Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

Executive summary

- Bank of Korea decided to follow CEEMEA/Latam central banks and has embarked into a tightening cycle in the past six months to ease the rising inflationary pressures.

- However, South Korea’s biggest trading partner China is keeping its ‘zero-Covid policy’, which has been constantly weighing on growth expectations in the past year and therefore could impact Korean economic activity in the medium term.

- A significant slowdown in the economic activity combined with a deceleration in global liquidity could lead to greater volatility in 2022 and therefore weigh on Korean domestic assets and the KRW.

Link to full article:

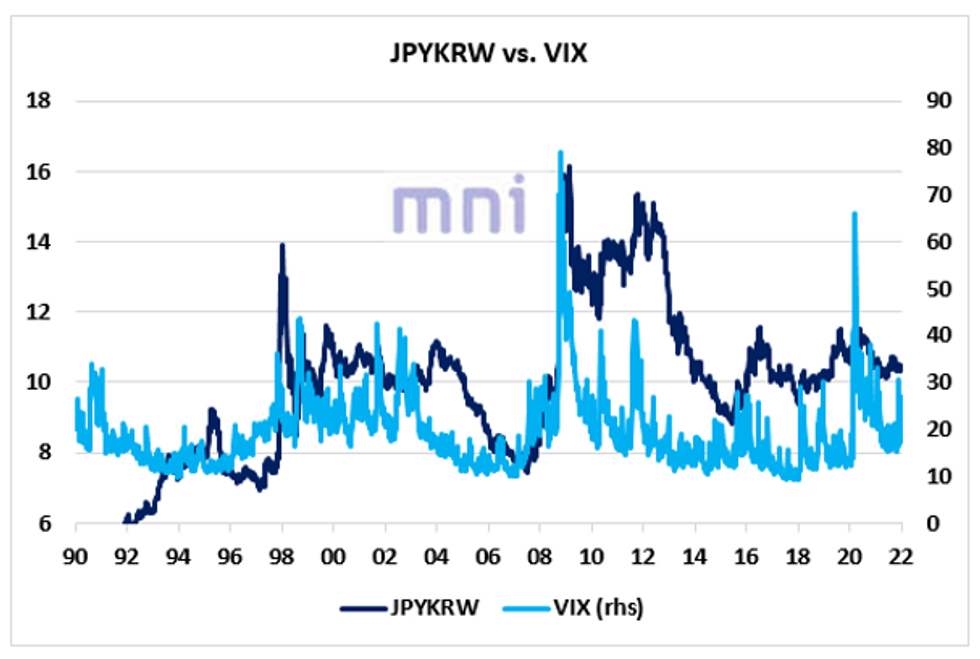

The Korean won has also been acting as a ‘risk-on’ currency in the past 30 years, which tends to depreciate significantly in periods of rising volatility (i.e. VIX). The chart below shows the strong co-movement between JPYKRW (risk off pair) and price volatility (VIX) in the past thirty years. As growth expectations in SK continue to fade in 2022 and global liquidity continues to decelerate, risky assets could experience greater volatility this year, which would be negative for the KRW.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok