Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK DATA

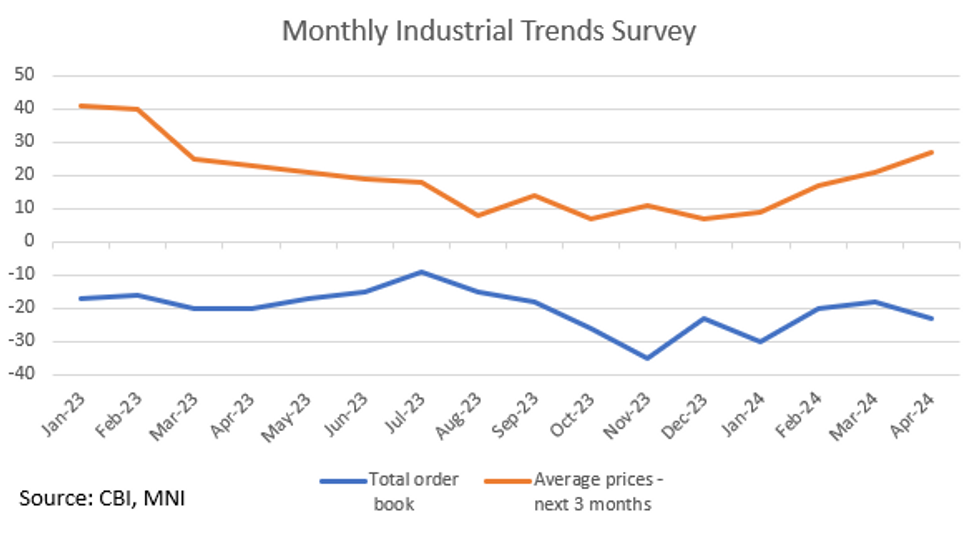

UK CBI Order Books Balance fell to -23% (vs -18% prior) in April, the lowest level since January 2024, again remaining below the long run average of -13%.

- Expectations for average selling price for next three months picked up for the fourth consecutive month to 27% (from 21% in March) - making it the highest since February 2023, and again remaining higher than the long run average of 7%.

- The CBI surveys manufacturing firms and hence this will be of importance to the part of non-energy industrial goods (NEIG) that is domestically produced. This sustained pickup in average selling price expectation will be concerning to the MPC, particularly as NEIG inflation has been easing recently (while services inflation has remained more sticky). If NEIG starts to stabilise, rather than disinflating, services inflation may need to be lower to get inflation sustainably back to target.

- Survey conducted between 25 March and 12 April, with 257 manufacturing firms responding.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok