestic GDP data (see below).

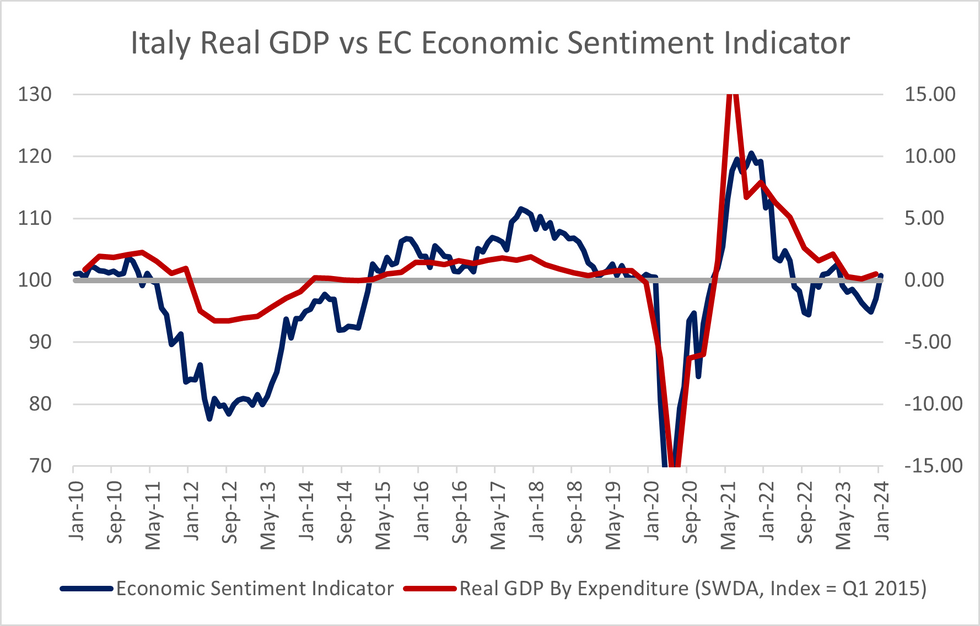

- Italian flash Q4 '23 GDP (SWDA) exceeded consensus expectations at +0.2% Q/Q (vs 0.0% cons; 0.1% prior) and +0.5% Y/Y (vs 0.2% cons; 0.1% prior). ISTAT noted that net exports contributed positively to the Q/Q print, while the domestic component contributed negatively. Industry and services saw a rise in value added over the quarter, with agriculture, forestry and fishing seeing a fall.

- Today also saw the release of the EC's forward looking sentiment survey, which in Italy's case rose above 100 (indicating an expansion) for the first month since April '23, with all industries other than construction seeing an improvement vs December's levels.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok